Shopify Capital Loans: The Complete Guide to Eligibility, True Costs, Repayment, and Better Funding Options

11

mins read

TL;DR

Shopify Capital offers MCAs, term loans, and Capital Flex but uses invitation-only access with no application process. Effective APR ranges from 8% to 40% depending on repayment velocity, making fast-selling merchants pay more. UCC-1 liens, milestone traps, daily deductions, and absent human support are critical hidden risks merchants overlook. A 7-criteria decision framework helps founders objectively evaluate whether to accept or explore cheaper alternatives. Luca AI offers dynamically-priced capital with same-day disbursal where costs decrease as business health improves.

1. What Is a Shopify Loan and How Does Shopify Capital Actually Work? [toc=What Is Shopify Capital]

Shopify Capital is Shopify's embedded financing program that provides funding directly through the merchant admin dashboard. Despite the popular search term "Shopify loan," most offers are technically Merchant Cash Advances (MCAs), a purchase of future receivables, not a traditional loan. This distinction affects your accounting, tax treatment, and legal protections. All US-based products are issued through WebBank, and Shopify has disbursed over $6 billion to merchants since launching in 2016, with funding ranging from $200 to $2 million based on store performance.

MCA vs. Term Loan vs. Capital Flex

Shopify Capital offers three distinct funding products. Merchants cannot choose which product they receive. Shopify's algorithm determines the type based on its risk assessment.

Shopify Capital Product Comparison

Feature

Merchant Cash Advance

Term Loan

Capital Flex

Structure

Purchase of future receivables

Fixed-schedule business loan

Revolving credit line

Repayment

% of daily sales (10-17%)

Fixed biweekly installments

Draw and repay; capacity replenishes

Fixed Term

No (18-month max)

12 months

Ongoing

Milestones

25% lump-sum threshold

25% repaid within 60 days

None disclosed

Availability

US, UK, Canada, Australia

US and Australia only

US only (early access)

Min. GMV Required

Not publicly disclosed

Not publicly disclosed

$50K+ trailing 12 months

MCAs represent the vast majority of Shopify Capital offers. Unlike a traditional loan with accruing interest, an MCA means Shopify purchases a fixed dollar amount of your future sales at a discount. You owe the same total regardless of repayment speed, a critical cost dynamic covered in the true APR section below.

Capital Flex: The 2026 Addition

Capital Flex, announced in early 2026, introduces a revolving credit model where merchants draw funds on demand and repayments replenish available capacity. Unlike the one-time lump-sum MCA, Capital Flex allows repeated draws without waiting for a new offer cycle. Shopify's earlier Line of Credit product has been discontinued. Capital Flex replaces it with more flexible draw-and-repay mechanics. Availability is limited to US merchants with $50K+ trailing 12-month GMV.

Common Use Cases

Shopify Capital is designed for short-term working capital, not long-term financing or equipment purchases. The most common funded activities include:

⏰ Seasonal inventory: Pre-purchasing Q4 stock 60-90 days before peak demand

💰 Ad campaign scaling: Deploying additional budget to proven campaigns with demonstrated ROAS

Cash flow bridging: Covering operating expenses during gaps between Shopify Payments payout cycles

Peak-season hiring: Onboarding temporary fulfillment and customer service staff for high-volume periods

The maximum repayment term across all products is 18 months. Merchants with longer-term capital needs should review the alternatives comparison later in this guide.

💸 How Luca AI Structures Capital Differently

Luca AI offers dynamically-priced funding where the rate adjusts in real time based on current business health, not a static snapshot from weeks ago. Advances range from €10K to €100K+ with same-day disbursal, and pricing updates with every individual draw. Merchants who improve performance between advances pay progressively less. Where Shopify Capital locks you into a fixed factor rate on a single lump sum, Luca AI's frequent-small-draws model means your blended cost of capital decreases as your business grows, rewarding improving performance rather than penalizing repayment speed.

2. Who Is Eligible for Shopify Capital and How Do You Get an Offer? [toc=Eligibility and Offers]

Shopify Capital uses an invitation-only model. Merchants cannot apply directly. Offers appear automatically in your Shopify admin under Finance → Capital when Shopify's algorithm determines you qualify. While Shopify does not publish its exact eligibility formula, the known and widely inferred requirements include:

✅ Active Shopify store for at least 90 days with consistent sales history

✅ Shopify Payments enabled as the active payment processor (cannot be deactivated during repayment)

✅ Business located in a supported country (US, UK, Canada, Australia, or select EU markets)

✅ Low chargeback and dispute rate (generally below 1%)

✅ No active Shopify policy violations or compliance flags

⚠️ Inferred factors: sales growth trajectory, revenue consistency, product category risk, refund rates, and overall store health score

🌍 Regional Product Availability

Not all Shopify Capital products are available in every country. The product you are offered depends on both your location and Shopify's risk assessment:

Shopify Capital Regional Availability

Country

Products Available

Payment Requirement

United States

MCAs + Term Loans + Capital Flex

Shopify Payments required

Canada

MCAs only

Shopify Payments required

United Kingdom

MCAs only

Shopify Payments required

Australia

Term Loans only

Shopify Payments required

Germany / Netherlands

MCAs (limited availability)

Shopify Payments required

Some US states restrict access to the loan product specifically, though MCAs remain available in all states. Your principal place of business and bank account must both be in the same supported country.

Step-by-Step: From Offer to Funding

Check your Shopify admin under Finance → Capital for an offer notification

Review available offers. There may be multiple amounts and term options

Select your preferred offer and review the total repayment amount and remittance rate

Accept the terms and submit your application

Shopify conducts an underwriting review (1-3 business days)

⚠️ Your offer may change, shrink, or be rescinded after underwriting. This is not uncommon

Approved funds are deposited to your bank account within 1-5 business days

What to Do If You Are Not Offered Shopify Capital

The most common frustration merchants report is receiving no offer at all, or being suddenly rejected after a long history of successful repayment. There is no appeals process, and Shopify provides no explanation for rejections.

