Best Startup Business Loans of 2026: Compare Options, Rates, and How to Qualify

14

mins read

In this article

TL;DR

SBA microloans, online lenders, and CDFIs are the top startup loan types in 2026, each with distinct rates, timelines, and eligibility thresholds. Only 31% of sub-$100K-revenue firms receive full funding, so we outline a credit ladder strategy to build qualification over 12 to 24 months. Loan alternatives like grants, ROBS, crowdfunding, and revenue-based financing serve founders who cannot or should not take on traditional debt. E-commerce founders with strong real-time metrics but thin credit histories can bypass traditional underwriting through performance-based capital from Luca AI. We provide a readiness scorecard, total borrowing cost calculator, and industry-specific loan paths so founders apply to the right product the first time.

Q1: What Are Startup Business Loans and How Do Lenders Define 'Startup'? [toc=Definition and Lender Standards]

Startup business loans are financing products designed for businesses typically under two years old that may lack revenue history, established business credit, or collateral. Unlike traditional business loans underwritten against years of financial statements, startup loans rely heavily on personal credit scores, business plans, and projected cash flow, making the application process fundamentally different from what established businesses experience.

How Lenders Define 'Startup'

There is no universal definition. Most lenders classify a business as a "startup" if it has been operating for fewer than 24 months, though some online lenders accept applications from businesses with as little as three months of operating history. The SBA uses industry-specific size standards rather than a fixed age threshold, but its microloan program is explicitly designed for early-stage businesses.

⏰ Time in business: Most traditional lenders require 2+ years; online lenders often accept 6 to 12 months; SBA microloans and CDFIs may work with businesses under 6 months old

💰 Revenue thresholds vary widely: From $0 (Kiva, some CDFIs) to $100,000+ annual revenue (OnDeck, Fundbox)

Personal credit carries outsized weight: Without established business credit, lenders rely almost entirely on personal credit scores, ranging from no minimum (Kiva) to 680+ for SBA 7(a) approval

Business plans replace financials: Where established businesses submit tax returns and P&L statements, startups are judged on projected cash flow, market analysis, and the founder's industry experience

The 2026 Lending Landscape

The Federal Reserve's 2025 Small Business Credit Survey found that 45% of small employer firms applied for financing, the highest rate since 2021, with a full-funding rate of 46%. However, revenue dramatically influences outcomes: firms earning under $100,000 annually had a 31% full-funding rate, while those earning $1M to $10M reached 61%.

On the SBA side, FY2025 saw approximately 77,600 SBA 7(a) loans totaling $37 billion, with over 80% of approvals going to loans under $500,000. The average SBA microloan disbursement rose to $16,131 in FY2025, up from roughly $13,000 in prior years. However, Q1 FY2026 was disrupted by the longest federal government shutdown in U.S. history (October 1 to November 12, 2025), which halted SBA E-Tran completely and reduced approvals by 48% year-over-year for the quarter.

Who Should Consider a Startup Loan

Startup loans make sense when you need capital to launch or scale but want to avoid diluting equity. They are most appropriate when you have a clear use of funds (inventory, equipment, marketing), can demonstrate creditworthiness through personal credit, and have a realistic repayment plan. If you cannot meet even the most flexible lender requirements, alternatives like grants, crowdfunding, or bootstrapping may be a better starting point.

For e-commerce founders preparing loan applications, Luca AI simplifies the readiness assessment by extracting real-time revenue, margin, and cash flow data directly from connected platforms like Shopify and Xero, presenting a consolidated financial picture and pushing automated readiness reports to Slack or email, replacing the manual spreadsheet reconciliation that typically consumes hours of preparation time.

Q2: Who Are the Best Startup Business Loan Providers in 2026? [toc=Best Loan Providers 2026]

Choosing the right startup loan provider matters as much as choosing the right loan type. Below are the best startup business loan providers of 2026, ranked by rate competitiveness, funding speed, credit flexibility, and borrower-friendliness.

1. Luca AI: Best for E-commerce Startups

Luca AI offers dynamically-priced capital with same-day disbursal for e-commerce and DTC founders. Rather than static credit applications, Luca underwrites based on live business performance data from connected Shopify, Stripe, and Xero accounts, meaning pricing reflects your current trajectory, not a snapshot from 60 days ago. No personal guarantee required. Revenue-responsive repayment adjusts to your actual cash flow, eliminating the rigid weekly or monthly payment schedules that strain startup budgets. The entire process, from data connection to capital deployment, takes minutes, not weeks.

✅ Ideal for: E-commerce and DTC founders with connected commerce data who need capital deployed in hours, not weeks.

2. OnDeck: Best for Short-Term Working Capital

OnDeck provides term loans from $5K to $500K and lines of credit up to $200K with repayment terms of 12 to 24 months. Minimum credit score of 600 and at least one year in business with $100,000 annual revenue required. Fast approval (often within one business day), but the average interest rate runs high. Bankrate reports an average of 57.9% APR for term loans.

3. Fundbox: Best for New Businesses Needing Flexible Credit

Fundbox offers business lines of credit up to $150,000 to $250,000 with 12- or 24-week terms and weekly repayment. Starting draw fee of 4.66% for 12-week terms. Requires just 3 months in business, $100,000 annual revenue, and a 600 credit score.

4. Kiva: Best for Pre-Revenue Founders

Kiva provides genuinely 0% APR microloans from $1,000 to $15,000 with zero origination fees, zero maintenance fees, and no minimum credit score. Repayment terms range from 12 to 36 months. The catch: borrowers must raise initial support from 5 to 40 personal network members before accessing the broader Kiva platform. Repeat borrowers automatically qualify for at least double their first loan amount.

5. Accion Opportunity Fund: Best for Underserved Founders

A CDFI lender focused on minority-, women-, and veteran-owned businesses. Flexible credit requirements and below-market rates, with technical assistance and mentorship included. Ideal for founders who may not meet traditional credit thresholds but have strong business fundamentals.

6. Taycor Financial: Best for Equipment Purchases

Specializes in equipment financing with asset-backed lending. The equipment itself serves as collateral, making approval easier for startups without other assets. Best suited for businesses needing machinery, vehicles, or technology hardware.

