E-commerce Working Capital: Stop Guessing, Start Calculating Your Exact Need

12

mins read

TL;DR

Working capital needs are use-case specific: Calculate (Monthly COGS × Inventory Months) + Fixed Costs + Ad Spend, not generic 15-25% benchmarks.

Over-capitalization has hidden costs: Taking €100K when €60K covers the need means paying fees on €40K idle capital, increasing effective cost by 40%+.

2026 presents unique challenges: Tariffs increased COGS 15-30%, CPMs rose 22% YoY, and conversion rates dropped 8-12%, demanding real-time visibility.

Dynamic pricing rewards patience: Improving business health metrics before drawing capital can reduce financing costs by 15-30%.

RBF beats bank loans for speed: 48-72 hours vs. 6-8 weeks, no personal guarantees, but static pricing without intelligence creates blind spots.

AI transforms guesswork to strategy: Intelligence without capital is advice; capital without intelligence is risk. The 2026 imperative combines both.

Q1. Why Do E-commerce Businesses Struggle to Calculate Working Capital Needs? [toc=Working Capital Challenges]

It's 11 PM on a Tuesday. The CFO of a €4M DTC brand sits surrounded by browser tabs: Shopify payouts in one, Stripe settlements in another, Amazon disbursement reports downloading, and Xero reconciliation spreadsheets sprawling across 30+ tabs. The question is simple: Can we afford the Q2 inventory order? The answer remains elusive after three hours of manual data stitching.

This scenario plays out nightly across thousands of growth-stage e-commerce businesses. The frustration isn't incompetence. It's architectural.

⚠️ Why Traditional Formulas Fail E-commerce

The classic working capital formula, Current Assets minus Current Liabilities, assumes stable, predictable single-channel businesses. E-commerce operates nothing like this.

Consider the variables traditional formulas ignore:

Seasonal revenue swings: 3-5x fluctuations between Q1 and Q4 for many DTC brands

Inventory cycles: 45-90 days of cash locked in products before a single sale

Marketplace holdbacks: Amazon retains 10-20% of disbursements in reserve accounts

Channel-specific payout schedules: Shopify pays in 2 days, Amazon in 14, wholesale in Net 30-60

"I find my cash is locked up in inventory and marketing, leaving me without the necessary working capital to scale as quickly as I know I can." — u/anonymous, r/ecommerce Reddit Thread

"Having to predict stock for 1-3 month lead times can be incredibly tricky when you have zero historical data, are growing rapidly, and your liquid cash reserves then become tied up in stock." — u/anonymous, r/ecommerce Reddit Thread

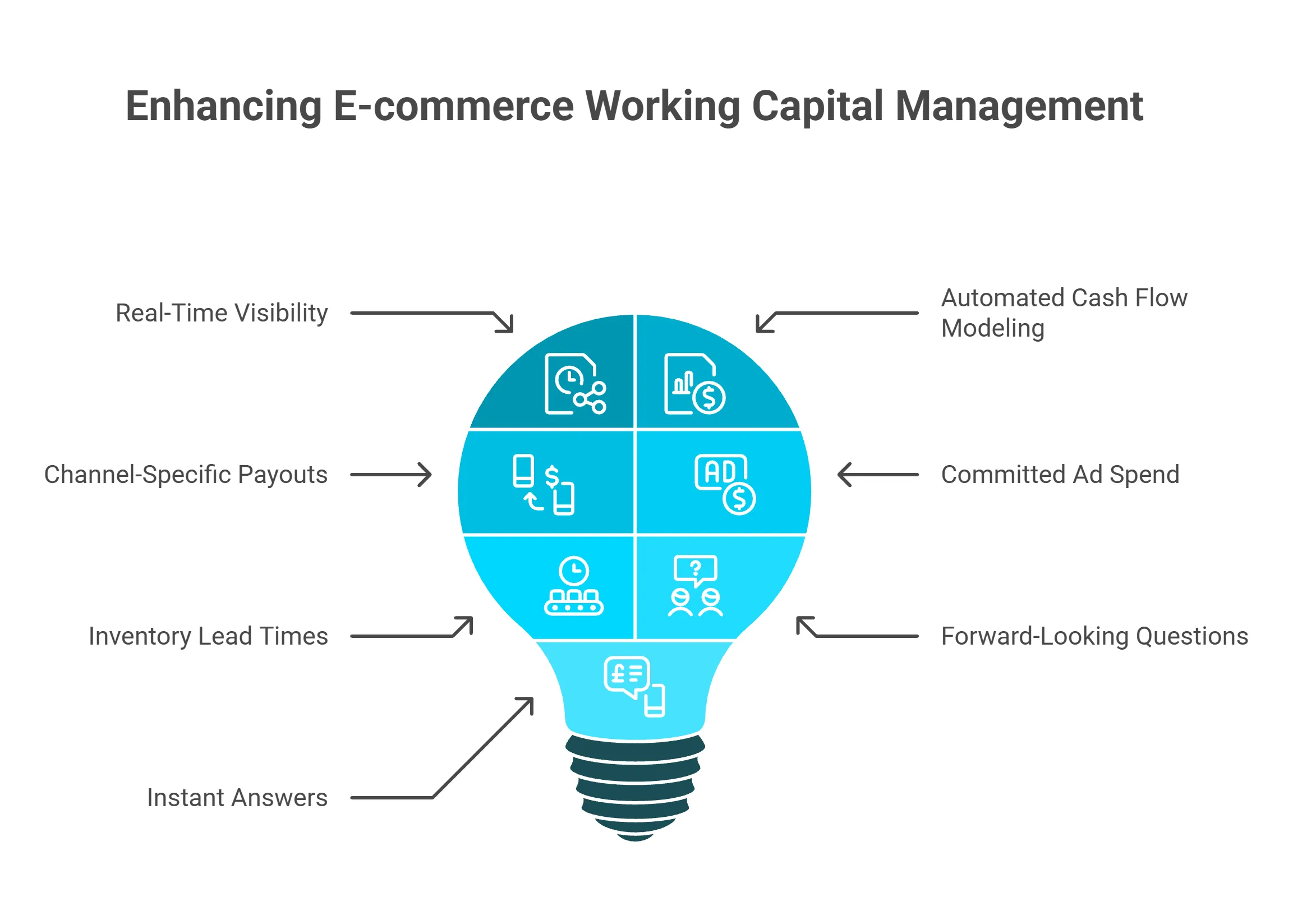

✅ What Working Capital Visibility Should Look Like

Lightbulb visualization depicting key working capital management components including real-time visibility, automated cash flow modeling, channel-specific payouts, and forward-looking financial questions for e-commerce.

The ideal state isn't more spreadsheets. It's synthesis. Real-time visibility across ALL revenue channels (DTC, marketplaces, wholesale) with automated cash flow modeling that accounts for channel-specific payout schedules, committed ad spend, and inventory lead times.

Instead of asking "What's my cash position?", a question that requires hours of reconciliation, founders should be asking forward-looking questions: "What's my cash position in 90 days if I scale this campaign?" and receiving answers in seconds.

