Payability Alternatives, Reviews & Real Pricing Breakdown (2026): 10 Better Options for Amazon Sellers

11

mins read

TL;DR

Payability charges 2% on gross sales, not net payouts, pushing effective costs to 3.08-3.5% after Amazon fees. Instant Advance carries a hidden 13-26% effective APR with UCC liens that sellers report persisting years after payoff. We ranked 10 alternatives across four financing models, with Luca AI's dynamic pricing topping the list for most seller archetypes. A 12-dimension comparison matrix and 6-archetype decision tree help sellers match the right provider to their margin profile and volume. Switching from Payability requires a 30-day notice period; our 6-step migration guide eliminates the cash flow gap during transition.

Q1: What Is Payability and How Does It Actually Work for Amazon Sellers in 2026? [toc=Payability Explained]

Payability is a revenue-based funding platform built specifically for marketplace sellers that accelerates cash flow through daily payouts and working capital advances. It is not a traditional lender. There are no credit checks, no interest charges, and no loan applications. The core value proposition is straightforward: instead of waiting for Amazon's standard 14-day (biweekly) payout cycle, Payability advances up to 80% of your previous day's sales directly to your account.

⏰ Supported Marketplaces & Eligibility

Payability supports sellers across Amazon, Walmart, Etsy, Shopify, eBay, NewEgg, TikTok Shop, and several other marketplaces. Approval is based entirely on marketplace account health, sales velocity, and performance metrics, not your personal credit score. The application takes under 10 minutes, with approval and first funding in as fast as one business day. There are no origination fees across any tier.

💰 Payability's Four Product Tiers

Payability Product Tiers

Product

Price

Min. Monthly Sales

Sales History

Key Feature

Free Access

$0 / 0% APR

$5,000

3 months

Daily payouts loaded to Payability Seller Card only

Instant Access

1-2% of gross sales

$10,000

3 months

Daily bank transfers (ACH/wire/Instant Transfer) + Seller Card with 2% cashback

Instant Advance

0.5-1% weekly fee (max 20 weeks)

$50,000 (Amazon/Walmart) or $10,000 (other)

9 months

Lump-sum advance of 75-150% of monthly sales, up to $250K

Advance Line

Variable rate on drawn-down funds

~$42,000/mo ($500K+ annual)

9 months

Revolving credit line: fees only on funds actually drawn

How Free Access Actually Works

Free Access advances 80% of the previous day's payouts into your Payability account daily, with the remaining 20% released when the marketplace completes its standard payout cycle. The catch: you must route all spending through the Payability Seller Card to maintain the 0% APR status. For sellers who can funnel 100% of business expenses through the card, this is genuinely free cash flow acceleration. No other provider offers a comparable $0 product.

⚠️ Critical Requirement: The 30-Day Cancellation Notice

One detail buried in Payability's terms that every seller should know upfront: Instant Access requires 30 days' written notice to unenroll. During that window, fees continue to be deducted daily from your payouts. You cannot cancel immediately. If you have an outstanding Instant Advance, you must repay the full balance plus accrued fees before fully exiting.

Q2: What Does Payability Really Cost? Gross vs. Net Fee Math, True Cost Calculator & ROI Breakeven [toc=True Cost Analysis]

The single most important thing to understand about Payability's pricing: fees are charged on gross marketplace sales, not on your net payout after Amazon takes its cut.

💸 Why the Gross vs. Net Distinction Changes Everything

Here's the math most sellers miss. On $100,000 in monthly gross sales:

Amazon referral fees (~15%): -$15,000

FBA fulfillment fees (~15%): -$15,000

Returns/refunds (~5%): -$5,000

Net payout: ~$65,000

Payability's 2% fee is calculated on the $100,000 gross. That's $2,000/month. But $2,000 ÷ $65,000 net = 3.08% effective rate on your actual take-home cash.