7. Bank of America: Best for Strong-Credit Founders

As an SBA Preferred Lender, Bank of America offers the lowest rates but the strictest requirements. Best for founders with 680+ credit scores, established banking relationships, and patience for longer approval timelines.

8. Lendzi: Best for Loan Shopping

A marketplace that matches borrowers with 75+ lenders, offering access to term loans up to $5M, lines of credit, and SBA loans through a single application. Useful for comparing multiple offers without multiple hard credit pulls.

9. Fora Financial: Best for Low-Credit Borrowers

Accepts credit scores as low as 500 with fast funding (often within 72 hours). Trade-off: higher rates reflecting the increased risk profile. Best for founders who need immediate capital and cannot wait for SBA or bank approval timelines.

Master Comparison Table

Best Startup Business Loan Providers 2026

Provider

Type

APR Range

Max Amount

Min Credit

Funding Speed

Collateral

Best For

Luca AI

Dynamic capital

Varies by health

Varies

None (data-based)

Same day

❌ No

E-commerce/DTC startups

OnDeck

Term loan / LOC

29.9% to 97.3%

$500K

600

1 to 3 days

❌ No

Short-term working capital

Fundbox

Line of credit

4.66%+ draw fee

$250K

600

1 to 3 days

❌ No

New businesses, flexible draws

Kiva

Microloan

0%

$15K

None

30 to 60 days

❌ No

Pre-revenue founders

Accion

CDFI loan

7% to 20%

$250K

Flexible

2 to 4 weeks

Varies

Underserved founders

Taycor

Equipment loan

5.99%+

$2M

550

1 to 5 days

✅ Equipment

Equipment purchases

Bank of America

SBA / term loan

SBA rates

$5M

680

2 to 8 weeks

✅ Often

Strong-credit borrowers

Lendzi

Marketplace

Varies

$5M

500

Varies

Varies

Loan comparison shopping

Fora Financial

Short-term loan

Factor rate 1.1+

$750K

500

1 to 3 days

❌ No

Low-credit, fast funding

Traditional revenue-based financing providers often present a contrasting experience. One Wayflyer borrower described the underwriting process:

"We handed them two stores' performance data on a platter, clean revenue, consistent orders, clear repayment strength. Any real underwriting team would look at those numbers and go, 'Yep, easy approval.' Instead, it turned into this bizarre slow-motion loop where nobody seemed to understand what they were looking at." Gemma Wayflyer - Trustpilot Verified Review

Another founder highlighted the broken promises common in the space:

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues, this was incredibly disappointing." Joshua Hannan Wayflyer - Trustpilot Verified Review

And the contract terms themselves can catch founders off guard:

"Read their terms and contract carefully! They said their offer is not secured, which is false; they still will file UCC. They can deem you in default for any reason at their discretion... the worst bank agreement I have read in 25 years." Zachary Piech, Owner of ValuePetSupplies.com Wayflyer - Trustpilot Verified Review

Q3: What Types of Startup Loans Can You Apply For? [toc=Startup Loan Types]

Startup loans fall into 11 distinct product categories, each with different rate structures, repayment mechanics, and eligibility requirements. The right type depends on your credit score, revenue status, collateral availability, and how quickly you need funds.

SBA 7(a) Loans

The SBA's flagship program offers up to $5M with terms up to 25 years and variable rates of approximately Prime + 2.25% to 4.75%. FY2025 saw roughly 77,600 approvals totaling $37 billion. Most lenders require 2+ years in business and 680+ credit. See Q4 for a full deep-dive.

SBA Microloans

Up to $50,000 (average disbursement: $16,131 in FY2025) at 8% to 13% APR through nonprofit CDFI intermediaries. Maximum 6-year repayment term. Includes free business training and technical assistance. The most startup-friendly SBA product.

Term Loans

Lump-sum financing repaid on a fixed schedule over 12 to 60 months. Available from banks (lower rates, stricter requirements) and online lenders (higher rates, faster approval). Amounts range from $5K to $5M depending on the lender.

Business Lines of Credit

Revolving credit you draw from as needed; interest accrues only on the amount drawn. Ideal for managing working capital gaps, seasonal inventory, or unpredictable expenses. Fundbox offers 12- or 24-week terms starting at a 4.66% draw fee.

Equipment Financing

The equipment you purchase serves as collateral, making approval easier for startups without other assets. Financing covers up to 100% of equipment cost with terms matching the equipment's useful life.

Online Lender Loans

Faster approval (1 to 7 days) with lower credit floors (some accept 500+), but significantly higher rates. OnDeck's average term loan APR reaches 57.9% according to Bankrate data. Best when speed outweighs cost concerns.

CDFI Loans

Community Development Financial Institutions serve underbanked founders with flexible credit requirements, below-market rates, and technical assistance. Often the bridge between "too early for banks" and "too expensive from online lenders."

Invoice Factoring

Not technically a loan. You sell outstanding invoices to a factoring company at a discount (typically 1% to 5% per month) and receive 80% to 90% of the invoice value upfront. Best for B2B startups with creditworthy customers and slow-paying accounts.

⚠️ Merchant Cash Advances (Last Resort)

A percentage of daily credit card or debit sales is collected until the advance plus fees is repaid. Factor rates of 1.1 to 1.5 translate to effective APRs of 40% to 350%. No credit score requirement, but the most expensive startup financing option by a wide margin.

Peer-to-Peer Lending

Platform-based lending (Prosper, LendingClub) connects borrowers with individual investors. Variable rates, less regulated than bank lending, and credit requirements vary by platform.

Nonprofit Microloans (Non-SBA)

Community lenders like Grameen America and Kiva offer below-market or zero-interest microloans. Kiva provides $1K to $15K at genuinely 0% APR with no fees and no credit score requirement.