How Luca AI Eliminates the Reconciliation Burden

Luca AI connects Shopify, Amazon, Stripe, Xero, and advertising platforms into a unified intelligence layer. Rather than exporting CSVs and building pivot tables, founders ask natural language questions spanning commerce, marketing, and finance simultaneously.

The system synthesizes cross-channel cash positions, models payout timing across platforms, and factors in committed advertising spend, delivering dynamic working capital forecasts that update as business conditions change. When opportunity emerges, Luca can surface capital offers sized to the specific use case, not arbitrary maximums.

Q2. What Is the Working Capital Formula and How Should E-commerce Brands Adapt It? [toc=Working Capital Formula]

📊 The Standard Working Capital Calculation

Working capital measures short-term financial health through a straightforward formula:

Working Capital = Current Assets − Current Liabilities

Financial analysts typically recommend a working capital ratio between 1.5:1 and 2:1 for healthy businesses. However, e-commerce brands, with their inventory intensity and variable cash cycles, often require higher ratios of 1.8:1 to 2.5:1 to maintain operational flexibility.

The working capital ratio formula:

Working Capital Ratio = Current Assets ÷ Current Liabilities

A ratio of 2:1 indicates the business holds €2 in current assets for every €1 in current liabilities, providing buffer for unexpected demands or growth opportunities.

⏰ Understanding the Cash Conversion Cycle

The cash conversion cycle (CCC) reveals how long cash remains tied up in operations before returning as revenue. For e-commerce, this metric directly determines working capital requirements.

CCC = DIO + DSO − DPO

Where:

DIO (Days Inventory Outstanding): Average days holding inventory before sale

DSO (Days Sales Outstanding): Average days to collect payment after sale

DPO (Days Payable Outstanding): Average days to pay suppliers

Example calculation for a €3M DTC brand:

DIO: 60 days (inventory holding period)

DSO: 7 days (payment processor settlement)

DPO: 30 days (supplier payment terms)

CCC = 60 + 7 − 30 = 37 days of cash tied up per cycle

"Working capital is calculated by subtracting current liabilities from current assets... as a company expands, its working capital rises because it purchases more materials and its lead times lengthen." — u/anonymous, r/smallbusiness Reddit Thread

💰 E-commerce-Specific Adjustments

Standard formulas miss critical e-commerce variables. A more accurate framework includes:

E-commerce Working Capital Components

Component

Calculation

Base working capital

Monthly COGS × Inventory months

Committed ad spend

Next 30 days of planned advertising

Refund reserves

2-5% of monthly revenue

Marketplace holdbacks

Amazon/Walmart reserve amounts

Seasonal buffer

Additional inventory for peak periods

Adjusted Formula: Base Working Capital + (Monthly Burn × Growth Buffer) + Seasonal Inventory Premium + Committed Marketing Spend

✅ Framework for Optimal Capital Sizing

Rather than calculating "maximum available," right-sized capital matches specific use cases:

Minimum viable capital: Covers one complete inventory cycle

Growth capital: Funds specific expansion opportunity (campaign scale, new SKU launch)

Safety buffer: 2-4 weeks of fixed costs for unexpected disruptions

Total = Opportunity-specific amount, not arbitrary percentage

Luca AI automates these calculations by synthesizing real-time data from commerce, payments, and accounting systems. The platform generates dynamic working capital forecasts that update continuously, sizing capital recommendations to specific use cases rather than generic industry benchmarks.

Q3. How Much Working Capital Does a €1M-€20M E-commerce Business Actually Need? [toc=Capital Requirements by Revenue]

Most e-commerce businesses need 3-6 months of operating expenses as accessible working capital, translating to roughly 15-25% of annual revenue. For a €5M brand, this suggests €750K-€1.25M across cash reserves and credit facilities. But these generic benchmarks often miss the mark. The RIGHT answer depends entirely on your specific situation, not blanket percentages.

💰 A Practical Calculation Approach

Rather than applying industry averages, calculate your specific requirement:

✅ Dropshipping operations (no inventory commitment)

✅ High gross margins (60%+)

✅ Single-channel simplicity

"Since then, I've faced ongoing challenges with stock availability due to a 60-day lead time, and I simply lack the working capital to purchase sufficient inventory." — u/anonymous, r/Entrepreneur Reddit Thread

"Wayflyer has been a game-changer for our business. The funding process was fast, straightforward, and transparent." — Verified Review, Trustpilot

✅ How Luca AI Calculates Your Specific Need

Luca AI analyzes your actual cash conversion cycle, seasonal patterns, channel mix, and growth velocity to calculate precise working capital requirements. Rather than suggesting generic percentages, the platform surfaces capital offers sized to your real opportunity, matching funding to specific use cases like inventory orders or campaign scaling, not arbitrary maximums.

Q4. The 'More Is Better' Myth: What's the Hidden Cost of Idle Capital? [toc=Hidden Cost of Idle Capital]

Common financing advice suggests taking maximum available capital: "you never know when you'll need it." This seemingly prudent approach ignores a critical reality: capital carries costs, and idle capital is expensive capital. When a founder takes €100K but deploys only €60K, fees apply to the full principal while €40K generates zero return.

💸 The True Cost of Over-Capitalization

The hidden costs of taking more than needed compound quickly:

Hidden Costs of Over-Capitalization

Cost Category

Impact

Fee drag

RBF fees (6-12%) apply to full principal, not deployed amount

Opportunity cost

Idle cash could earn 4-5% in money markets

Repayment pressure

Larger advances mean higher revenue-share percentages

Decision fog

Excess capital masks poor unit economics

Taking €100K when €60K covers the use case means paying fees on €40K that sits idle, effectively increasing the cost of deployed capital by 40% or more.

"Model the effective cost of capital and check for any minimum remittance floors that could bite during slow months." — Flippa E-commerce Funding Guide

✅ The Right-Sizing Alternative

The alternative approach: match capital precisely to specific use cases. Instead of €100K "just in case," structure funding around actual deployment:

€35K for the confirmed inventory order

€25K for the proven campaign scale

Total deployed: €60K with fees only on deployed capital Savings: 40% lower financing cost for identical business outcomes

⏰ The Case for Smaller, More Frequent Advances

Modern revenue-based financing platforms, unlike traditional loans, don't penalize multiple draws. Taking €30K three times as opportunities materialize costs less than €100K upfront, with additional advantages:

Each advance prices based on current business health

No fees on capital sitting idle between opportunities

Flexibility to adjust sizing as conditions change

"I've mostly relied on quick-access options because they were easy to renew and didn't require much paperwork, but the daily repayment is definitely starting to hurt now that margins are thinner." — u/Kelvinh6354, r/ecommerce Reddit Thread

"Good experience funding my wholesale/ecomm business, clear cost of capital. Their systems are easy to navigate." — Verified Review, Trustpilot

How Luca AI Enables Precision Capital Sizing

Luca AI recommends capital sized to specific opportunities, not maximum available. When the platform surfaces a scaling opportunity, funding recommendations match the use case precisely: "Campaign X shows 3.8x ROAS. €28K would fund a 4-week scale test. Available now at 5.2%."