Now layer in 2026 Amazon FBA fee increases: standard-size products priced above $50 saw an average $0.31/unit increase effective January 15, 2026, with minimal-split inbound placement fees rising an additional $0.05 on average. For sellers whose net payout drops to ~57-60% of gross after the 2026 fee adjustments, Payability's effective cost pushes to 3.3-3.5%.

Effective Cost Calculator by Seller Profile

Payability Effective Cost Calculator

Monthly Gross Sales

Payability Rate

Monthly Fee

Effective Rate (65% net)

Effective Rate (50% net)

$25,000

2.0%

$500

3.08%

4.00%

$50,000

1.5-2.0% (negotiable)

$750-$1,000

2.31-3.08%

3.00-4.00%

$125,000

1.25-1.5% (negotiated)

$1,563-$1,875

1.92-2.31%

2.50-3.00%

$250,000

1.0-1.25% (volume discount)

$2,500-$3,125

1.54-1.92%

2.00-2.50%

Instant Advance: The Hidden APR

Instant Advance Effective APR

Advance Amount

Weekly Fee Rate

Total Cost (20 weeks)

Effective APR

$10,000

1.0%

$2,000

~26%

$50,000

0.75%

$7,500

~19.5%

$100,000

0.65%

$13,000

~16.9%

$250,000

0.50%

$25,000

~13%

⚠️ Hidden surcharges most sellers overlook: Instant Transfer fees ($5-25 per same-day bank deposit), wire transfer fees ($15-35), and international currency conversion markup (1-3% above spot rate).

ROI Breakeven: When Do Daily Payouts Pay for Themselves?

At a 2% fee, Payability pays for itself only when the time value of receiving funds 10-12 days earlier exceeds that fee. For a seller reinvesting into inventory with 30% margins, the breakeven requires turning that capital within ~7 days of receipt. For a seller deploying early cash into PPC with uncertain ROAS, the breakeven is significantly riskier. You're paying a guaranteed 2% for speculative returns. Tools like unit economics trackers can help model whether the early access genuinely drives incremental profit.

Q3: What Are Real Amazon Sellers Saying About Payability? (Trustpilot, Reddit, YouTube & Seller Central Reviews) [toc=Seller Reviews]

You signed up for Payability expecting a straightforward 2% fee. Three months in, you're exporting CSVs, trying to reconcile why your actual deductions are 40% higher than projected. You search Reddit and discover hundreds of sellers asking the same questions. Across 476+ Trustpilot reviews, Reddit threads on r/AmazonSeller and r/FulfillmentByAmazon, and YouTube deep-dives, a consistent pattern emerges: the product works, but the pricing transparency doesn't.

❌ The 6 Most Common Complaint Patterns

1. Gross vs. net fee confusion

"They actually charge around 2% on GROSS SALES, meaning they calculate this fee based on all sales, regardless of whether or not you have received payment for them. In my view, the 2% they advertise is misleading. For us, it ended up being closer to 6%." u/deleted, r/AmazonSeller Reddit Thread

2. UCC filing not removed after payoff

"I paid off the advance in full, but two years later the UCC filing still hasn't been removed. Keeping a satisfied UCC in place this long should be a crime." Neal S. Payability - Trustpilot Verified Review

3. Fee double-dipping

"Watch your fees. Payability double dips their fee charges, so no matter what you won't get ahead or even close to 2% fee rate. Lots of false advertising here." Norma Jeanne Leite Payability - Trustpilot Verified Review

4. Rates don't decrease with scale Multiple sellers report having to fight for rate reductions despite tripling their sales volume.

5. Trial period charges Reports of fees charged despite canceling during the 7-day trial, with no clear grace period process.