Master Product Comparison

Startup Loan Types Comparison

Loan Type

Best For

Amount Range

Typical APR

Speed

Min Credit

Collateral

Key Risk

SBA 7(a)

Working capital, real estate

$5K to $5M

11.5% to 16.5%

2 to 3 months

680+

Often required

Slow approval

SBA Microloan

Early-stage startups

$500 to $50K

8% to 13%

2 to 4 weeks

620+

Rarely

Small amounts

Term Loan

Defined capital needs

$5K to $5M

9% to 99%

1 to 60 days

600+

Varies

Rate range

Line of Credit

Cash flow management

$6K to $250K

4.66%+ fee

1 to 7 days

600+

❌ No

Short terms

Equipment

Machinery, vehicles

Up to $2M

5.99%+

1 to 5 days

550+

✅ Equipment

Asset-specific

Online Lender

Speed-priority borrowers

$5K to $500K

29% to 97%

1 to 3 days

500+

❌ No

Very high cost

CDFI

Underserved founders

$500 to $250K

7% to 20%

2 to 4 weeks

Flexible

Varies

Limited availability

Invoice Factoring

B2B with receivables

80% to 90% of invoices

1% to 5%/month

1 to 7 days

500+

✅ Invoices

Customer-dependent

MCA ⚠️

Absolute last resort

$5K to $500K

40% to 350%

1 to 3 days

None

❌ No

Extreme cost

P2P Lending

Alternative credit paths

$1K to $50K

7% to 36%

1 to 2 weeks

600+

❌ No

Less regulated

Nonprofit Microloan

Pre-revenue, low credit

$1K to $15K

0% to 8%

2 to 8 weeks

None

❌ No

Small amounts

Luca AI offers a distinct product structure positioned between traditional term loans and revenue-based financing, with dynamically-priced capital, same-day disbursal, and revenue-responsive repayment. Unlike the static loan products above, Luca's pricing adjusts in real time based on current business performance rather than a credit application filed weeks ago.

Q4: How Do SBA Loans Work for Startups? [toc=SBA Loans Explained]

The most important misconception to clear up immediately: the SBA does not lend money directly. Instead, it guarantees 50% to 85% of loans made by SBA-approved lenders, reducing lender risk and enabling better terms for startups that would otherwise be denied. This guarantee mechanism is why SBA loans consistently offer the lowest rates available to new businesses.

SBA 7(a): The Flagship Program

The 7(a) is the SBA's most popular loan product, approving approximately 77,600 loans totaling $37 billion in FY2025. Key parameters:

💰 Maximum amount: $5M

Terms: Up to 25 years (real estate), 10 years (working capital/equipment)

Rates: Variable, typically Prime + 2.25% to 4.75% (average initial rate fell to 9.79% in Q1 FY2026, down from 11.16% at the Q1 FY2024 peak)

Credit floor: Most lenders require 680+, though some (like U.S. Bank) show flexibility

Collateral: Required for loans above $25K when available

Startup-friendliness: ⭐⭐ Typically requires 2+ years in business, though exceptions exist with strong business plans and industry experience

Over 80% of FY2025 7(a) approvals were for loans under $500,000, and more than half were under $150,000, reflecting the SBA's push to serve smaller borrowers.

SBA Microloan: The Startup Entry Point

The SBA Microloan program is explicitly designed for startups and early-stage businesses:

💰 Maximum amount: $50,000 (average disbursement: $16,131 in FY2025)

Terms: Up to 6 years

Rates: 8% to 13% APR

Credit floor: 620+ generally accepted; CDFIs may show flexibility with strong business plans

Collateral: Rarely required for smaller amounts

Startup-friendliness: ⭐⭐⭐⭐⭐ Purpose-built for new businesses

✅ Bonus: Includes free business training and technical assistance from the intermediary lender

Microloans are administered by nonprofit CDFI intermediaries, not banks, which makes them more accessible to founders with limited credit history.

SBA 504: Real Estate and Heavy Equipment

💰 Maximum amount: $5.5M

Purpose: Strictly for real estate purchases and major equipment

Requires: 10% down payment from the borrower

Startup-friendliness: ⭐⭐ Narrowest use case; limited relevance for e-commerce or service businesses

Decision Matrix

SBA Loan Program Comparison

Dimension

SBA 7(a)

SBA Microloan

SBA 504

Max Amount

$5M

$50K

$5.5M

Typical Approval Time

2 to 3 months

2 to 4 weeks

2 to 3 months

Credit Floor

680+

620+

680+

Collateral

Often required

Rarely required

Required (10% down)

Best Use Case

Working capital, expansion

First institutional loan

Real estate, heavy equipment

Startup-Friendliness

⭐⭐

⭐⭐⭐⭐⭐

⭐⭐

How to Apply for an SBA Loan

Find an SBA-approved lender via the SBA Lender Match tool, or contact a CDFI intermediary for microloans

Prepare your business plan with 12-month financial projections, market analysis, and a specific use-of-funds statement

Gather documents: Personal tax returns (2 years), bank statements (3 to 6 months), EIN, business formation documents, SBA Form 1919 (Borrower Information Form), SBA Form 912 (Statement of Personal History)

Submit and undergo underwriting with 2 to 4 weeks for microloans and 2 to 3 months for 7(a)

Close and receive funds

For e-commerce founders, SBA microloans often serve as the ideal first institutional loan, building the repayment history and business credit needed to qualify for larger SBA 7(a) or competitive online loans within 12 to 18 months. The average microloan of roughly $16,000 can fund initial inventory, a Shopify build-out, or early marketing tests, creating the revenue track record that unlocks larger capital down the road.

Q5: What Do You Need to Qualify and Are You Loan-Ready? [toc=Qualification and Readiness]

Before you apply for any startup business loan, score yourself against the criteria lenders actually evaluate. Each unchecked box below either increases your denial risk or raises your cost of capital.

⭐ Credit Score Tiers and What They Unlock

Your personal credit score is the single most influential factor for startup loans. Since most startups have no established business credit, lenders default to the founder's personal profile.

Your credit score is the single most influential factor for startup loans — each tier unlocks dramatically different products and rates.

Credit Score Tiers and Loan Options

Credit Range

Options Available

Expected Rates

750+

SBA 7(a), premium bank terms

Lowest origination fees, best APR

680 to 749

SBA 7(a), traditional banks, most online lenders

8 to 20% APR

640 to 679

SBA Microloans, broader online access

12 to 30% APR

580 to 639

Online term loans, select LOCs

25 to 50% APR

500 to 579

MCAs, high-cost online lenders only

40 to 100%+ effective APR

Collateral and Personal Guarantees

Collateral dramatically improves approval odds and reduces rates. Common collateral includes real estate, equipment, inventory, and business bank balances. If you lack collateral, most lenders will require a personal guarantee, meaning your personal assets (home, savings) are at risk if the business defaults. SBA loans above $25,000 typically require collateral when available, and virtually all SBA loans require a personal guarantee.