This precision approach eliminates fee drag on idle capital while ensuring founders capture time-sensitive opportunities without over-committing to unnecessary financing costs. The AI Co-Founder model connects intelligence with capital, so the system that identifies the opportunity also sizes the funding appropriately.

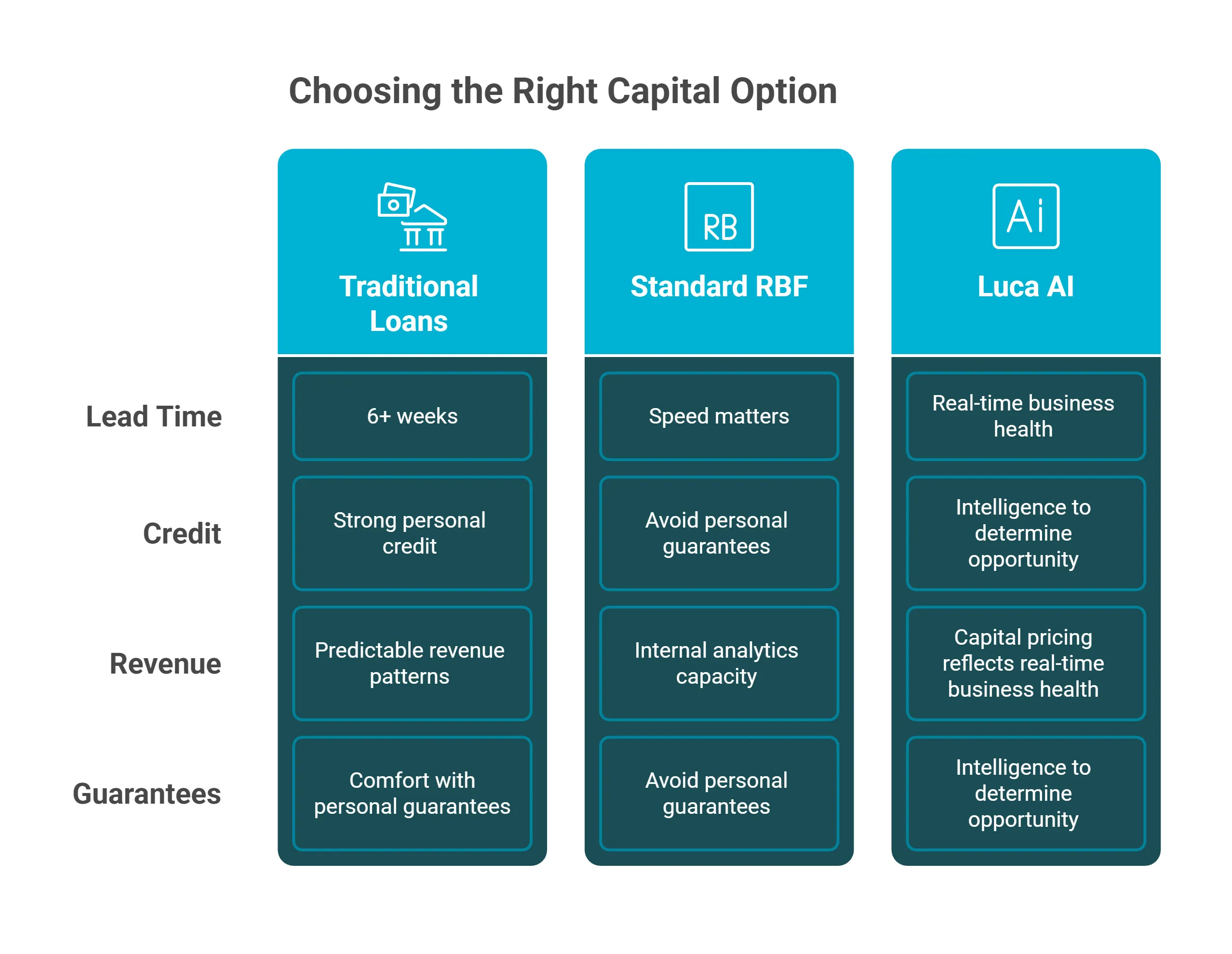

Q5. Revenue-Based Financing vs. Traditional Loans: Which Suits E-commerce Better? [toc=RBF vs Traditional Loans]

You've identified a growth opportunity, a winning campaign ready to scale, inventory to secure for Q4, or seasonal demand to capture, but lack the capital to execute. Both revenue-based financing (RBF) and traditional bank loans address this gap, but through fundamentally different mechanisms that produce dramatically different outcomes for e-commerce operators.

Visual comparison of three e-commerce capital options evaluating lead time, credit requirements, revenue conditions, and guarantee needs, highlighting Luca AI's real-time business health approach.

💰 Traditional Bank Loans: The Established Path

Traditional bank financing offers certain advantages that remain relevant for specific situations:

✅ Strengths:

Lower headline rates (8-12% APR)

Predictable fixed monthly payments

Builds business credit history for future borrowing

❌ Limitations for E-commerce:

6-8 week approval cycles, opportunity often passes

Personal guarantees required in most cases

Rigid repayment regardless of revenue fluctuations

Collateral requirements mismatched to asset-light business models

Inflexible use-of-funds restrictions

"Local banks have expressed that our reinvestment strategy 'doesn't look good' and seem to overlook our revenue growth, perceiving us as largely unprofitable." — u/anonymous, r/smallbusiness Reddit Thread

⏰ Revenue-Based Financing: Speed with Trade-offs

RBF platforms like Wayflyer and Clearco solve the speed problem but introduce their own constraints:

✅ Strengths:

48-72 hour approval and funding

No personal guarantees or collateral

Repayments flex with revenue (slow month = lower payment)

No guidance on whether the opportunity merits funding

"RBF is expensive financing, but it's an option when traditional lenders are wary. It's important to note that the overall repayment amount can be higher than that of conventional loans." — u/Ambitious-Echo4890, r/smallbusiness Reddit Thread

📊 Head-to-Head Comparison

Financing Options Comparison

Feature

Traditional Loans

Standard RBF

Luca AI Dynamic RBF

⏰ Approval Speed

6-8 weeks

48-72 hours

Same day

💸 Personal Guarantee

❌ Required

✅ None

✅ None

💰 Repayment Flexibility

Fixed payments

Revenue-linked

Revenue-linked

Effective Cost

8-12% APR

15-25% of capital

Dynamic (improves with health)

Intelligence Layer

❌ None

❌ None

✅ Cross-functional reasoning

Capital Sizing

Lender-determined

Application-based

✅ Opportunity-matched

✅ Which Option Fits Your Situation?

Choose traditional loans if: You have 6+ weeks lead time, strong personal credit, predictable revenue patterns, and comfort with personal guarantees.

Choose standard RBF if: Speed matters, you want to avoid personal guarantees, but you have internal analytics capacity to determine deployment strategy.