6. Perceived fake reviews

"I think most of the 5 star reviews here are fake or incentivized. The only positive is that once you stop working with Payability, you appreciate every penny you get directly from Amazon." Leandro Payability - Trustpilot Verified Review

✅ 4 Genuine Praise Points

⭐ Cash flow lifesaver: One seller reported launching 3 new products within weeks because daily deposits freed up capital that Amazon's biweekly cycle had been locking up

⭐ Free Access genuinely costs $0: Sellers routing 100% of expenses through the Seller Card confirm zero fees: "free money acceleration"

⭐ No credit check: "Couldn't get bank financing, Payability approved me in 24 hours" is a consistent theme among newer sellers and those rebuilding credit

⭐ Costs scale down with sales: Unlike fixed loan payments, when sales drop, Payability fees drop proportionally, providing natural downside protection

📊 Net Sentiment: 6/10 Cautiously Positive

Payability carries a 4.4/5 on Trustpilot across 476+ reviews, but the distribution reveals the story: highly polarized between sellers who found it genuinely valuable during cash crunches and sellers who discovered the effective cost was far higher than advertised. YouTube reviewers generally validate the product's utility for cash flow acceleration while consistently flagging fee transparency as the primary weakness.

Q4: Payability Pros, Cons & the Contractual Fine Print Every Seller Should Read [toc=Pros, Cons & Fine Print]

Payability solves a real, documented problem. Amazon's slow biweekly payout cycle constrains working capital for sellers who need to reinvest daily. But its contractual structure creates compounding friction that many sellers don't discover until they're already enrolled.

✅ Pros

Daily cash flow acceleration: receive up to 80% of yesterday's sales

No credit check or personal guarantee required

No origination fees across all product tiers

Free Access plan at genuinely $0 (with Seller Card requirement)

Transfer fees for non-ACH methods not clearly disclosed upfront

Outstanding advances must be fully repaid before exit

⚠️ Contractual Fine Print Deep-Dive

1. UCC-1 Liens Payability files a UCC lien on your business when you take an Instant Advance. This is standard in merchant cash advances, but the removal process is where problems emerge. Multiple sellers report UCC filings remaining active for years after full payoff, which can directly impede your ability to secure other financing.

2. 30-Day Cancellation Hold Instant Access requires 30 days' written notice. During this window, daily fee deductions continue. You cannot cancel immediately, and the overlap creates a material cost if you're transitioning to a different provider.

3. Data Access & API Persistence Payability connects directly to your marketplace API, pulling full sales data, payout schedules, and account health metrics. This data connection persists after cancellation until you manually revoke API access from your marketplace settings.

4. Trial Period Auto-Conversion The 7-day Instant Access trial auto-converts to paid if not cancelled through the proper process. Multiple user reviews report being charged despite believing they had cancelled.

"I never understood the charges, the fees are very shady. They said one thing then it does not add up. Just confusing." Shatina Payability - Trustpilot Verified Review

💡 Top 5 Documented Reasons Sellers Leave Payability

Effective cost too high After doing the gross-vs-net math, sellers realize true costs are 50-75% higher than the advertised rate

UCC lien complications Active liens blocking applications for bank lines of credit, SBA loans, or other secured financing

Outgrew the model Sellers crossing $100K+/month qualify for bank lines of credit at 10-12% APR vs. Payability's 12-24% effective APR

Amazon suspension exposure Fees continued accruing during account suspensions while payouts were frozen

Found cheaper lump-sum alternativesWayflyer, Clearco, and others offer 6-15% flat fees for growth capital vs. Instant Advance's 13-26% effective APR