⚠️ A UCC (Uniform Commercial Code) lien gives the lender a legal claim on your business assets. Some lenders, including certain revenue-based financing providers, file blanket UCC liens covering all business property, not just the financed amount.

✅ The 10-Point Loan Readiness Scorecard

☐ Personal credit score is 640+ (or you know your exact score and have pulled your report)

☐ You can articulate exactly how much capital you need and the specific use of funds

☐ You have 3+ months of business bank statements showing consistent activity

☐ Your business plan includes 12-month financial projections with realistic assumptions

☐ You have calculated startup costs by category (equipment, inventory, legal, operating, and working capital)

☐ You understand your Debt Service Coverage Ratio and can show 1.25x coverage

☐ You have identified collateral or are prepared to sign a personal guarantee

☐ You know whether SBA, online, or alternative lending fits your timeline and credit profile

☐ You have an EIN, business formation documents, and required licenses/permits

☐ You have researched at least 3 lenders and compared their terms

Score Interpretation

Loan Readiness Score Interpretation

Your Score

What It Means

Recommended Path

⭐ 8 to 10 checks

Strong application

Target SBA 7(a) or competitive online rates

5 to 7 checks

Gaps exist

Focus on SBA Microloans or CDFIs while strengthening weak areas

3 to 4 checks

Significant gaps

Apply to flexible online lenders or Kiva while building fundamentals

❌ 0 to 2 checks

Not loan-ready

Consider bootstrapping, grants, or credit-building strategy first

Q6: How Do You Apply for a Startup Business Loan Step by Step? [toc=Application Process]

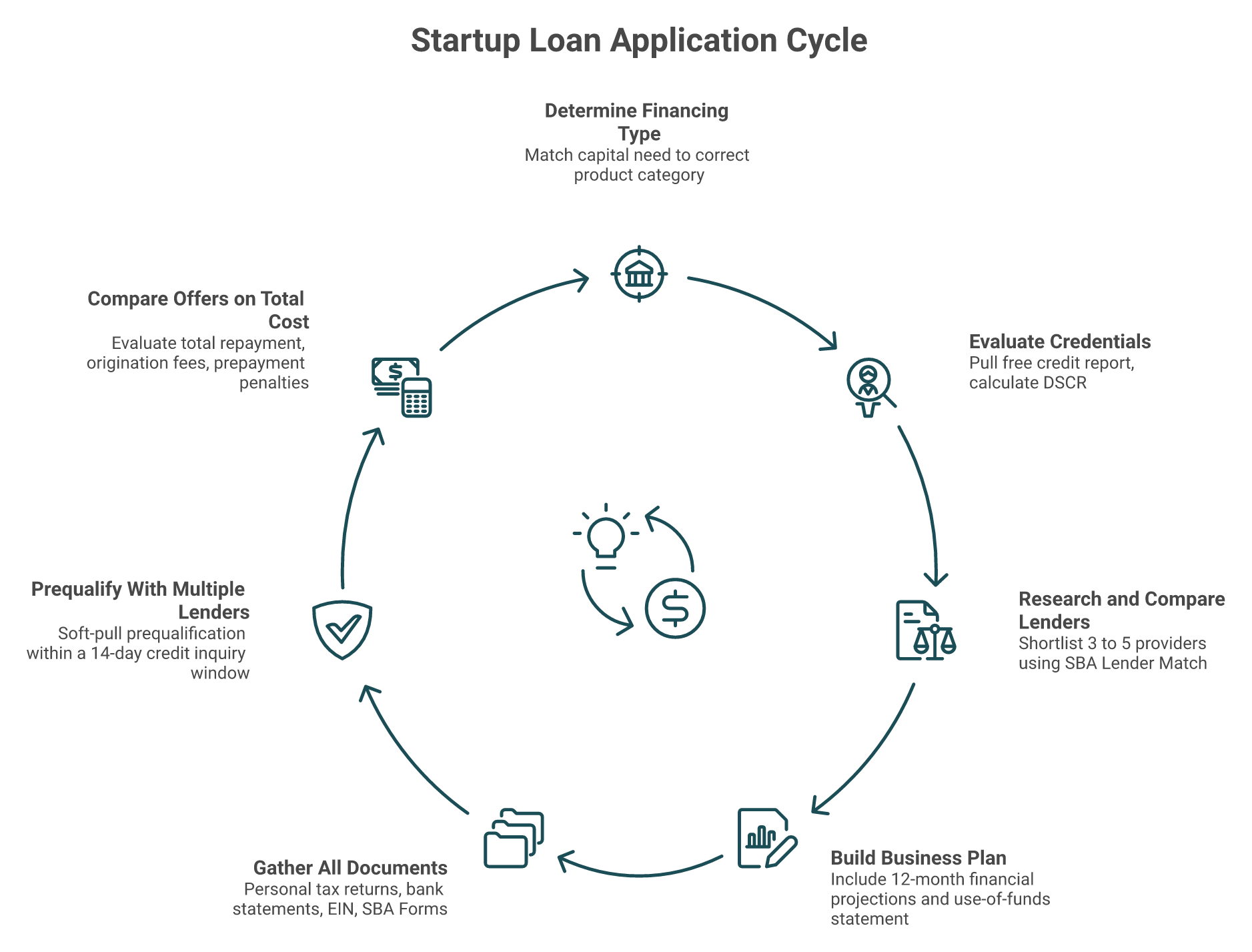

The startup loan application process follows seven distinct steps, though the timeline ranges from same-day to three months depending on the loan type you pursue.

The startup loan application follows seven distinct steps — skipping or rushing any phase is the most common cause of avoidable denials.

Step 1: Determine Your Financing Type

Match your capital requirement to the right loan product. Use the startup costs breakdown from your readiness scorecard (Q5) and cross-reference with the product taxonomy in Q3. A founder needing $15,000 for initial inventory has no business applying for an SBA 7(a). An SBA microloan or Kiva loan is faster, cheaper, and better suited to the amount.