"Our recent Shopify Capital $180,000 loan has been declined after we applied. This is strange to me, as since 2025 we've successfully been accepted for and repaid over $500K in capital loans." r/shopify Reddit Thread

"You're likely blacklisted indefinitely if you weren't able to fully complete the loan." u/nanlycc, r/shopify Reddit Thread

"It's based on sales history. If you haven't launched, you're not eligible." u/o0630gs, r/shopify Reddit Thread

To improve your chances: maintain steady sales growth, keep chargebacks below 0.5%, ensure Shopify Payments is your primary processor, and build at least 90 days of uninterrupted selling history with clean compliance records.

💸 How Luca AI Handles Qualification Differently

Unlike Shopify Capital's opaque invitation system, Luca AI offers a transparent qualification path. Connect your store and your funding eligibility is assessed in real time based on verifiable business health metrics. There is no waiting for an invitation that may never come, and no unexplained rejections after years of successful borrowing. Learn more about the intelligence capital thesis behind this approach.

3. What Does a Shopify Loan Really Cost? Factor Rates, Fee Structures, and True APR Calculated [toc=True Cost and APR]

Shopify Capital does not charge a traditional interest rate. Instead, it uses a factor rate, a flat multiplier applied to your advance amount to determine total repayment. For example, a $100,000 advance at a 1.10 factor rate means you repay $110,000 total. The $10,000 fee is fixed at acceptance and does not change regardless of how quickly or slowly you repay. Typical factor rates range from 1.10 to 1.17 depending on your store's risk profile, with no origination fees and no compounding interest.

Fixed-Fee vs. Monthly-Fee Structure

Shopify Capital offers two fee models depending on the product and offer:

Fixed-fee: A one-time flat fee determined at acceptance. You know the total cost upfront, e.g., $10,000 on a $100,000 advance.

Monthly-fee: A recurring charge (e.g., $1,400/month) that continues until the balance is fully repaid. Total cost depends on repayment duration.

⚠️ Break-even formula: Divide the fixed fee by the monthly fee to find the crossover point. If Fixed Fee ($10,000) ÷ Monthly Fee ($1,400) = 7.1 months, then:

Repay faster than 7 months → monthly-fee structure costs less

Repay slower than 7 months → fixed-fee structure costs less

Choose based on your realistic sales velocity, not optimistic projections.

💰 True APR: The Number Shopify Does Not Show You

A 10% factor fee sounds modest, but the effective Annual Percentage Rate (APR) depends entirely on how fast you repay. This is the most misunderstood aspect of Shopify Capital, and faster repayment actually increases your effective APR.

APR Conversion Formula: Effective APR ≈ (Total Fee ÷ Advance Amount) × (365 ÷ Days to Full Repayment) × 100

Effective APR by Repayment Speed

Scenario

Advance

Fee (1.10)

Repayment Period

Effective APR

⚡ Fast sales

$100,000

$10,000

4 months

~30%

📊 Moderate sales

$100,000

$10,000

8 months

~15%

🐢 Slow sales

$100,000

$10,000

14 months

~8.5%

This is counterintuitive: the better your sales perform, the more expensive the capital becomes in APR terms. Traditional loans work the opposite way. Faster repayment reduces total interest. Understanding your unit economics is critical before accepting any offer.

The same $100,000 Shopify Capital advance costs between 8.5% and 30% effective APR depending solely on how fast your sales repay it.

Luca AI prices capital dynamically. Rates start competitive and decrease as your business health improves between draws. Instead of one large advance at a fixed factor rate, Luca enables frequent smaller draws (€10K-€50K) where each draw is individually priced on current performance. The result: a lower blended cost over 12 months compared to a single large Shopify Capital advance, because improving businesses pay less with each subsequent draw rather than being locked into a static rate. Explore how funding to scale marketing campaigns works with this model.

4. How Does Shopify Capital Repayment Work? Deductions, Milestones, and Cash Flow Impact [toc=Repayment and Cash Flow]

Shopify Capital repayment is automatic. Shopify withholds a fixed percentage of your daily Shopify Payments revenue before depositing the remainder into your bank account. This percentage is called the remittance rate, and it typically ranges from 10% to 17% of daily sales depending on your offer terms.

On a $1,000 sales day with a 10% remittance rate, $100 goes to repayment

On a $3,000 sales day, $300 goes to repayment

On a $0 sales day, $0 is deducted, but the clock still ticks toward milestone deadlines

⚠️ You cannot deactivate Shopify Payments while an active advance is being repaid. Switching payment processors mid-repayment would breach your agreement.

Every sale passes through Shopify's automatic deduction before reaching your bank. Miss a milestone, and a lump-sum demand follows.

Milestone Requirements and Maximum Terms

Repayment is not entirely open-ended. Shopify enforces specific milestone and term limits depending on the product:

Term Loans: At least 25% must be repaid within the first 60 days. Full repayment is required within 12 months. Fixed biweekly installments apply regardless of sales volume.

MCAs: A 25% lump-sum threshold applies. If your daily remittances have not reached 25% of the total owed by a certain date, Shopify may require a lump-sum payment to catch up.

All products: Maximum repayment term is 18 months. If the balance is not cleared by then, Shopify can demand full payment.