Choose Luca AI if: You want capital pricing that reflects real-time business health AND intelligence to determine whether the opportunity is worth pursuing, before you commit.

Q6. How Should You Time Capital to Specific Use Cases? [toc=Capital Timing Strategy]

⏰ The Capital Timing Principle

The optimal moment to access capital is when a specific, validated use case exists with a defined deployment window, not "just in case" or "while it's available." Mismatched timing creates unnecessary costs: capital arriving 6 weeks before deployment means paying fees on idle funds while opportunity economics potentially shift.

This principle inverts conventional wisdom. Traditional advice suggests maintaining maximum available credit "for opportunities." The data suggests otherwise: precisely-timed capital aligned to deployment produces superior outcomes.

💰 Timing by Use Case Category

Different working capital needs demand different timing strategies:

Inventory Orders

✅ Trigger: When purchase order is confirmed with supplier

❌ Avoid: When "considering" reorder or building forecasts

Deployment window: Match to supplier lead time (typically 30-90 days)

Campaign Scaling

✅ Trigger: When ROAS stabilizes above threshold for 7+ consecutive days

❌ Avoid: During initial testing phase or first profitable week

Deployment window: 14-28 day scale test cycles

Seasonal Preparation

✅ Trigger: 4-6 weeks before expected demand spike

❌ Avoid: 3 months early "to be safe"

Deployment window: Align to seasonal inventory cycle

Wholesale/B2B Expansion

✅ Trigger: When order is confirmed with deposit received

❌ Avoid: During prospecting or negotiation phases

Deployment window: Match to production and delivery timeline

⚠️ Timing Anti-Patterns to Avoid

Four common timing mistakes increase capital costs without improving outcomes:

Capital Timing Anti-Patterns

Anti-Pattern

Problem

Cost Impact

"Bank it for later"

Paying fees on idle capital

6-12% on unused funds

"End of quarter availability"

Taking capital because offered, not needed

Unnecessary carrying costs

"Round number bias"

Taking €100K when €67K covers use case

33% over-capitalization

"Fear-based buffer"

Adding 50% "safety margin"

Half the capital sits unused

✅ Matching Capital Velocity to Deployment Velocity

Capital velocity should match the return cycle of its intended use:

Inventory capital (60-day turns) → 60-90 day deployment horizon

Marketing capital (14-21 day ROAS cycles) → Size to 2-3 week increments

Seasonal capital (90-day peak periods) → Deploy across the full season

Mismatched velocity, taking 6-month capital for 3-week campaign tests, wastes carrying cost on funds that sit idle between deployments.

How Luca AI Optimizes Capital Timing

Luca AI matches capital offers to use-case timing automatically. When the platform identifies a scaling opportunity, it calculates both the optimal funding amount AND the deployment window: "Deploy €32K to Campaign X over 21 days for projected €128K incremental revenue. Available now at 5.2%." Capital arrives precisely when needed, sized to the specific opportunity, eliminating timing waste.

Q7. How Do Multi-Channel Sellers Manage Working Capital Across Platforms? [toc=Multi-Channel Capital Management]

You sell across Shopify (55% of revenue, 2-day payouts), Amazon (30%, 14-day disbursements with 10% reserve holdback), and wholesale to three retailers (15%, Net 45 terms). Each channel operates with different margin profiles, payout timing, and cash conversion cycles. Your spreadsheet attempts to reconcile all three, but by the time clarity emerges, the inventory opportunity has passed.

This scenario defines the multi-channel working capital challenge: cash positions that appear healthy on one channel while another starves for capital.

⚠️ Why Multi-Channel Complexity Multiplies

Each sales channel introduces unique working capital variables:

Channel-Specific Cash Flow Variables

Channel

Payout Timing

Hidden Cash Traps

Shopify/DTC

2-day Stripe payouts

8-12% reduction from fees, refunds, chargebacks

Amazon

14-day disbursements

10-20% trapped in reserve holdbacks

Walmart

14-21 day cycles

Compliance-related holds

Wholesale

Net 30-60 terms

90+ days before payment on some orders

Amazon holdbacks can trap €50K+ in reserves precisely during peak season when you need cash for inventory. Wholesale orders require production commitment 90 days before payment arrives. Shopify shows "revenue" in dashboards, but actual cash arrives 8-12% lighter after processor fees and returns.

"One effective strategy to avoid being constrained by cash flow while broadening your product offerings is to start selling wholesale. This approach enables you to transform payment terms into positive cash flow." — u/kiko77777, r/ecommerce Reddit Thread