Step 2: Evaluate Your Credentials

Pull your free credit report from AnnualCreditReport.com. Calculate your Debt Service Coverage Ratio (monthly net operating income ÷ projected monthly payment ≥ 1.25). Identify which scorecard items from Q5 you need to address before applying.

Step 3: Research and Compare Lenders

Use SBA Lender Match for SBA loans. For online lenders, shortlist 3 to 5 providers from the ranked comparison in Q2. As one Reddit founder learned the hard way, vetting your lender matters:

"I will be very careful with who I work with. I will be asking for a list of everything they will be requiring up front, I will be vetting the person at that particular bank by asking for references." u/deleted, r/smallbusiness Reddit Thread

Step 4: Build Your Business Plan

Include 12-month financial projections, a specific use-of-funds breakdown, and market analysis. Lenders want to see exactly how capital translates to revenue. One founder who secured a pre-revenue SBA loan noted: the business plan detail level was what made the difference.

Step 5: Gather All Documents

Use the organized checklist from Q5. Incomplete document packages are the number-one cause of delayed SBA approvals. Have everything assembled before you initiate contact with any lender.

⏰ Step 6: Prequalify With Multiple Lenders

Most online lenders and SBA Lender Match offer soft-pull prequalification that won't impact your credit score. Apply within a 14-day window. Credit bureaus treat multiple inquiries for the same loan type within this period as a single inquiry.

Step 7: Compare Offers on Total Cost

Never evaluate a loan on headline APR alone. Compare total cost of capital (see Q7), including origination fees, repayment frequency impact, and prepayment penalties.

Approval Timeline by Loan Type

Approval Timeline by Loan Type

Loan Type

Typical Approval

Funding Speed

Online lenders

1 to 3 days

1 to 7 days

SBA Microloans

2 to 4 weeks

2 to 4 weeks

SBA 7(a)

4 to 8 weeks

2 to 3 months

Traditional banks

2 to 4 weeks

4 to 8 weeks

Luca AI

Same day

Same day

⚠️ Common Mistakes That Kill Applications

Applying for more than you need, which increases cost and raises denial risk

Submitting incomplete document packages

Not shopping multiple lenders for competing offers

Ignoring factor rate vs. APR conversion. A 1.3 factor rate on 6 months is roughly 60% APR

Not reading prepayment penalty clauses

Applying for the wrong loan type entirely

For e-commerce founders, Luca AI collapses this seven-step process into one: connect your Shopify, Stripe, and Xero accounts, and Luca underwrites based on live business data, bypassing weeks of document gathering and manual lender comparison. Funding deploys the same day, with no separate application form required.

Q7: What Does a Startup Loan Actually Cost? (Total Borrowing Cost Analysis) [toc=Total Borrowing Cost]

Most startup loan comparison articles list APR ranges but never show what you actually pay in total dollars. A $50,000 loan at "15% APR" and a $50,000 loan at "1.3 factor rate" sound like they belong in the same conversation, but the second can cost two to four times more. The startup lending industry profits from this confusion.

The Factor Rate Trap: With Real Math

A factor rate is a decimal multiplied by your loan principal to determine total repayment. A 1.3 factor rate on $50,000 over 6 months means you pay back $65,000. That is $15,000 in fees, translating to roughly 60% effective APR.

Now add common hidden costs:

💸 Origination fees: 0.5 to 6% of the loan amount ($250 to $3,000 on a $50K loan)

Draw fees on lines of credit (each time you access funds)

Prepayment penalties, as some lenders charge you for paying early

UCC filing fees ($50 to $200)

Late payment fees ($15 to $50 or 5% of the missed payment)

Weekly repayment impact, since paying weekly instead of monthly reduces the effective time you hold capital, inflating true cost further

As one founder recently noted on Reddit about shopping for small business loans:

"One company offered me the money today but the 'factor rate' they quoted works out to like 45% APR when I did the math." u/bongsandsongsaz, r/loansforsmallbusiness Reddit Thread

💰 Total Cost Comparison: $50,000 Across 5 Loan Types

Total Cost Comparison: $50,000 Across 5 Loan Types

Loan Type

Rate/Fee

Term

Total Interest/Fees

Total Repayment

Monthly Payment

Effective APR

SBA Microloan

8% APR

5 years

~$10,830

~$60,830

~$1,014

~8.3%

Online Term Loan

25% APR + 3% orig.

2 years

~$15,300

~$65,300

~$2,721

~27%

Business LOC

18% APR (drawn)

1 year revolving

~$9,000 (if fully drawn)

~$59,000

Varies

~18%

Revenue-Based Financing

12% flat fee

Varies with revenue

$6,000

$56,000

Revenue-linked

15 to 45%

⚠️ Merchant Cash Advance

1.4 factor rate

6 months

$20,000

$70,000

~$11,667

~80%

The difference between the cheapest option (SBA Microloan at ~$10,830 in total interest) and the most expensive (MCA at $20,000 in fees) is $9,170 on the same $50,000 principal, nearly a 2x cost differential.

On the same $50,000 principal, the cheapest loan type costs $10,830 in interest while the most expensive charges $20,000 in fees — a gap invisible in APR ranges alone.

The 36% Affordability Rule

Before borrowing, verify affordability: total monthly debt payments (including the new loan) should not exceed 36% of gross monthly revenue.

Worked example:

Monthly revenue: $15,000

36% cap: $5,400/month maximum total debt service

Existing obligations: $1,500/month

Maximum new loan payment: $3,900/month

Calculating Your DSCR

Most lenders require a minimum 1.25x Debt Service Coverage Ratio: monthly net operating income ÷ monthly debt payment ≥ 1.25.

Example: A startup with $12,000 monthly revenue and $8,000 monthly expenses has $4,000 in net operating income, supporting a maximum monthly loan payment of $3,200 ($4,000 ÷ 1.25).

Luca AI eliminates the cost-comparison guesswork for e-commerce founders. Because Luca's capital is dynamically priced based on real-time business health, the rate reflects current performance, not a static credit snapshot from weeks ago. Transparent, all-in pricing with no origination fees, no hidden charges, and revenue-responsive repayment means you always know your total cost of capital before you commit.