Missing a milestone can trigger a mandatory lump-sum payment demand. As one merchant described:

"The contracts say I must have repaid 30% of Loan 2 by the 6-month mark which is tomorrow, but I've had no way to pay anything toward it." r/shopify Reddit Thread

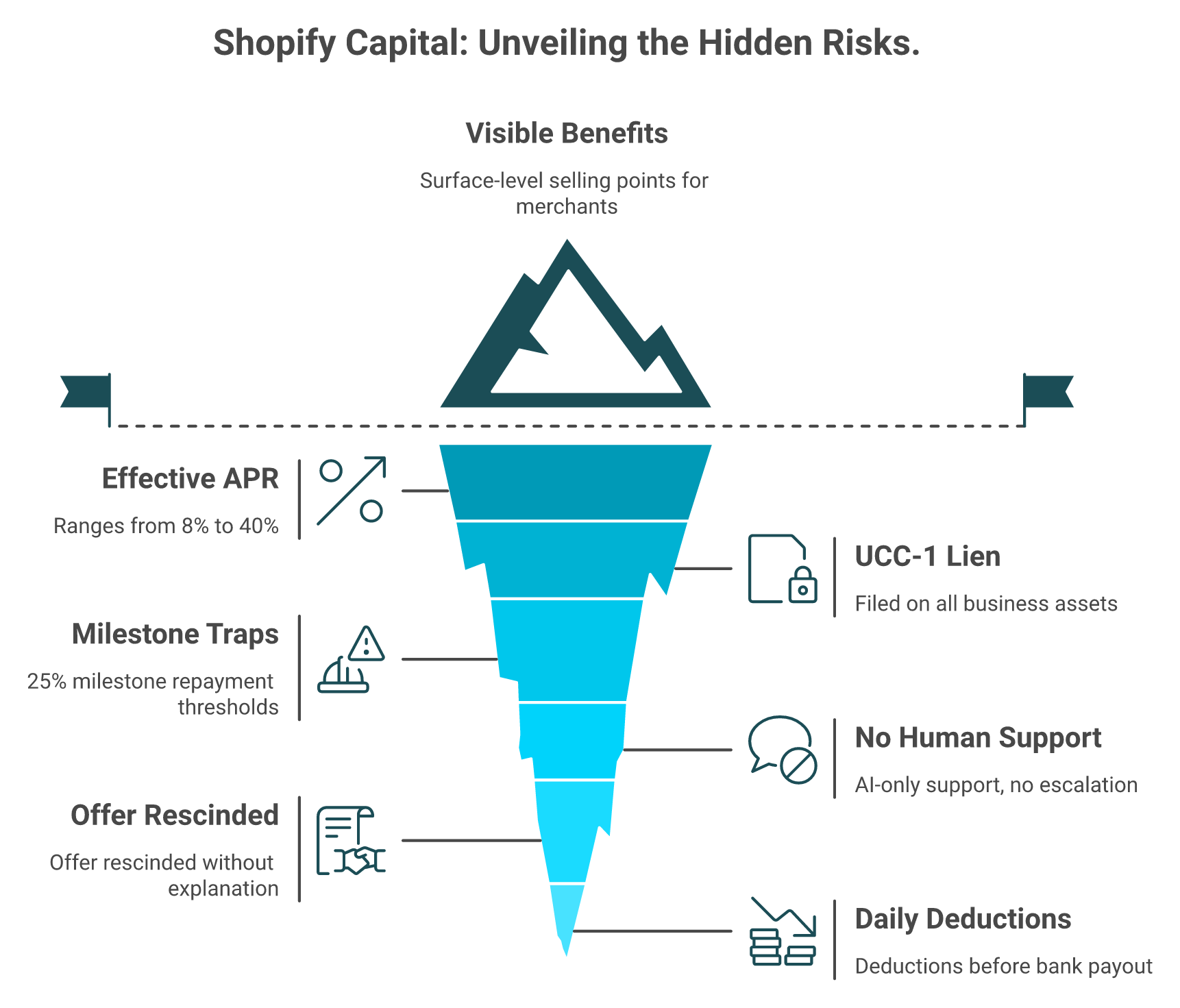

⚠️ UCC-1 Lien: The Hidden Legal Claim

When you accept Shopify Capital, a UCC-1 financing statement is filed against your business assets. In plain terms, this gives Shopify a legal claim on your business assets (inventory, receivables, equipment) until the advance is fully repaid. The practical impact:

Other lenders may decline your application because Shopify's lien takes priority

The lien remains active until full repayment and formal termination filing

Merchants report delays in UCC termination even after complete payoff

💰 Cash Flow Impact by Store Size

The daily deduction affects different store sizes in fundamentally different ways. Here is how a standard 10% remittance rate plays out across three revenue tiers. Understanding this impact is essential for effective cash flow forecasting:

Cash Flow Impact by Revenue Tier

Store Tier

Monthly Revenue

Advance

Daily Deduction

Revenue Withheld

Est. Repayment

🏪 Small

$5,000/mo

$10,000

~$16/day

~10%

~7 months

📈 Growing

$25,000/mo

$50,000

~$83/day

~10%

~7 months

⭐ Established

$100,000/mo

$200,000

~$333/day

~10%

~7 months

Seasonal variation changes everything. Take the $50,000 advance example: during a Q4 spike where revenue triples for two months, repayment accelerates. The advance is cleared faster but at a higher effective APR (~25%). During a post-holiday slump where revenue drops 50% for three months, daily deductions shrink but the repayment timeline stretches, and milestone requirements become dangerous if your cash flow cannot cover the minimums. For merchants looking to better manage these dynamics, exploring AI tools for Shopify owners can provide real-time visibility into repayment projections.

💸 Luca AI's Approach to Repayment Pressure

Luca AI structures capital as many smaller, optimally-timed draws rather than one large lump sum. This means daily cash flow is never burdened by outsized deductions from an oversized advance, and if a seasonal dip hits, you are not trapped in a milestone shortfall on capital you took months ago when business conditions were different. Discover how this AI co-founder approach to financial management keeps your cash runway protected.

5. What Are the Pros and Cons of Shopify Capital? And When Does It Make Sense? [toc=Pros, Cons, and Fit]

Shopify Capital is a strong fit for Shopify-only merchants who need fast working capital under $200K for time-sensitive opportunities, but it carries hidden costs and structural limitations that make it a poor choice for multi-channel sellers, long-term financing, or merchants with access to traditional credit.