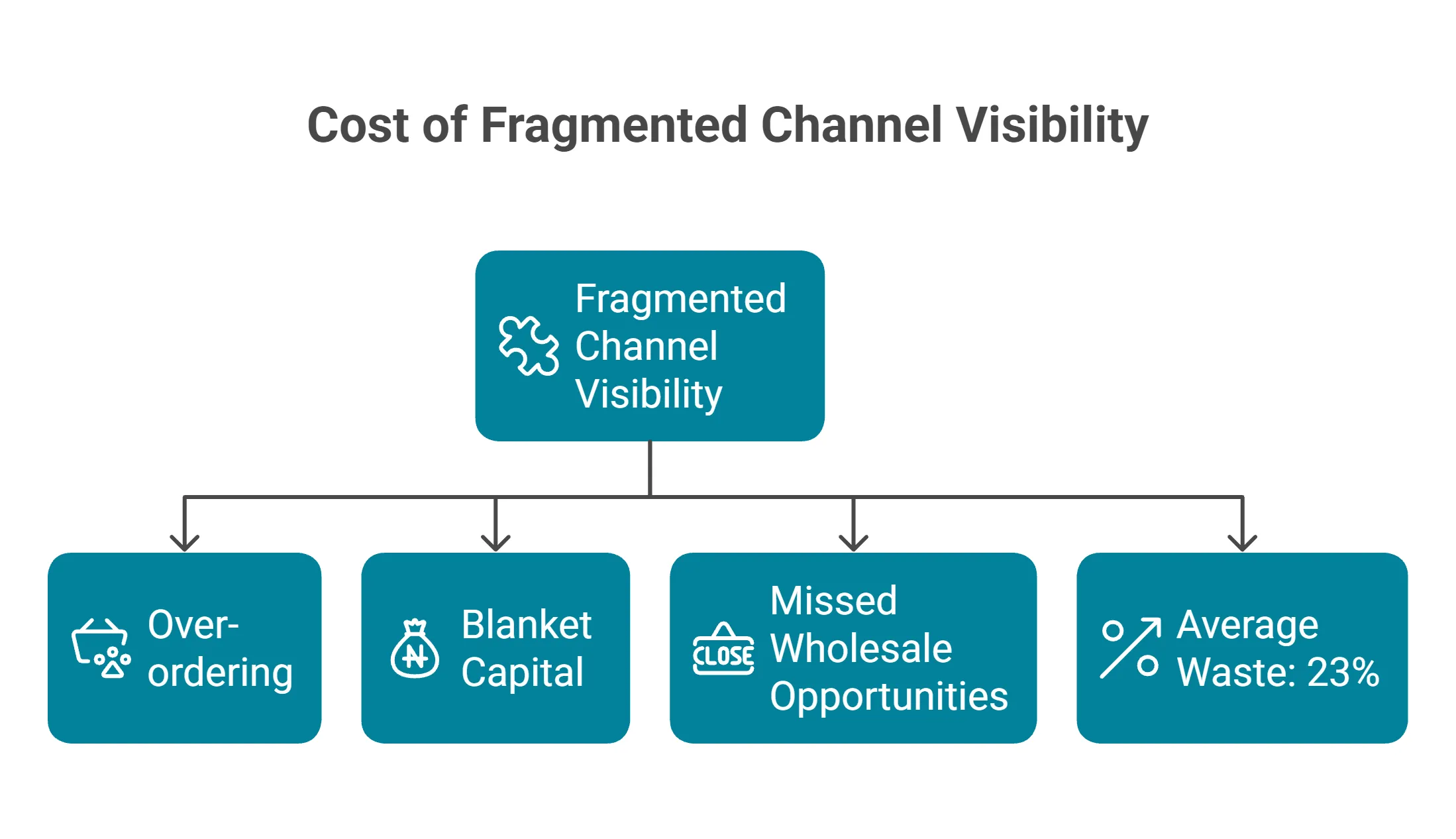

💸 The Cost of Fragmented Channel Visibility

Operating without unified multi-channel cash visibility produces measurable waste:

Diagram illustrating how fragmented multi-channel visibility causes over-ordering, blanket capital decisions, missed wholesale opportunities, and 23% average working capital waste for e-commerce sellers.

Over-ordering for one channel while another stockouts

Blanket capital that ignores channel-specific ROI differences

Missed wholesale opportunities because cash is trapped in Amazon reserves

Average waste: Multi-channel sellers hold 23% more working capital than necessary due to poor cross-channel visibility

"To ensure your store thrives, it's essential to monitor key metrics across platforms, but rather than switching between different tools, consider implementing automated workflows that compile this data." — u/aplchian4287, r/ecommerce Reddit Thread

✅ What Multi-Channel Capital Management Should Look Like

Effective multi-channel working capital management requires:

Unified cash view: Real-time position across all channels with payout timing

Channel-specific margin analysis: Understand true contribution by platform

Automated holdback alerts: Know when marketplace reserves spike

Cross-channel capital recommendations: Deploy where ROI is highest

Without synthesis, founders become the manual integration layer, spending hours reconciling channel data that should flow automatically.

How Luca AI Unifies Multi-Channel Capital Planning

Luca AI connects Shopify, Amazon, Walmart, and wholesale data into a single working capital view. Ask: "What's my cash position across all channels for the next 60 days?" and receive channel-by-channel breakdown with payout timing, holdback status, and margin analysis. Capital recommendations factor in which channel offers the best deployment ROI, ensuring funding flows to highest-return opportunities regardless of platform.

Q8. What Are the Biggest Working Capital Challenges for E-commerce in 2026? [toc=2026 Working Capital Challenges]

The 2026 E-commerce Landscape

The 2026 e-commerce environment presents unprecedented working capital complexity. Trump administration tariffs have increased COGS 15-30% on imported goods. Meta and Google CPMs continue rising (averaging +22% YoY). Interest rates remain elevated. Margins compress from all directions simultaneously, creating a working capital environment that demands real-time visibility, not spreadsheet reconciliation.

"The tariff announcements of 2025 compelled many brands to substantially boost their inventory levels in an effort to maintain margins before tariffs were implemented." — Forbes Finance Council January 2026

⚠️ Four 2026-Specific Working Capital Challenges

2026 E-commerce Working Capital Challenges

Challenge

Impact

Working Capital Implication

Tariff uncertainty

COGS shifts overnight with policy changes

Inventory costing becomes unpredictable

Extended lead times

Supply chain hedging requires ordering further ahead

More capital tied up for longer periods

Marketing cost inflation

Same ROAS requires more absolute spend

Higher cash burn on customer acquisition

Consumer caution

Conversion rates down 8-12% vs. 2024

Extended payback periods on marketing investment

"Three out of four brands are worried about tariff volatility, and many are already adjusting their operations, diversifying suppliers, raising prices, absorbing added costs, and rethinking fulfillment." — Passport 2026 E-commerce Outlook

❌ Why Traditional Tools Can't Keep Pace

Traditional working capital management, spreadsheets reconciling Shopify and Xero data, fails in 2026's volatile environment. By the time last month's cash position is calculated, tariff rates have changed. Standard RBF providers offer capital priced on 60-day-old applications that don't reflect current margin reality.

The architecture of these tools assumes stability that no longer exists. E-commerce founders drowning in data need systems built for volatility, not legacy spreadsheet workflows.

"Revenue-based financing is basically loan sharking for people too early for real loans, but it actually works when you have predictable monthly revenue." — u/anonymous, r/ecommerce Reddit Thread

✅ What 2026 Working Capital Management Requires

The 2026 imperative demands systems capable of:

Real-time margin tracking as COGS shifts with tariff changes

Scenario modeling for multiple tariff outcomes (increase vs. stabilize)

Proactive alerts when CAC inflation erodes campaign profitability

Dynamic capital pricing reflecting current business health, not last quarter's application

How Luca AI Addresses 2026 Volatility

Luca AI's proactive intelligence was architected for exactly this environment. The platform provides real-time margin tracking as COGS fluctuates, scenario modeling for tariff contingencies, automated alerts when marketing efficiency declines, and dynamic capital pricing that reflects today's business health, not outdated snapshots.

When Luca identifies a scaling opportunity, the recommendation is based on current numbers. Capital pricing adjusts as business conditions change. The system that analyzes the opportunity also funds it, with pricing that reflects real-time confidence, not historical applications.