Q8: Which Loan Fits Your Industry and How Are Real Founders Using Them? [toc=Industry Loan Fit]

Cecil & Lou, an e-commerce children's apparel brand, used Clearco's revenue-based funding to finance $500,000 in inventory within three days, enabling a complete business model shift from auction-style sales to in-stock inventory that now accounts for 60% of their revenue.

Industry-Specific Loan Paths

Recommended Loan Types by Industry

Industry

Recommended Loan Type

Why It Fits

E-commerce/DTC

Revenue-based financing or SBA Microloan

Fast deployment, scales with revenue, ideal for inventory + ad spend

SaaS

Business line of credit

Draw against ARR growth, flexible repayment

Restaurant/Food

SBA 7(a) + equipment financing

Long terms for buildout + kitchen equipment

Retail/Brick-and-Mortar

SBA 504 + working capital line

Real estate financing + cash flow management

Service-Based

SBA Microloan or personal LOC

Lower capital needs, no inventory burden

Construction/Healthcare

Equipment financing + SBA 7(a)

Heavy asset purchases, licensing costs

Case Study #1: E-commerce: From Auction Model to Inventory-Led Growth

Cecil & Lou's founders had proven demand through pre-sale auctions but couldn't build inventory without upfront capital. Traditional banks offered a maximum $150,000 line of credit, which was insufficient for a brand processing hundreds of orders daily. By using Clearco's invoice funding, they deployed $500,000 in three days, repaid as inventory sold, and carried no long-term debt. The lesson: for product-based e-commerce, the speed of capital deployment directly determines whether you capture demand or lose it to competitors.

Case Study #2: Service Business: SBA Microloan Through a CDFI

A contracting firm owner with damaged personal credit found that banks dismissed the application entirely, while online lenders quoted rates exceeding 40%. The breakthrough came through a local nonprofit CDFI offering SBA microloans:

"What ultimately succeeded was an SBA microloan from a local nonprofit CDFI. It took about six weeks, but the interest rate was below 10% and the repayment terms were fair. They focused more on the business's viability than on my credit score." u/otlucenie, r/loansforsmallbusiness Reddit Thread

The contrast is instructive: Cecil & Lou needed speed and scale (revenue-based financing); the contractor needed affordability and credit flexibility (CDFI microloan). The "best" loan depends entirely on your industry context and primary constraint.

⚠️ The Cautionary Pattern

Founders who choose the wrong loan type for their industry pay the price. One Reddit user was offered an $11,000 MCA at a 1.48 factor rate, roughly 105% annualized, for a business that likely qualified for an SBA microloan with patience:

"$11,000 at 1.48 factor rate, 110 total payments... roughly 105% annualized. These are what we could consider to be a D-paper, or high-risk deal. Both of these deals are shit that only benefit the broker and funder." u/deleted, r/smallbusiness Reddit Thread

The Optimal E-commerce Funding Sequence

For Shopify/DTC founders specifically, the capital ladder follows a predictable path:

Month 0 to 6: SBA Microloan or Kiva ($1K to $50K) for initial inventory and setup

Month 6 to 12: Business line of credit once consistent revenue is established for cash flow management

Month 18+: SBA 7(a) or competitive term loan for larger growth investments

Luca AI compresses this multi-year funding sequence into a single relationship for e-commerce founders. With same-day disbursal, rates that adjust based on live business performance, and revenue-responsive repayment matching your cash flow cycle, Luca replaces the manual process of graduating between lenders as your business grows. One capital partner from first inventory order to scaled Q4 campaigns, the path Cecil & Lou had to build across multiple providers over years.

Q9: What If Your Startup Loan Application Is Denied? [toc=Denied Application Recovery]

You spent three weeks gathering documents, wrote a detailed business plan, applied for an SBA microloan, and got denied. The rejection email offers no specifics, just "does not meet criteria at this time." You're back to square one with less confidence and no clearer path forward. This is among the most common startup loan outcomes. The Federal Reserve's 2024 Small Business Credit Survey found that firms under $100,000 in annual revenue had only a 31% full-funding rate, and almost no guide tells you what to do next.

❌ Why Applications Get Denied

The most common denial reasons, each with a specific fix:

Common Denial Reasons and How to Fix Them

Denial Reason

How to Fix It

Insufficient time in business (<6 months)

Apply to Kiva (no time requirement) or CDFIs while building operating history

Personal credit score below threshold

Open a secured credit card, pay down utilization below 30%, and dispute errors on your report

Inadequate revenue documentation or zero revenue

Start generating revenue first, even small amounts; track all transactions through a dedicated business bank account

No collateral for secured products

Pivot to unsecured options (Kiva, online lenders, and SBA microloans)

Industry classified as high-risk

Seek CDFIs or specialized lenders in your vertical

Wrong loan type for your profile

Match your profile to the product taxonomy in Q3; don't request SBA 7(a) when a microloan fits

Incomplete document package or weak projections

Use the Q5 checklist; have a SCORE mentor review your business plan before resubmitting

One denied founder's first move was instructive:

"Ask your loan officer; they should tell you how to get it approved or what you need. They should have done this before you even really submitted." u/deleted, r/smallbusiness Reddit Thread

💰 The Funding Sequencing Strategy (Credit Ladder)

Instead of waiting 18 months until you qualify for your ideal loan, build a capital ladder:

A loan denial is not a dead end — this credit ladder sequences five products over 18 to 24 months to build the exact profile lenders require.