✅ Pros

Fast funding: 1-5 business days from acceptance to bank deposit, with no lengthy application process

No personal credit check: Shopify evaluates store performance, not your credit score, and MCAs are not reported as debt on personal credit reports

Simple application: Accept directly in Shopify admin with a few clicks; no paperwork, no business plan, and no financial statements required

Flexible repayment: Daily deductions scale with sales volume; lower sales days mean lower payments

All-in-one dashboard: Manage funding, repayment tracking, and your store from the same Shopify admin interface

No compounding interest: Total cost is fixed upfront via a factor rate; the fee does not grow over time

❌ Cons

Invitation-only: You cannot apply; offers appear when Shopify's algorithm decides you qualify, and rejection reasons are never disclosed

Expensive vs. bank loans: Effective APR ranges from 15-40% depending on repayment velocity, far above SBA loan rates of 6-13%

Daily deduction pressure: 10-17% of every sale is withheld before reaching your bank account, directly impacting working capital and payroll capacity

Only Shopify sales counted: Amazon, wholesale, retail POS, and other channel revenue is invisible to Shopify's algorithm, deflating your offer amount and misrepresenting your true business size

Non-negotiable terms: You accept the offer as-is or decline; there is no ability to negotiate rates, amounts, or repayment percentages

UCC-1 lien: Shopify files a legal claim against your business assets that remains until full repayment and can block other financing

No human support: Multiple merchants report AI-only support for Capital issues with no escalation path to a human agent

⚠️ The Multi-Channel Revenue Problem

This deserves specific attention: if your brand sells on Amazon, Etsy, wholesale, or retail alongside Shopify, Shopify Capital only sees your Shopify revenue. A brand doing $500K/month total but only $150K through Shopify will receive an offer sized for a $150K/month business, dramatically undervaluing your actual capital capacity and making the advance disproportionately expensive relative to total revenue. For brands managing multiple sales channels, understanding your full unit economics across all platforms is critical before accepting any single-channel financing offer.

⏰ When Shopify Capital Makes Sense

✅ Good fit:

Seasonal inventory gaps: Q4 stock purchases needed 60-90 days before peak

Scaling a proven ad campaign with demonstrated ROAS above 3x

Bridging a cash flow gap between Shopify Payments payout cycles

First-time capital need under $50K when speed matters more than cost

❌ Bad fit:

During peak sales periods: you will repay too fast, inflating effective APR above 25%

Long-term financing needs: equipment, warehouse leases, and multi-year hires

Multi-channel sellers: your offer will be undersized relative to total business capacity

Merchants who qualify for SBA loans or bank credit lines: significantly cheaper alternatives exist

Already carrying another MCA: stacking advances compounds daily deduction pressure

6. How Should You Record Shopify Capital on Your Books? Accounting, Tax, and Financial Reporting [toc=Accounting and Tax Treatment]

Shopify Capital MCAs are technically purchases of future receivables, not loans, which directly affects how they should appear on your balance sheet, income statement, and tax return. Many merchants and even their accountants misclassify the MCA fee as "interest expense" when it should be recorded as a "financing fee" or "cost of capital." Term Loans, by contrast, follow standard liability accounting. Getting this distinction right matters for both accurate financial reporting and maximizing your available tax deductions.

Accrual Method: Journal Entries

For a $50,000 advance at a 1.10 factor rate ($55,000 total repayment, $5,000 fee):

Day 1: Receiving the advance

Journal Entry: Day 1 Advance Receipt

Account

Debit

Credit

Cash (Bank Account)

$50,000

-

Prepaid Financing Fee

$5,000

-

MCA Payable (Short-Term Liability)

-

$55,000

Daily remittance (e.g., $100 deducted from a $1,000 sales day)

On Day 1, the full $55,000 appears as a current liability, reducing your net equity on the balance sheet. The $5,000 prepaid fee sits as a current asset and is amortized to the P&L over the projected repayment period. As daily remittances reduce the liability, your balance sheet reflects the declining obligation. This approach spreads the financing cost evenly across the repayment period, matching expense recognition to the period of benefit, which is critical for accurate monthly P&L reporting to investors or lenders.

Cash Method: Simpler but Different Timing

Under cash-basis accounting, the fee is recognized as expense only when actual remittances occur. Each daily deduction is split proportionally between principal and fee. For a $55,000 total repayment on a $50,000 advance, approximately 90.9% of each payment reduces the principal and 9.1% is recorded as financing expense on your income statement.

This means your P&L impact is spread across every payment day rather than amortized monthly, resulting in uneven expense recognition but matching your actual cash outflows. Most small Shopify merchants on cash-basis accounting find this approach simpler, though it can distort monthly profitability if daily sales volume fluctuates significantly.

💰 Tax Deductibility and IRS Considerations

Shopify Capital fees are generally deductible as a business expense classified as a financing cost, not interest. Key tax considerations:

Cash method: Deduct the fee portion as paid throughout the repayment period

Accrual method: Deduct as amortized, spreading the deduction evenly across months

MCAs are not reported as debt on personal credit reports, an important distinction from traditional loans

Tax timing strategy: If you accept an advance late in the fiscal year, the cash method lets you defer most deductions to the following year when remittances actually occur

Cross-year advances: When repayment spans two fiscal years, ensure your CPA allocates the fee deduction correctly to avoid IRS timing issues

⚠️ Always consult a CPA for your specific situation, particularly when an advance spans two fiscal years or you are switching accounting methods.

💸 How Luca AI Simplifies This

Luca AI connects directly to Xero and QuickBooks, automatically categorizing Shopify Capital transactions and amortizing fees correctly under your chosen accounting method, eliminating the manual journal entry reconciliation that causes most MCA accounting errors. Learn more about how Luca handles financial management for e-commerce brands.