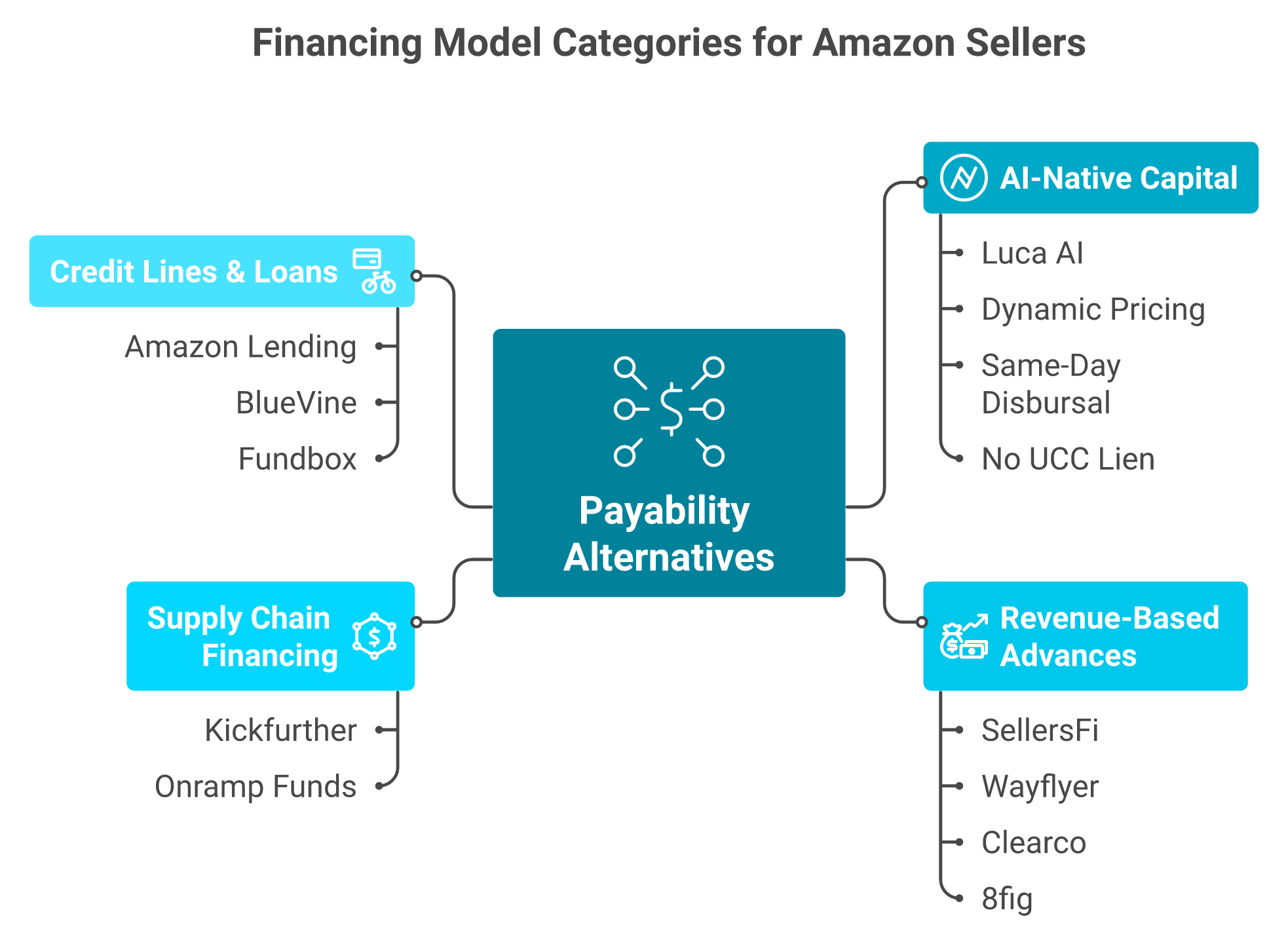

Q5: What Are the 10 Best Payability Alternatives for Amazon Sellers in 2026? [toc=Top 10 Alternatives]

Not all financing tools are built the same. The 10 alternatives below span four distinct financing model categories: (A) AI-native capital with dynamic pricing, (B) revenue-based advances and daily payout alternatives, (C) supply chain and inventory-specific financing, and (D) traditional credit lines and term loans. Unlike competitor listicles where providers rank themselves #1, this list is ordered by overall value-to-Amazon-seller fit.