Month 1 to 3: Open a secured business credit card to establish business credit + apply for a Kiva 0% microloan ($1K to $15K)

Month 3 to 6: Use consistent card payments to register a DUNS number with Dun & Bradstreet and build an Experian Business credit profile

Month 6 to 9: Apply for an SBA microloan through a CDFI with 6 months of bank statements and credit card repayment history

Month 12 to 18: Use microloan repayment track record to qualify for a business line of credit

Month 18 to 24: Graduate to SBA 7(a) or competitive online term loan with established business credit + revenue history

How Startup Loans Affect Your Credit

⚠️ Hard inquiries: Each application creates a 2 to 5 point temporary credit score drop, but multiple inquiries within a 14 to 45 day window are counted as one

Repayment behavior: Since most startup loans require a personal guarantee, on-time payments build both personal and business credit simultaneously

Long-term benefit: 12+ months of on-time repayment significantly strengthens your profile for future borrowing

Building business credit: Register with Dun & Bradstreet (free DUNS number), Experian Business, and Equifax Business; ensure your lender reports to commercial credit bureaus; maintain utilization below 30% on revolving credit

The traditional RBF industry often compounds this denial problem. One Uncapped reviewer described the experience of being stranded:

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M. Then, months later, right as we hit our 5% EBITDA margin, they cut it again to $350K." Xin Shui, CEO/Founder Uncapped - Trustpilot Verified Review

Another reviewer highlighted the opacity of the denial process:

"Wasted 10 days with daily promises that were never kept. Was asked for countless documents to tell me in the end that I don't have enough cash runway to borrow money, absolute nonsense from some underwriter that does not understand e-commerce." A Ovidiu Uncapped - Trustpilot Verified Review

Luca AI offers an alternative path for e-commerce founders who've been denied traditional startup loans. Because Luca underwrites based on real-time business performance data, live Shopify revenue, actual ad performance, and current cash position, rather than static credit applications, founders with strong business fundamentals but thin credit histories can access capital that traditional lenders deny. Same-day disbursal means no 18-month credit-building wait.

Q10: What Are the Best Alternatives If a Startup Loan Isn't Right for You? [toc=Loan Alternatives]

A startup business loan isn't always the right move, and sometimes it's simply not available. Whether you don't qualify, don't want debt, or need capital faster than loan approval timelines allow, these alternatives each serve specific startup scenarios. Some can also be combined with loans as part of a funding stack.

Non-Dilutive Alternatives

⭐ Startup Business Grants

No repayment required, but highly competitive. The SBA's SBIR/STTR programs have historically been the largest federal source ($10K to $5M), though congressional reauthorization is still pending as of early 2026. Private options include the Amber Grant ($10,000 monthly + $25,000 annual prize for women entrepreneurs) and the FedEx Small Business Grant. Best for founders willing to invest significant application time for free capital.

Business Credit Cards

Cards with 0% intro APR offers (12 to 21 months) provide short-term, interest-free financing for operating expenses under $25,000. They also build business credit when used responsibly. ⚠️ Post-introductory rates jump to 18 to 26% APR, so carry no balance past the promotional window.

Family and Friend Loans

Flexible terms, but protect the relationship with a written loan agreement specifying interest rate (at minimum the IRS Applicable Federal Rate), repayment schedule, and default terms. This isn't optional. The IRS can reclassify undocumented loans as taxable gifts.

💰 Bootstrapping and Self-Funding (Including ROBS)

A Rollover for Business Startups (ROBS) lets you invest 401(k) funds into your business tax- and penalty-free through a C-corp structure. The process requires forming a C corporation, creating a 401(k) plan for that corporation, rolling over existing retirement funds, and purchasing stock in the new company. Significant IRS compliance requirements make this best executed with a ROBS specialist like Guidant Financial.

Home Equity Loans/HELOCs

Current rates of approximately 7 to 9% using your home as collateral. ⚠️ You risk losing your home if the business fails. Best used only as short-term bridge financing, not as a primary startup funding source.

Dilutive Alternatives

Angel Investors

Typically $25K to $500K for equity stakes of 10 to 25%. Best for high-growth startups with scalable models. Founders trade ownership for capital plus mentorship and network access.

Venture Capital

$500K to $10M+ for significant equity. Best for startups targeting rapid scale (SaaS, tech, and biotech). Requires a pitch deck, traction metrics, and willingness to give up board seats.

Equity-based (Republic, Wefunder): Raises of $250K to $5M under Regulation CF; Republic charges a 6% cash fee plus 2% equity

Quick Comparison

Startup Loan Alternatives Comparison

Alternative

Capital Range

Cost/Dilution

Speed

Best For

Key Risk

Grants

$5K to $5M

Free 💰

1 to 6 months

R&D, women/minority founders

Extremely competitive

Credit Cards

$5K to $25K

0% intro to 18 to 26%

Instant

Short-term operating expenses

Post-intro rate spike

Family/Friends

Varies

Flexible rate

Days

Early-stage, small amounts

Relationship damage

ROBS

$50K+

No debt/dilution

3 to 6 weeks

Founders with retirement savings

Retirement risk, IRS compliance

HELOC

$25K to $500K

7 to 9% APR

2 to 6 weeks

Bridge financing

Home at risk

Angel Investors

$25K to $500K

10 to 25% equity

1 to 6 months

Scalable startups

Dilution + control loss

Venture Capital

$500K to $10M+

Significant equity

3 to 12 months

High-growth tech/SaaS

Major dilution + board seats

Crowdfunding

$10K to $5M

6 to 8% fee or equity

2 to 4 months

Consumer products

Campaign failure risk

Q11: Startup Business Loans FAQ [toc=FAQ]

Can I get a startup business loan with bad credit?

Yes, but options narrow and costs rise significantly. Below 580, expect APRs of 25 to 99% from online lenders like Fora Financial or merchant cash advances. SBA microloans through CDFIs may accept 580+ with a strong business plan and collateral. Kiva offers 0% interest regardless of credit score, with no minimum required.

⏰ How long does it take to get a startup business loan?

Startup Loan Approval Timelines

Loan Type

Timeline

Online lenders

1 to 7 days

SBA Microloans

2 to 4 weeks

Traditional banks

4 to 8 weeks

SBA 7(a)

2 to 3 months

Luca AI (e-commerce)

Same day

Speed and cost are inversely correlated. The fastest options (online lenders, MCAs) are almost always the most expensive.

Can I use a personal loan to start a business?

Technically yes, but personal loans lack the tax advantages and credit-building benefits of business loans. They carry personal liability regardless, typically cap at $50,000, and charge higher rates than SBA options. The biggest drawback: personal loans do nothing to build your business credit profile. Best used only as short-term bridge financing when no business loan option is available.

Do startup business loans require collateral?

It depends on the loan type. SBA 7(a) loans above $25,000 typically require collateral when available. SBA microloans, most online lenders, and Kiva do not require collateral. Equipment financing uses the equipment itself as collateral, minimizing additional asset requirements. MCAs require no collateral but are the most expensive option by a significant margin.