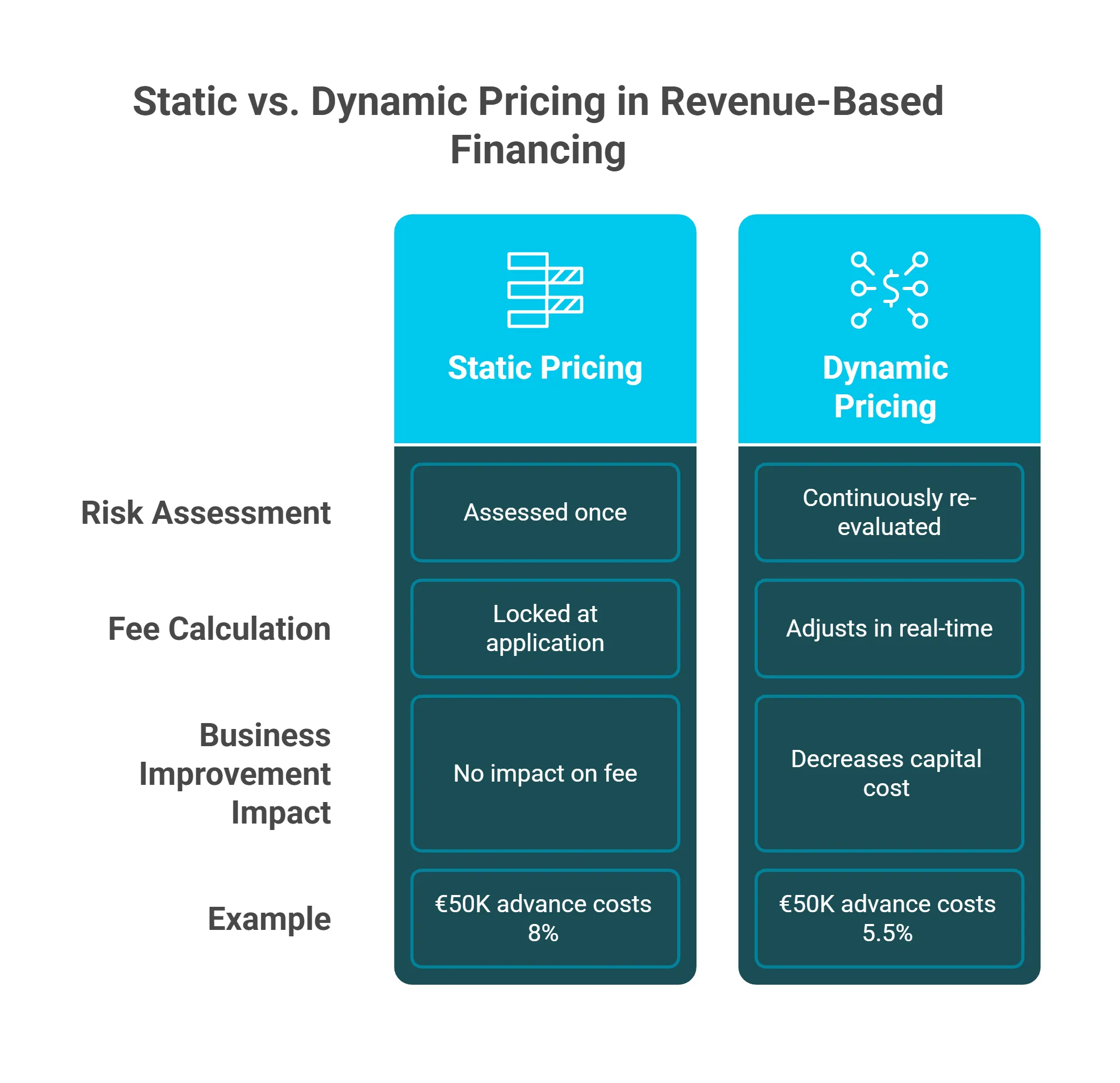

Q9. What Is Dynamic Pricing in Revenue-Based Financing, And Why Waiting Can Mean Cheaper Capital? [toc=Dynamic Pricing Explained]

Dynamic pricing in revenue-based financing means your capital cost adjusts in real-time based on business performance, rather than being locked at application based on a 60-day-old snapshot. This creates a counterintuitive opportunity: improving your business health before taking capital can significantly reduce your financing cost.

Comparison infographic contrasting static and dynamic pricing models in revenue-based financing, showing how dynamic pricing adjusts fees in real-time based on business health improvements.

💰 How Static vs. Dynamic Pricing Works

Traditional RBF providers assess risk once. They pull historical revenue, calculate a fee (typically 6-12% of principal), and lock that rate regardless of whether your business improves next week or next month. The price you see on day one is the price you pay.

Dynamic pricing operates fundamentally differently. The system continuously re-evaluates business health signals. If ROAS improves, margins strengthen, or cash position solidifies, your effective capital cost decreases. The same €50K advance might cost 8% today or 5.5% in three weeks if key metrics improve.

"AI monitors demand, competitor rates, stock levels, and browsing patterns to adjust prices instantly. It reduces excess inventory, boosts margins, and maintains competitive pricing without manual intervention." — u/SweatyCut5414, r/AI_In_ECommerce Reddit Thread

✅ Factors That Improve Your Dynamic Rate

Multiple business health signals influence dynamic capital pricing:

If your capital need isn't urgent (4+ weeks horizon), improving specific metrics before drawing capital can yield 15-30% lower effective cost.

Example scenario: A DTC brand needed €50K for inventory. Initial offer: 9.2% fee. Over three weeks, they improved ROAS from 2.8x to 3.4x through creative optimization. Updated offer: 6.8% fee. Savings: €1,200 on the same €50K draw.

The AI that prices your capital can also show you HOW to reduce that price, identifying which metric improvements would most impact your rate.

"Dynamic pricing, as definition, is offering flexible prices based on changing market conditions and trends. To apply it you should track the market demand and competitors' prices." — u/PrisyncCom, r/econometrics Reddit Thread

How Luca AI Enables Strategic Timing

Luca AI's dynamic pricing reflects its confidence in your growth, the same AI analyzing whether you should take capital also prices that capital based on real-time performance signals.

Better yet, Luca shows you which improvements would reduce your rate: "Improving ROAS to 3.2x would reduce your advance rate from 7.1% to 5.8%. Current trajectory suggests 2-3 weeks." You receive capital guidance AND pricing optimization in one interface through our financial management capabilities.

Q10. How Do You Know If You Need Working Capital Financing Right Now? [toc=Signs You Need Capital]

Score your e-commerce working capital health against these 8 criteria to determine whether financing is critical, beneficial, or premature for your current situation.

📋 Working Capital Health Checklist

Rate your business (check all that apply):

☐ You've identified a winning campaign (ROAS 3x+) but can't increase budget due to cash constraints

☐ Inventory lead times mean ordering now for demand 90+ days away

☐ More than 40% of annual revenue concentrates in Q4 (seasonal dependency)

☐ You've turned down a purchase order or wholesale opportunity due to cash timing

☐ Your cash conversion cycle exceeds 60 days

☐ Marketplace holdbacks (Amazon reserves) exceed 10% of monthly revenue

☐ You're using personal funds or credit cards to bridge cash gaps

☐ Growth rate exceeds your ability to self-fund inventory and marketing

⚠️ Score Interpretation

Working Capital Health Score Guide

Your Score

What It Means

Recommended Action

6-8 checks

❌ Critical need

Working capital financing is essential, you're actively leaving growth on the table and may be damaging business health through constraint

3-5 checks

⚠️ Growth opportunity

Financing could meaningfully accelerate growth; evaluate options and timing strategically

0-2 checks

✅ Currently sufficient

Cash position may be adequate; focus on optimization before taking external capital

Seasonal preparation requiring capital you don't have

Purchase orders you can't fulfill

Expansion opportunities you must decline

"It's tough when market demand is constantly changing and you can't keep up. As a business owner, it's important to adapt to market demands quickly and efficiently." — Industry Analysis

✅ What Luca AI Surfaces Automatically

Luca AI detects these signals through proactive intelligence, alerting you to working capital needs before they become crises. The platform diagnoses which specific use case (inventory, marketing, seasonal) is creating the constraint and presents funding options sized to that specific opportunity.