The 10 best Payability alternatives fall into four distinct financing models, each suited to different seller profiles and capital needs.

⭐ #1: Luca AI: Intelligence-Led Dynamic Capital

On the capital side, Luca AI offers dynamically-priced advances where the rate adjusts in real time based on business performance. Stronger months mean cheaper capital. Disbursal is same-day, with no personal guarantee, no UCC lien, and no applications per advance. The model favors frequent small advances ($10K-$50K) so capital never sits idle, reducing total cost versus one lump sum.

✅ Lowest effective cost via dynamic pricing + optimal sizing

✅ One-click deployment; rate improves as your business improves

❌ Newer entrant; capital amounts may start smaller for new users

Separately, Luca also provides an AI-native analytics layer with a unified data warehouse, predictive modeling, scenario simulation, root-cause analysis, and customized reporting pushed via Slack and email.

💰 #2-#5: Revenue-Based Advance Alternatives

#2 SellersFi/Uncapped: Direct Payability Replacement

0.5-1% weekly fee model. Acquired by Uncapped, but the transition has created friction for existing customers.

"I wasn't asked when Uncapped took over the business I had with SellersFi. Uncapped is incapable to connect to my bank account due to their flawed integration of Plaid's service." Volker Foerster Uncapped - Trustpilot Verified Review

#3 Wayflyer: Growth Capital for Scaling Brands

6-15% flat fee, $10K-$1M advances, revenue-share repayment. Large funding amounts, but inconsistent underwriting is a documented pattern.

"After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute." Geoff Brand Wayflyer - Trustpilot Verified Review

#4 Clearco: Post-Restructuring Challenges

6-12% flat fee, $50K-$500K. Post-restructuring, tighter underwriting and near-absent customer support dominate reviews.

#5 8fig: AI-Driven Supply Chain Financing

Multi-round disbursement cycles with documented bait-and-switch on approved amounts.

"We had a signed agreement with 8fig for three preset rounds of funding. They only funded the first round, which was at the highest cost, and then backed out of the rest." Melissa 8fig - Trustpilot Verified Review

💸 #6-#10: Marketplace Lending & Credit Lines

Marketplace Lending and Credit Line Alternatives

#

Provider

Cost Model

Best For

6

Amazon Lending

6-20% total cost, invitation-only

Qualifying Amazon sellers: lowest friction

7

Kickfurther

0.5-2% monthly interest

Inventory-only financing, no bank credit needed

8

Onramp Funds

Revenue-based repayment, ecommerce-specific

Marketplace sellers needing purpose-built capital

9

BlueVine

Line of credit up to $250K, 14%+ APR

Flexible draw-as-needed credit; no UCC lien under $200K

Honorable mentions: Ampla (best for DTC/CPG brands), OnDeck (reliable but expensive term loans), and Resolve (B2B focus at 3.15%, better suited for wholesale sellers than marketplace sellers).

Q6: Payability vs. Alternatives: The Full Head-to-Head Comparison Matrix [toc=Comparison Matrix]

Every Payability alternative structures fees differently: percentage of gross sales, flat fee on advance, weekly rates, and revenue-share. This makes apples-to-apples comparison nearly impossible without normalizing across dimensions. This matrix standardizes the comparison across 12 dimensions so sellers can filter by what matters most.

📊 Master Comparison Table

Payability vs. Alternatives: 12-Dimension Comparison

Dimension

Payability

Luca AI

SellersFi

Wayflyer

Clearco

8fig

Amazon Lending

Kickfurther

Onramp

BlueVine

Fundbox

Fee Type

% of gross

Dynamic rate

Weekly %

Flat % advance

Flat % advance

Multi-round cycle

Fixed APR

Monthly interest

Rev-share

APR

APR

Effective Annual Cost

12-24%

Varies (improves with performance)