7. What Happens After Your First Shopify Capital Loan? Renewals, Re-Borrowing, and Debt Cycle Risks [toc=Renewals and Debt Cycles]

After fully repaying a Shopify Capital advance, merchants typically receive a new offer within one to four weeks. Shopify's algorithm recalculates eligibility fresh each cycle. Subsequent offers may be larger if repayment was smooth and sales grew, or smaller or absent entirely if sales declined, chargebacks increased, or milestones were missed.

How Renewal Offers Work

Once you have repaid at least 65% of your active advance, you will likely see a new offer appear in your Shopify admin. You do not need to wait for full repayment. Shopify allows stacking, where a second advance is approved before the first is cleared. However, repayments on the second advance do not begin until the first is fully paid off.

Subsequent offer amounts are influenced by your repayment performance, current sales trajectory, and overall store health. Merchants who maintained steady growth and clean compliance records during their first advance typically see larger offers. Those who experienced sales dips or milestone issues may see reduced amounts, or no offer at all.

"I've taken almost a million total. You can make it work well in some industries. Now I do SBA." u/n7yyk6y, r/shopify Reddit Thread

"You don't start paying on loan 2 until loan 1 is paid off." u/n7wk0wu, r/shopify Reddit Thread

⚠️ Serial Borrowing: Warning Signs of a Debt Cycle

The convenience of automatic renewal offers creates a real risk of serial borrowing, where each advance funds operating expenses depleted by the previous advance's remittance rate. Watch for these warning signs:

Funding operations, not growth: Taking a new advance to cover payroll or rent rather than revenue-generating activities like inventory or ads

Escalating advance sizes without revenue growth: Accepting $75K, then $100K, then $150K while monthly revenue stays flat

Effective APR creeping above 25%: High-velocity repayment on repeated advances compounds the true cost

Zero ROI visibility: Unable to trace how the last advance generated returns that justify the next one

What merchants see above the surface is speed and simplicity. What sits below are the UCC-1 liens, milestone traps, and APR inflation most discover too late.

What to Do If Your Offer Is Rescinded

Offers can be rescinded mid-underwriting without explanation. This is not uncommon and catches merchants off guard. If it happens: document your current sales data for use with alternative lenders, maintain business continuity without relying on anticipated capital, and explore the alternatives detailed in the comparison section below.

Building Toward Better Options

The smartest Shopify Capital users treat it as a bridge, not a permanent capital strategy. Practical steps for improving subsequent offers and eventually graduating to cheaper financing:

Maintain sales growth trajectory month-over-month

Keep chargebacks below 0.5% and refund rates under 5%

Build 12+ months of clean financial records for future SBA or bank applications

Diversify revenue channels while keeping Shopify Payments active

Use each advance exclusively for ROI-positive activities that generate measurable returns

💸 How Luca AI Prevents Debt Cycles

Luca AI's capital model is designed to prevent debt cycles by construction. Each draw is sized to the specific opportunity it funds, not a lump sum you figure out later. Dynamic pricing means your cost decreases as business health improves, creating a positive cycle rather than an escalating debt burden.

8. What Are Real Merchants Saying About Shopify Capital in 2026? Reviews, Complaints, and Support Analysis [toc=Merchant Reviews 2026]

Shopify Capital reviews in 2026 are sharply polarized. Merchants praise the speed and simplicity, funding in one to three days, no credit check, no paperwork, but consistently criticize cost opacity, unexplained rejections after successful repayment histories, unauthorized deductions, and near-total absence of human support for Capital-related issues. Shopify Inc. holds over 1,100 BBB complaints filed in the last three years, and carries a 1.2-star rating on Trustpilot from over 5,000 reviews. Though not all complaints are Capital-specific, the pattern reflects systemic support quality issues across the platform.

⭐ What Merchants Appreciate

"I've taken almost a million total. You can make it work well in some industries. Now I do SBA." u/n7yyk6y, r/shopify Reddit Thread

"Good value for money? No. Quick money in a pinch? Yes." u/nkl7e6h, r/shopify Reddit Thread

The consistent positive theme across merchant reviews is speed and accessibility. Merchants who understand the true cost and use Shopify Capital specifically for short-term, ROI-positive deployments, such as seasonal inventory and proven ad campaigns, report satisfactory experiences. The product delivers on its core promise when expectations are properly calibrated and the advance is sized appropriately relative to monthly revenue.

❌ Common Complaints and Warnings

The negative reviews cluster around four recurring themes: unexplained rejections, unauthorized deductions, milestone traps, and absent human support.

"Our recent Shopify Capital $180,000 loan has been declined after we applied. This is strange to me, as since 2025 we've successfully been accepted for and repaid over $500K in capital loans." r/shopify Reddit Thread

"Shopify started taking daily repayment deductions from my bank account even though I have NOT received any NEW CAPITAL or SIGNED for a NEW LOAN." r/ecommerce101 Reddit Thread

"Shopify seems to have completely removed the human support element in favor of AI with no backup plan." u/njq1xqu, r/shopify Reddit Thread

"The contracts say I must have repaid 30% of Loan 2 by the 6-month mark which is tomorrow, but I've had no way to pay anything toward it." r/shopify Reddit Thread

The unauthorized deduction complaint is particularly alarming. A merchant reported Shopify withdrawing daily repayment amounts without any new capital disbursement or signed agreement, with support unable to resolve the issue through multiple contacts.

💬 Community Sentiment Summary

The overall pattern across Reddit, Shopify Community forums, and Trustpilot is clear: Shopify Capital works best as occasional, short-term bridge financing for experienced merchants who understand the true cost and do not depend on it as a primary capital strategy. The loudest complaints come from merchants who experienced algorithmic rejections without explanation, unauthorized payment holds, or milestone traps during low-sales periods, all situations where the absence of human support becomes a critical failure point. For merchants seeking a more transparent approach to cash flow forecasting and capital access, alternative models exist that prioritize real-time data over opaque algorithms.