Scored 4+? The question isn't whether you need capital, it's how much and for what.

Ask Luca: "What's my working capital gap for scaling this quarter?" and receive a specific answer with funding options matched to your situation, in seconds, not spreadsheet hours.

Q11. What Should You Look for in an E-commerce Working Capital Solution in 2026? [toc=Evaluating Capital Solutions]

The 2026 Decision Context

Choosing a working capital solution in 2026 means committing to a financial partner during volatile market conditions. Tariff uncertainty, CAC inflation, and margin compression demand more than capital access, they demand intelligence about whether and how to deploy that capital.

Choose based on rate alone, and you miss the strategic guidance that determines whether funding makes sense given current conditions.

❌ How Most Founders Evaluate (And Why It Fails)

Most founders evaluate working capital providers on headline fee percentage or "fastest approval." This approach ignores critical 2026 questions:

Does the provider understand how tariffs affect your margin?

Can they help determine IF you should take capital given current CAC inflation?

Do they price based on today's business health or last quarter's application?

Will they recommend right-sized amounts, or push maximum available?

"Lack of adequate liquidity leads to business working capital problems that impact procurement, payroll, production, and growth opportunities." — Credlix Working Capital Analysis

✅ The 2026 Evaluation Framework

Score potential providers (0-2 each) on these 8 criteria:

Speed to funding , Hours vs. weeks (critical when opportunities are time-sensitive)

Repayment flexibility , Revenue-linked vs. fixed (essential during volatile periods)

Intelligence layer , Can model cash impact of funding decisions, tariff scenarios

Dynamic pricing , Cost reflects current health, not stale application

Integration depth , Connects to your actual data sources across all channels

Proactive alerts , Surfaces opportunities and risks before you ask

Capital sizing , Recommends right-sized amounts, not maximum available

Scoring guide: 12+ = modern working capital solution. Below 8 = capital without intelligence.

📊 How Luca AI Scores

Luca AI Evaluation Scorecard

Criterion

Score

Why

E-commerce Specificity

✅ 2

Built exclusively for e-commerce

Speed to Funding

✅ 2

Same-day capital deployment

Repayment Flexibility

✅ 2

Revenue-share repayment

Intelligence Layer

✅ 2

Cross-functional reasoning

Dynamic Pricing

✅ 2

Real-time health-based

Integration Depth

✅ 2

20+ data sources

Proactive Alerts

✅ 2

24/7 monitoring

Right-Sizing

✅ 2

Opportunity-matched

Total

16/16

-

"Finance professionals who blend analytical rigor with AI fluency will lead the transformation from data reporting to strategic insight." — AI Finance 2026 Analysis, LinkedIn

The Real Question

The real question isn't "Which provider has the lowest fee?", it's "Which system understands my business well enough to tell me whether I should take capital, how much, and when?" That's the intelligence gap that separates 2026 working capital solutions from legacy financing.

Q12. How Does AI Transform Working Capital from Guesswork to Strategy? [toc=AI-Powered Capital Strategy]

The Fragmented E-commerce Finance Stack

Today's e-commerce finance stack is fundamentally fragmented. Shopify tracks DTC revenue. Amazon Seller Central holds marketplace data. Stripe and PayPal manage payment timing. Xero or QuickBooks handle accounting. Separate banking portals show cash visibility. And yet another application process, disconnected from all of the above, governs capital access.

CFOs become the manual integration layer, spending 15+ hours weekly synthesizing data that should flow automatically. By the time the reconciliation is complete, the opportunity window has often closed. This is exactly why e-commerce founders are drowning in data.

❌ Why Traditional Solutions Fall Short

Traditional solutions address symptoms, not causes.

Analytics dashboards (Triple Whale, Lifetimely, Polar Analytics) show marketing performance but can't model cash impact. They answer "What happened to ROAS?" but not "Can I afford to scale this campaign?"

RBF providers (Wayflyer, Clearco) offer capital but operate as black boxes. Founders receive offers without understanding whether deploying that capital makes financial sense given current margins, inventory position, and growth trajectory.

Intelligence and capital remain siloed, requiring manual triangulation that doesn't scale.

"Triple Whale is an AI-powered ecommerce analytics and attribution platform, commonly used by DTC brands to understand LTV, CAC, and marketing efficiency." — Best AI Tools for Ecommerce 2026