12-26%

6-15% flat

6-12% flat

10-30%+

6-20%

6-24%

Variable

14-95%

36-99%

Max Funding

$250K

$10K-$50K per advance

$2.5M

$1M

$500K

$1M+

$5M

$500K

Variable

$250K

$250K

Funding Speed

1 day

Same day

2 days

1-3 days

2-5 days

1-2 weeks

Instant (pre-approved)

1-2 weeks

3-5 days

Same day

Same day

Min Monthly Revenue

$5K-$50K

Varies

$10K

$20K+

$10K+

$25K+

Invitation-only

$10K

$10K+

$10K

$2.5K

Credit Check

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

✅ Yes (625+)

✅ Yes (600+)

Personal Guarantee

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

❌ No

✅ Yes

✅ Yes

UCC Lien

✅ Yes (Advance)

❌ No

✅ Yes

✅ Yes

✅ Yes

✅ Yes

✅ Yes

❌ No

✅ Yes

❌ No (<$200K)

❌ No

Cancellation Terms

30-day notice

No hold period

Varies

Revenue-share until paid

Revenue-share until paid

Contract-bound

Loan term

Consignment term

Revenue-share

Flexible

Flexible

Analytics/Intelligence

❌ None

✅ Full AI layer

❌ None

❌ Basic dashboard

❌ None

❌ Basic

❌ None

❌ None

❌ None

❌ None

❌ None

🏆 Dimensional Winners

Fastest funding speed:Luca AI (same-day) and Amazon Lending (instant for pre-approved sellers)

Lowest effective cost: Amazon Lending (6% floor, but invitation-only); Luca AI (dynamic pricing rewards business improvement)

Most accessible (no credit check): Payability, Luca AI, SellersFi, Wayflyer, and Clearco

No personal guarantee: Payability, Luca AI, Wayflyer, Clearco, and 8fig

No UCC lien: Luca AI, Kickfurther, BlueVine (under $200K), and Fundbox

Most cancellation flexibility: Luca AI (no hold period), Fundbox, and BlueVine vs. Payability (30-day mandatory notice)

Use this table to shortlist 2-3 providers based on your non-negotiable criteria. For example, "no credit check + under $50K/month + Amazon-only" narrows the field to Payability, Luca AI, and SellersFi. Then apply the archetype recommendations in the next section to make your final selection.