"Best thing really is to get better at cash management which I know sucks but it's the only thing in your control." u/nq69hjr, r/shopify Reddit Thread

"If you aren't qualifying for legitimate financing and your business is more than 2yrs old, ask your accountant why not and see if you can fix it." u/nklbup0, r/shopify Reddit Thread

The recurring message from seasoned merchants: treat Shopify Capital as a tactical tool with an expiration date, not a long-term relationship. Those who have used it successfully eventually graduate to SBA loans, bank lines of credit, or alternative capital providers with more transparent terms and human support.

9. Should You Accept a Shopify Capital Offer? A Decision Framework for Founders [toc=Decision Framework]

Accepting a Shopify Capital offer feels urgent. The money appears in your dashboard, the terms seem simple, and the "no credit check" pitch is appealing. But accepting without modeling the downstream impact on your cash flow, effective APR, and alternative options is how merchants end up paying 30-40% effective APR on capital they did not optimally deploy.

❌ The Wrong Way to Decide

Most merchants evaluate Shopify Capital offers by looking at two numbers: the advance amount and the total repayment. This approach ignores the variables that actually determine whether the capital helps or hurts your business: your repayment velocity (which determines true APR), whether a higher-ROI deployment exists for that capital, and whether cheaper alternatives are available for your specific credit profile and revenue level.

A $50,000 advance with a $5,500 fee looks like an 11% cost. But if your strong Q4 sales repay it in three months, the effective APR is closer to 33%. That same merchant might qualify for an SBA line at 10% APR, paying three times more than necessary because the decision was made on surface-level numbers.

✅ The 7-Criteria Evaluation Framework

Score each criterion from 0 (red flag) to 2 (strong) to systematically assess any Shopify Capital offer:

Shopify Capital 7-Criteria Evaluation Framework

#

Criterion

Score 0 (Red Flag)

Score 1 (Acceptable)

Score 2 (Strong)

1

Effective APR at projected repayment velocity

Above 25%

15-25%

Below 15%

2

Capital deployment ROI

No clear use case

General working capital

Proven ROI activity (inventory, ads with 3x+ ROAS)

3

Daily cash flow impact

Payroll/operations at risk

Tight but manageable

Minimal impact on operations

4

Alternative availability

Qualify for SBA or bank credit

Some alternatives, slower access

No viable alternatives

5

Timing urgency

General capital, no deadline

Moderate urgency (weeks)

Time-critical opportunity (days)

6

Multi-channel revenue

<50% revenue through Shopify

50-80% through Shopify

90%+ through Shopify

7

UCC-1 lien impact

Actively seeking other financing

May need financing within 12 months

No other financing needed

💰 How to Interpret Your Score

11-14 points: Strong candidate. The offer aligns with your business context, timing, and cost tolerance. Proceed with confidence.

7-10 points: Borderline. The decision depends on timing urgency and how quickly you can secure alternatives. Consider spending 48 hours exploring other options before accepting.

Below 7 points: Cheaper or more flexible alternatives almost certainly exist. The offer may feel convenient, but the effective cost relative to available alternatives makes it a poor capital allocation decision.

The single most common mistake: accepting during peak sales periods when you will repay quickly and inflate effective APR, rather than waiting for a slower period when the same advance costs significantly less in APR terms.

💸 Let Luca AI Run This Analysis for You

Luca AI can run this evaluation automatically. Ask: "Should I accept this $75K Shopify Capital offer?" and Luca models your projected repayment velocity based on historical sales patterns, calculates the effective APR, simulates the cash flow impact over 90 days, and flags whether alternative funding sources offer better terms for your specific situation. The analysis that takes hours manually happens in seconds.

10. What Are the Best Alternatives to Shopify Capital in 2026? [toc=Best Alternatives 2026]

If you have evaluated Shopify Capital using the decision framework above and scored below 10, or simply want to compare before accepting, the e-commerce funding landscape in 2026 offers more options than ever. Each alternative carries different trade-offs across cost, speed, eligibility, and repayment flexibility. The right choice depends on your revenue scale, credit profile, and how quickly you need funds.

💰 Master Alternatives Comparison Table

E-commerce Funding Alternatives Comparison 2026

Provider

Funding Speed

Cost Range

Capital Limits

Repayment Model

UCC-1 Lien?

Best For

Luca AI

Same-day

Dynamic, decreasing with performance

€10K-€100K+

Revenue-share, automated

No

Merchants wanting capital priced on current health

PayPal Working Capital

1-3 days

5-30% fixed fee

Up to $250K

% of PayPal sales

No

PayPal-heavy sellers needing fast cash

Clearco

24-72 hrs

6-12% fees

$10K-$10M

Revenue-share

Varies

Larger brands with clean financials

Wayflyer

1-3 days

2-8% advertised

$10K-$20M

Revenue-share

Yes

High-revenue brands needing large advances

SBA Loans

6-8 weeks

6-13% APR

Up to $5M

Fixed monthly installments

Varies

Established businesses, lowest cost

Bank Line of Credit

2-6 weeks

8-15% APR

Varies

Revolving, interest-only draws

Collateral

Businesses with strong credit history

OnDeck / Fora Financial

1-3 days

20-50% APR

Up to $250K

Fixed daily/weekly

Yes

Fast funding when credit options are limited

Settle / Ampla

3-7 days

1-2% monthly

Up to $5M

PO-based, inventory-tied

Varies

Inventory-heavy brands, PO financing

⚠️ What Merchant Reviews Reveal About Alternatives

The reviews from merchants who have used these alternatives paint a consistent picture: speed and accessibility come at the cost of transparency and support quality, while cheaper options like SBA loans require patience and documentation most scaling founders cannot afford.