✅ The AI-Era Transformation

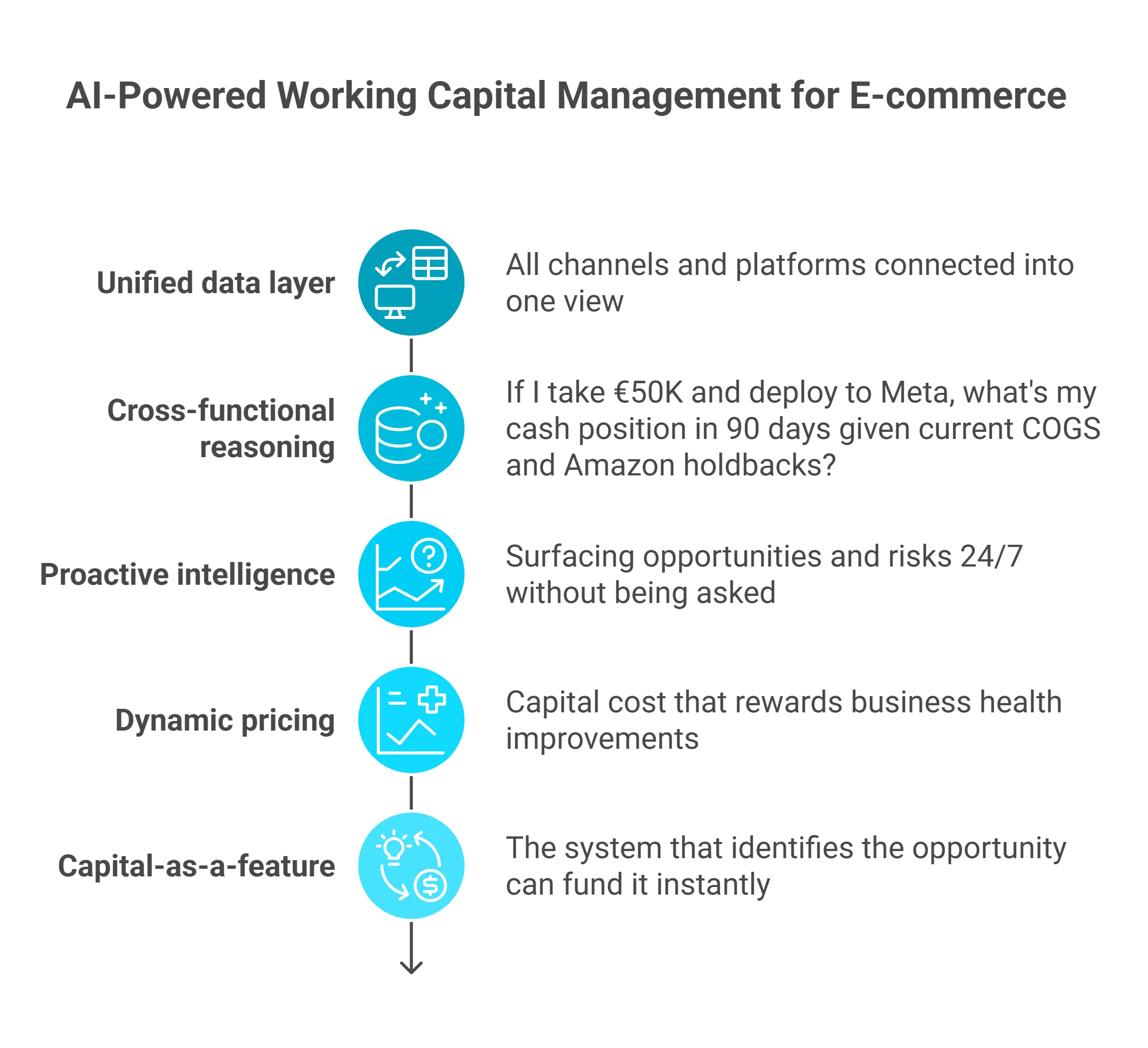

Process flow showing five AI-powered working capital capabilities: unified data layer, cross-functional reasoning, proactive intelligence, dynamic pricing, and instant capital-as-a-feature for e-commerce.

The AI-era shift reframes the fundamental equation: Intelligence without capital is advice. Capital without intelligence is risk.

The competitive advantage in 2026 isn't having data or access to funding, it's having a system that can reason across both to make optimal decisions. The question changes from "Can I get capital?" to "Should I take capital, how much, for what, and when?"

This synthesis was architecturally impossible with siloed tools. It requires a unified system designed from the ground up to connect commerce, marketing, finance, and operations into a single reasoning layer.

"The most intriguing change in 2025 isn't merely that prices shift more quickly; it's that AI pricing is moving from 'undercutting rivals' to 'maximizing margins.'" — u/Claneo, r/AI_In_ECommerce Reddit Thread

Unified data layer: All channels and platforms connected into one view

Cross-functional reasoning: "If I take €50K and deploy to Meta, what's my cash position in 90 days given current COGS and Amazon holdbacks?"

Proactive intelligence: Surfacing opportunities and risks 24/7 without being asked

Dynamic pricing: Capital cost that rewards business health improvements

Capital-as-a-feature: The system that identifies the opportunity can fund it instantly

The Defining Shift

The transformation: from asking your analytics tool "What happened?" then separately applying for capital based on guesswork, to asking Luca "Should I scale this campaign?" and receiving analysis, scenario modeling, funding recommendation, and instant access in one conversation.

How do we calculate exactly how much working capital our e-commerce business needs?

We recommend moving beyond generic industry benchmarks (the typical "15-25% of annual revenue" guidance) to a use-case-specific calculation that reflects your actual business dynamics.

For example, a €5M DTC brand with €150K monthly COGS, 2-month inventory holding, €80K fixed costs, and €50K planned campaign scale would need approximately €510K in working capital, significantly below generic benchmarks.

Channel mix (marketplace holdbacks vs. DTC payouts)

Growth velocity exceeding self-funding capacity

We built Luca AI's financial management capabilities to automate these calculations by synthesizing real-time data from your commerce, payments, and accounting systems, delivering dynamic forecasts that update as conditions change.

What's the difference between revenue-based financing and traditional bank loans for e-commerce?

We see these as fundamentally different financing mechanisms suited to different situations.

Traditional bank loans offer:

Lower headline rates (8-12% APR)

Predictable fixed payments

Business credit building

However, they come with:

6-8 week approval cycles

Personal guarantee requirements

Rigid repayment regardless of revenue fluctuations

Collateral requirements mismatched to asset-light e-commerce

Revenue-based financing provides:

48-72 hour approval and funding

No personal guarantees

Repayments that flex with revenue

No equity dilution

The trade-off is higher effective cost (typically 1.2-1.5x borrowed amount) and static pricing based on application snapshots.

We believe the ideal solution combines RBF speed with intelligence, which is why we built Luca AI to offer dynamic pricing that improves as your business health strengthens, plus strategic guidance on whether the opportunity merits funding.

How does dynamic pricing work in revenue-based financing, and can waiting reduce our capital cost?

Dynamic pricing means your capital cost adjusts in real-time based on current business performance rather than being locked at application based on outdated snapshots.

How it works: Traditional RBF providers assess risk once and lock your rate. Dynamic pricing continuously re-evaluates business health signals. If your ROAS improves, margins strengthen, or cash position solidifies, your effective capital cost decreases.

The strategic patience opportunity: If your capital need isn't urgent (4+ weeks horizon), improving specific metrics before drawing can yield 15-30% lower cost. We've seen brands save €1,200+ on €50K draws by waiting 3 weeks while improving ROAS.

We designed Luca AI's intelligence layer to show you exactly which metric improvements would reduce your rate, turning capital timing into a strategic advantage.

What are the biggest working capital challenges for e-commerce businesses in 2026?

We see 2026 presenting unprecedented working capital complexity from four converging pressures:

1. Tariff Uncertainty Trump administration tariffs have increased COGS 15-30% on imported goods. Policy changes can shift costs overnight, making inventory costing unpredictable.

2. Extended Lead Times Supply chain hedging requires ordering further ahead, tying up more capital for longer periods. Many brands now commit to inventory 90+ days before sales.

3. Marketing Cost Inflation Meta and Google CPMs continue rising (averaging +22% YoY). The same ROAS requires more absolute spend, increasing cash burn on customer acquisition.

4. Consumer Caution Conversion rates are down 8-12% vs. 2024, extending payback periods on marketing investment.

Traditional working capital management (spreadsheets reconciling Shopify and Xero) can't keep pace with this volatility. By the time you calculate last month's position, conditions have changed.

We built Luca AI's proactive intelligence specifically for 2026 volatility: real-time margin tracking, scenario modeling, automated alerts, and dynamic capital pricing reflecting current business health.

How do we know if our e-commerce business needs working capital financing right now?

We've developed an 8-point diagnostic to help you assess your current situation:

Score your business (check all that apply):

☐ Winning campaign (ROAS 3x+) but can't increase budget due to cash constraints

☐ Inventory lead times require ordering 90+ days ahead

☐ More than 40% of revenue concentrates in Q4

☐ Turned down purchase orders or wholesale due to cash timing

☐ Cash conversion cycle exceeds 60 days

☐ Marketplace holdbacks exceed 10% of monthly revenue

☐ Using personal funds or credit cards to bridge gaps

☐ Growth rate exceeds self-funding capacity

Score interpretation:

6-8 checks: Critical need, you're leaving growth on the table

3-5 checks: Financing could meaningfully accelerate growth

0-2 checks: Current cash position may be sufficient

We designed Luca AI to surface these signals automatically through proactive intelligence, alerting you to working capital needs before they become crises and presenting funding options sized to specific opportunities. See how we think about connecting intelligence with capital.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.