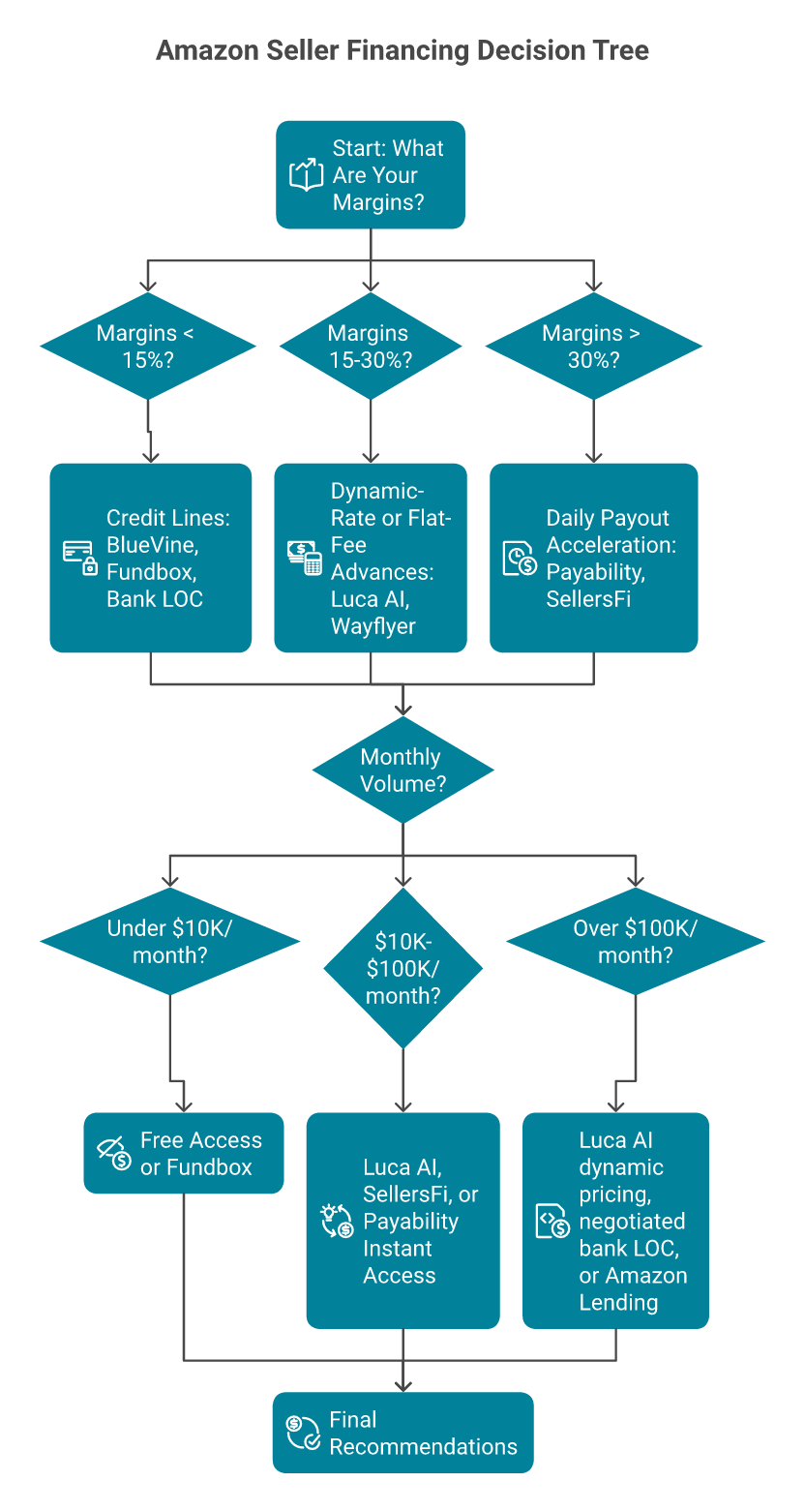

Q7: Which Alternative Is Best for Your Seller Type? (Archetype Recommendations & Decision Tree) [toc=Seller Archetype Guide]

Your optimal financing provider depends on your seller model, not just your revenue. Score yourself against these six archetypes to find your match.

🔍 Archetype 1: Amazon FBA Arbitrage Sellers

High volume, thin margins (10-20%), fast inventory turns. Best fit: Luca AI (dynamic pricing rewards fast turns with lower rates) or Payability Free Access (if all spend routes through Seller Card). Avoid: Wayflyer/Clearco, as flat fees erode thin margins on large capital draws.

🔍 Archetype 2: Private Label Brand Owners

Moderate margins (25-40%), longer inventory cycles, PPC-dependent. Best fit: Luca AI (capital sized to campaign scaling needs; rate improves with ROAS improvement) or Wayflyer (growth capital for proven campaigns). Avoid: Payability Instant Advance, as weekly fees compound heavily during long inventory lead times.

🔍 Archetype 3: Wholesale Sellers

Very thin margins (5-15%), very high volume, predictable reorders. Best fit: BlueVine or Fundbox credit lines (lowest APR for qualifying sellers) or Amazon Lending if invited. Avoid: Any percentage-of-gross-sales model (Payability, SellersFi), as at 5-15% margins, even 1% of gross destroys profitability.

🔍 Archetype 4: Multi-Channel Sellers

Amazon + Shopify + Walmart: need unified cash flow across marketplaces. Best fit: Luca AI (multi-platform data synthesis plus single capital relationship across all storefronts) or Payability (multi-marketplace daily payouts). Avoid: Amazon Lending (Amazon-only) or Shopify Capital (Shopify-only).