💸 What's the difference between a factor rate and an APR?

APR is an annualized percentage reflecting total borrowing cost over a full year. A factor rate is a decimal multiplied by your loan amount to determine total repayment; for example, 1.3 x $50,000 = $65,000 total. Factor rates obscure true cost because they don't account for term length: a 1.3 factor over 6 months translates to approximately 60% APR, but over 12 months it's closer to 30% APR. Always convert to effective APR before comparing offers.

How much can I borrow as a startup?

Amounts range from $500 (Kiva) to $5M (SBA 7(a)), but most startups secure $10,000 to $100,000 in their first loan. The amount you qualify for depends on your credit score, existing revenue, available collateral, and the loan type you pursue.

How do I know how much to borrow?

Calculate your startup costs by category: equipment, inventory, legal fees, operating expenses, and a working capital reserve. Then add a 10 to 15% contingency buffer. Verify the resulting monthly payment fits within the 36% debt-to-revenue rule covered in Q7. For e-commerce founders, Luca AI models your exact capital need by connecting to your actual revenue projections, marketing spend plans, and inventory requirements across Shopify and Xero, extracting live data rather than relying on spreadsheet estimates.

FAQ's

What credit score do I need to qualify for a startup business loan in 2026?

Credit score requirements vary significantly across startup loan types, and we want founders to understand the full range before assuming they are disqualified. SBA 7(a) loans typically require a minimum personal credit score of 680 or higher, while SBA microloans through CDFIs may accept scores as low as 580 with a strong business plan and some collateral.

Online lenders like Fora Financial or Bluevine often approve borrowers with scores in the 600 to 650 range, though APRs climb steeply as scores drop. Below 580, expect rates between 25% and 99% APR, and options narrow to merchant cash advances or high-cost short-term products.

However, credit score is not the only path. Kiva offers 0% interest microloans with no minimum credit score requirement at all, making it one of the most accessible entry points for early-stage founders. We recommend using a secured business credit card to build both personal and business credit profiles simultaneously, which strengthens qualification for better products over time.

How long does it take to get approved for a startup business loan?

Approval timelines for startup business loans range from same-day to three months, depending entirely on the loan type and lender. We break down the realistic timelines founders should plan around:

Online lenders: 1 to 7 days. Fastest approval, but typically the most expensive with APRs ranging from 15% to 99%.

SBA microloans: 2 to 4 weeks through CDFI intermediaries, offering rates between 8% and 13%.

Traditional bank loans: 4 to 8 weeks, requiring extensive documentation and often collateral.

SBA 7(a) loans: 2 to 3 months, the most thorough underwriting process but the best rates for qualified borrowers.

Speed and cost are inversely correlated in startup lending. The fastest options are almost always the most expensive, so we advise founders to start the application process well before capital is urgently needed.

For e-commerce operators who cannot wait weeks for approval, Luca AI provides same-day capital disbursal by underwriting against live Shopify revenue and real-time business health data, eliminating the traditional application bottleneck without the punitive rates of merchant cash advances.

What should I do if my startup business loan application gets denied?

Getting denied is the most common outcome for early-stage founders. The Federal Reserve's 2024 Small Business Credit Survey found that firms under $100,000 in annual revenue had only a 31% full-funding rate. We recommend a structured recovery approach rather than reapplying immediately to the same product.

First, contact your loan officer directly and ask for specific denial reasons. Common causes include insufficient time in business, personal credit below threshold, inadequate revenue documentation, or applying for the wrong loan type entirely.

Second, begin building a capital ladder:

Month 1 to 3: Open a secured business credit card and apply for a Kiva 0% microloan.

Month 3 to 6: Register a DUNS number with Dun & Bradstreet and build an Experian Business credit profile.

Month 6 to 9: Apply for an SBA microloan with six months of bank statements and repayment history.

This sequenced approach builds the exact documentation trail lenders require. For e-commerce founders with strong business fundamentals but thin credit histories, performance-based capital from Luca AI bypasses the traditional credit-building timeline by underwriting against real-time revenue and ad performance data.

Can I get a startup business loan with no revenue or collateral?

Yes, but the options are limited and founders need to match their profile precisely to available products. We see three viable paths for pre-revenue or no-collateral startups:

Kiva microloans ($1K to $15K): No credit score minimum, no collateral required, and 0% interest. The catch is that approval depends on community crowdfunding your loan request, which requires a compelling business narrative and active network engagement.

SBA microloans (up to $50K): Administered through CDFIs, these do not require collateral in most cases and accept borrowers with limited revenue history. Rates range from 8% to 13% APR, and a detailed business plan with realistic financial projections can compensate for zero current revenue.

Grants: The SBA's SBIR/STTR programs and private options like the Amber Grant require no repayment at all, though they are extremely competitive and application timelines run 1 to 6 months.

We advise founders to avoid merchant cash advances as a zero-collateral solution because effective APRs frequently exceed 60%. Instead, for e-commerce founders seeking growth capital, Luca AI evaluates live store performance and marketing data to determine funding eligibility, removing the collateral and revenue history requirements that block traditional approval.

What is the difference between a factor rate and an APR on a startup loan?

Understanding this distinction is critical because factor rates are designed to obscure the true cost of borrowing. We see founders consistently underestimate how expensive short-term lending products actually are when they compare factor rates to traditional APRs.

APR (Annual Percentage Rate) reflects the total annualized cost of borrowing, making it directly comparable across different loan terms and products. A 10% APR means you pay $10 per $100 borrowed over one year.

A factor rate is a decimal multiplied by your total loan amount. For example, a 1.3 factor rate on a $50,000 loan means you repay $65,000 total. The problem is that this number does not account for repayment term length. A 1.3 factor over 6 months translates to roughly 60% APR, while the same factor over 12 months is closer to 30% APR.

Online lenders and merchant cash advance providers commonly use factor rates because they appear lower than equivalent APRs. We recommend always converting factor rates to effective APR before comparing any offers. Tools like unit economics calculators help founders model the true impact of borrowing costs on margins and cash flow before committing to capital that could erode profitability.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.