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing only to be told we no longer fit their criteria." Joshua Hannan, Wayflyer Trustpilot Verified Review

"They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop, Wayflyer Trustpilot Verified Review

"Read their terms and contract carefully! They said their offer is not secured, which is false. They still will file UCC." Zachary Piech, Wayflyer Trustpilot Verified Review

Choose Shopify Capital if you need fast, simple funding under $200K and sell exclusively through Shopify with no immediate need for other financing

Choose SBA Loans if you can wait 6-8 weeks and want the lowest possible rate with multi-year repayment terms

Choose Luca AI if you want capital priced on your current business health with same-day disbursal, optimally-sized draws, and a cost structure that rewards improving performance over time

Choose Settle/Ampla if your primary need is inventory-specific PO financing for large seasonal purchase orders

11. How Does Shopify Capital Work for International Merchants? US vs. UK vs. Canada vs. Australia [toc=International Availability]

Shopify Capital's product availability, funding terms, and repayment structures vary significantly by country. A UK merchant's experience is fundamentally different from a US merchant's, not just in currency, but in the type of funding product offered and the terms attached to it. Understanding these regional differences is critical before evaluating whether Shopify Capital fits your business.

🌍 Country-by-Country Product Breakdown

Shopify Capital International Product Availability

Country

Product Type

Repayment Model

Currency

Capital Flex Available?

Special Notes

United States

MCAs + Term Loans

MCA: % of daily sales; Loans: fixed biweekly

USD

✅ Yes (early access)

Issued through WebBank; some state-level restrictions on loans

Canada

MCAs only

% of daily sales

CAD

❌ No

No term loan option; percentage-based repayment only

United Kingdom

MCAs only

% of daily sales

GBP

❌ No

Similar structure to Canada; MCA only

Australia

Term Loans only

Fixed daily percentage with milestones

AUD

❌ No

Loan product only; milestone requirements within 6-month periods

Germany

MCAs (limited)

% of daily sales

EUR

❌ No

Newer market; limited availability and eligibility pool

Netherlands

MCAs (limited)

% of daily sales

EUR

❌ No

Newer market; limited availability and eligibility pool

The table above illustrates a key limitation: no single country outside the US receives the full product suite. Canadian and UK merchants are restricted to MCAs, while Australian merchants can only access term loans, each with distinct repayment mechanics and risk profiles.

⚠️ International-Specific Constraints

Several limitations apply specifically to merchants operating outside the United States:

Capital Flex is US-only. International merchants cannot access the revolving credit product regardless of revenue level or account history

Principal place of business AND bank account must be in the same supported country. A UK entity with a US bank account will not qualify

Shopify Capital funds in local currency only. Multi-currency stores receive funding in their home currency, not the currency of their customers

Cross-border entities face complications. A UK company selling primarily to US customers may find the eligibility assessment does not reflect actual business strength

Shopify Payments is mandatory in all regions. Merchants using third-party payment processors are automatically ineligible

💬 Support Quality Across Regions

Customer support for Shopify Capital follows the same channels regardless of location: email and chat, with no dedicated phone support for Capital issues. Merchants across all regions report identical frustrations. Escalation paths are effectively non-existent, and Capital-specific issues are often routed to general support agents unfamiliar with financing products or MCA structures.

"I've contacted support five or six times, and every single time they tell me the same thing. It's been escalated to the Shopify Payments team. And then nothing ever happens." r/shopify Reddit Thread

International merchants frequently have fewer alternative financing options available in their local markets compared to US-based sellers, making this support gap particularly impactful when issues arise mid-repayment or during milestone enforcement periods. Exploring the right e-commerce tech stack can help international sellers identify region-appropriate financing tools.

💸 Luca AI's Multi-Market Approach

Luca AI serves e-commerce merchants across European markets with multi-currency capital access and transparent terms regardless of region. There are no country-specific product limitations or restricted availability windows that leave international merchants with fewer options than their US counterparts.

12. Shopify Capital FAQ: Quick Answers to the Most Common Questions [toc=FAQ]

Does Shopify Capital affect my credit score?

No hard credit pull is performed when you receive or accept an offer. MCAs are not reported as debt on personal credit reports. However, if you default and the debt is sent to collections, that collection activity can impact your credit score.

Can I repay Shopify Capital early?

Yes, you can make a lump-sum payment at any time through your Shopify admin under Finance → Capital → Make a Payment. However, the total fee does not decrease with early repayment. You owe the full fixed fee regardless of how quickly you repay. No penalty, but no discount either.

⏰ How long does Shopify Capital funding take?

The typical timeline from acceptance to bank deposit is 2-5 business days. Underwriting review adds 1-3 business days before approval. Total time from offer to funds: approximately 3-8 business days, assuming the offer is not rescinded during underwriting.

Can I have two Shopify Capital advances at once?

In some cases, yes. Shopify may offer a second advance once you have repaid at least 65% of the active advance. However, repayment on the second advance does not begin until the first is completely paid off.

"You don't start paying on loan 2 until loan 1 is paid off." u/n7wk0wu, r/shopify Reddit Thread

⚠️ What happens if I default on Shopify Capital?

Shopify can enforce the UCC-1 lien, redirect Shopify Payments funds, lock your admin panel, and send the debt to collections. Merchants who default report being permanently ineligible for future offers.

Is Shopify Capital a scam?

No. It is a legitimate financing program with US products issued through WebBank, an FDIC-insured institution. However, multiple merchants report unauthorized deductions, unexplained rejections, and near-impossible support escalation. The product is legitimate; the operational support is where trust breaks down.

Can I use Shopify Capital for any business expense?

Yes, there are no usage restrictions. Shopify does not monitor how you deploy the funds. ROI is highest when capital targets revenue-generating activities, such as inventory, proven ad campaigns, and seasonal hiring, rather than fixed costs.

💰 How does Shopify Capital compare to a traditional business loan?

Shopify Capital vs. Traditional Business Loan

Feature

Shopify Capital

Traditional Business Loan

Credit check

None

Full underwriting, hard pull

Cost structure

Fixed factor rate (1.10-1.17)

Interest rate (6-15% APR)

Repayment

Daily % of sales

Monthly fixed installments

Application

Invitation-only, no paperwork

Application with financials

Approval speed

2-5 business days

2-8 weeks

Max term

18 months

1-25 years

Why did my Shopify Capital offer disappear?

Offers can expire, be rescinded during underwriting, or change based on sales fluctuations between viewing and accepting. This is a known frustration with no workaround. If your offer disappears, it may return in future cycles if store metrics improve. Tracking your unit economics consistently helps you stay prepared for when new offers appear.

Is Shopify Capital available on Shopify Basic plans?

Yes. Shopify Capital is available across all plan tiers: Basic, Shopify, Advanced, and Plus. Eligibility is based entirely on sales performance, account health, and geographic location, not your subscription plan.

FAQ's

Is Shopify Capital a loan or a merchant cash advance?

Despite the common search term "Shopify loan," most Shopify Capital offers are technically Merchant Cash Advances (MCAs), not traditional loans. An MCA is a purchase of your future receivables at a discount, meaning Shopify buys a fixed dollar amount of your future sales upfront. This distinction matters for three critical reasons: accounting classification, tax treatment, and legal protections.

With an MCA, you owe the same total repayment regardless of how fast or slow you repay. There is no accruing interest, but there is also no savings from early repayment. The fee is locked at acceptance. Shopify does offer actual term loans in the US and Australia, but these represent a small fraction of total offers. Term loans carry fixed biweekly installments and must be repaid within 12 months.

We recommend understanding this distinction before accepting any offer, because it directly impacts how the cost appears on your books and what deductions you can claim. For a deeper look at how we help merchants navigate these financial decisions, explore our financial management tools.

What is the true APR on a Shopify Capital advance?

Shopify Capital does not disclose an APR figure. Instead, it uses a factor rate between 1.10 and 1.17, which translates to a flat 10-17% fee on the advance amount. However, the effective APR depends entirely on how quickly you repay, and faster repayment actually increases your APR.

Here is how that plays out on a $100,000 advance with a 1.10 factor rate ($10,000 fee):

Repaid in 4 months: ~30% effective APR

Repaid in 8 months: ~15% effective APR

Repaid in 14 months: ~8.5% effective APR

This is counterintuitive. The better your sales perform, the more expensive the capital becomes in annualized terms. Traditional loans work the opposite way. We believe every founder should model their projected repayment velocity before accepting. Our cash flow forecasting tools can simulate this automatically, showing you the real cost based on your actual sales patterns rather than guesswork.

Why was my Shopify Capital offer declined or rescinded?

Shopify Capital is invitation-only, and there is no formal application or appeals process. Offers appear in your Shopify admin when the algorithm determines you qualify, and they can disappear or be rescinded during underwriting without any explanation. This is one of the most common frustrations merchants report.

Known eligibility factors include:

Active Shopify store for at least 90 days with consistent sales

Shopify Payments enabled as the primary processor

Chargeback rate below 1% (ideally below 0.5%)

No active policy violations or compliance flags

Inferred factors include sales growth trajectory, revenue consistency, product category risk, and refund rates. Even merchants with successful repayment histories of $500K+ report sudden rejections with no reason provided. Multi-channel sellers are especially disadvantaged because only Shopify revenue is visible to the algorithm.

We built our qualification process to be the opposite of this. When you connect your store to Luca AI, your funding eligibility is assessed transparently in real time based on verifiable business health metrics, with no opaque invitation gates.

How do daily Shopify Capital repayment deductions affect my cash flow?

Shopify Capital repayment is automatic. A fixed percentage of your daily Shopify Payments revenue, called the remittance rate, is withheld before funds reach your bank account. This rate typically ranges from 10% to 17% of daily sales depending on your offer terms.

On a $1,000 sales day with a 10% remittance rate, $100 goes to repayment. On a $0 sales day, nothing is deducted, but milestone deadlines still apply. This creates a cash flow squeeze that intensifies during seasonal dips when revenue drops but repayment obligations remain.

The most dangerous scenario is accepting a large advance before a slow season. If your daily remittances fall short of milestone thresholds, Shopify can demand a lump-sum payment to catch up. We have seen merchants trapped by this mechanic when post-holiday slumps hit.

We structure capital differently at Luca AI: many smaller, optimally-timed draws rather than one large lump sum. This means daily cash flow is never burdened by outsized deductions. Learn how our approach to cash flow forecasting keeps your runway protected during every season.

What are the best alternatives to Shopify Capital for e-commerce funding?

The e-commerce funding landscape in 2026 offers several strong alternatives to Shopify Capital, each with different trade-offs across cost, speed, and flexibility. The right choice depends on your revenue scale, credit profile, and urgency.

Top alternatives include:

SBA Loans: 6-13% APR, but 6-8 week approval. Best for established businesses wanting the lowest cost

PayPal Working Capital: Fixed fee, 1-3 day funding. Best for PayPal-heavy sellers

Wayflyer: Revenue-share model, $10K-$20M range. Best for high-revenue brands

Clearco: 6-12% fees, 24-72 hour funding. Best for larger brands with clean financials

Bank Lines of Credit: 8-15% APR, revolving. Best for businesses with strong credit history

We designed Luca AI to address the gaps all of these options share. Our capital is dynamically priced, meaning your rate decreases as your business health improves between draws. Each draw is individually sized to the specific opportunity it funds. Explore our detailed comparison of funding alternatives to find the best fit for your business.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.