🔍 Archetype 5: Sellers Under $10K/Month

Limited options and no negotiation leverage. Best fit: Payability Free Access ($0 cost) or Fundbox (minimum $30K annual revenue, the lowest threshold available). Avoid: Wayflyer, 8fig, and Clearco, as minimums are too high.

🔍 Archetype 6: Sellers Over $100K/Month

Maximum negotiation leverage. Best fit: Luca AI (dynamic pricing most advantageous at scale) or a negotiated bank line of credit at 10-12% APR. Avoid: Payability at the standard 2% rate without negotiation, as that's an effective 24%+ APR equivalent on net payouts.

🌳 Decision Tree Summary

Start with your margin profile:

Margins <15%: Use credit lines (BlueVine, Fundbox, bank LOC)

Margins 15-30%: Use dynamic-rate or flat-fee advances (Luca AI, Wayflyer)

Margins >30%: Daily payout acceleration can work (Payability, SellersFi)

Then filter by volume:

Start with your margin profile, then filter by volume to find the financing provider that fits your Amazon business model.

Under $10K/month: Free Access or Fundbox

$10K-$100K/month: Luca AI, SellersFi, or Payability Instant Access

Over $100K/month: Luca AI dynamic pricing, negotiated bank LOC, or Amazon Lending if invited

Q8: What Happens to Your Financing If Amazon Suspends Your Account? [toc=Amazon Suspension Impact]

Amazon suspends tens of thousands of seller accounts annually for policy violations, IP claims, or review manipulation. If you're enrolled with a financing provider when suspension hits, the financial exposure varies dramatically by provider. This section maps what happens to your money across every major option.

⚠️ Provider-by-Provider Suspension Analysis

Payability: Instant Access fees continue accruing on your gross sales balance while payouts are frozen. Instant Advance must still be repaid in full plus accrued weekly fees regardless of payout status. The UCC lien remains on file throughout.

SellersFi/Uncapped: Similar structure to Payability. Revenue-share repayment pauses if zero revenue flows, but balance remains due. Multiple sellers report hostile communication when accounts face disruption.

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M." Xin Shui, CEO/Founder Uncapped - Trustpilot Verified Review

Wayflyer: Revenue-share pauses if no sales, but the UCC lien persists. Documented cases of approved funding being reversed during account disruptions.

Clearco: ACH-based repayment from your bank account continues regardless of marketplace status. Multiple sellers report Clearco pulling funds faster than contracted terms.

"They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly." Thomas Bishop Clearco - Trustpilot Verified Review

8fig: Documented cases of pulling pre-approved funding during account disruptions while maintaining repayment obligations and UCC liens.

Amazon Lending: Suspension can freeze both sales AND the lending facility simultaneously. Remaining balance is due per original terms regardless.

✅ Luca AI's Structural Advantage

Luca AI's dynamic model with small, frequent advances means maximum exposure at any given point is limited to $10K-$50K, not $250K-$500K. Disbursal pauses automatically if account health degrades, and there's no UCC lien creating secondary financial damage during an already critical period.

🛡️ Risk Mitigation Framework

Minimize maximum exposure: Providers using frequent small advances (Luca AI) limit worst-case loss versus single large lump-sum providers

Verify UCC lien removal timeline: Demand written confirmation of the removal process before signing; multiple sellers across Payability, 8fig, and Wayflyer report liens persisting years after payoff

Maintain separate bank reserves: Keep 1-2 months of repayment obligations liquid outside the marketplace ecosystem

Check for cross-default clauses: Some providers can call the entire balance due if you default on another obligation

"I have already paid these people off and they put a lien on my marketplace account. I asked for a letter of payoff and they have been lagging since November." Bobby Onramp Funds - Trustpilot Verified Review

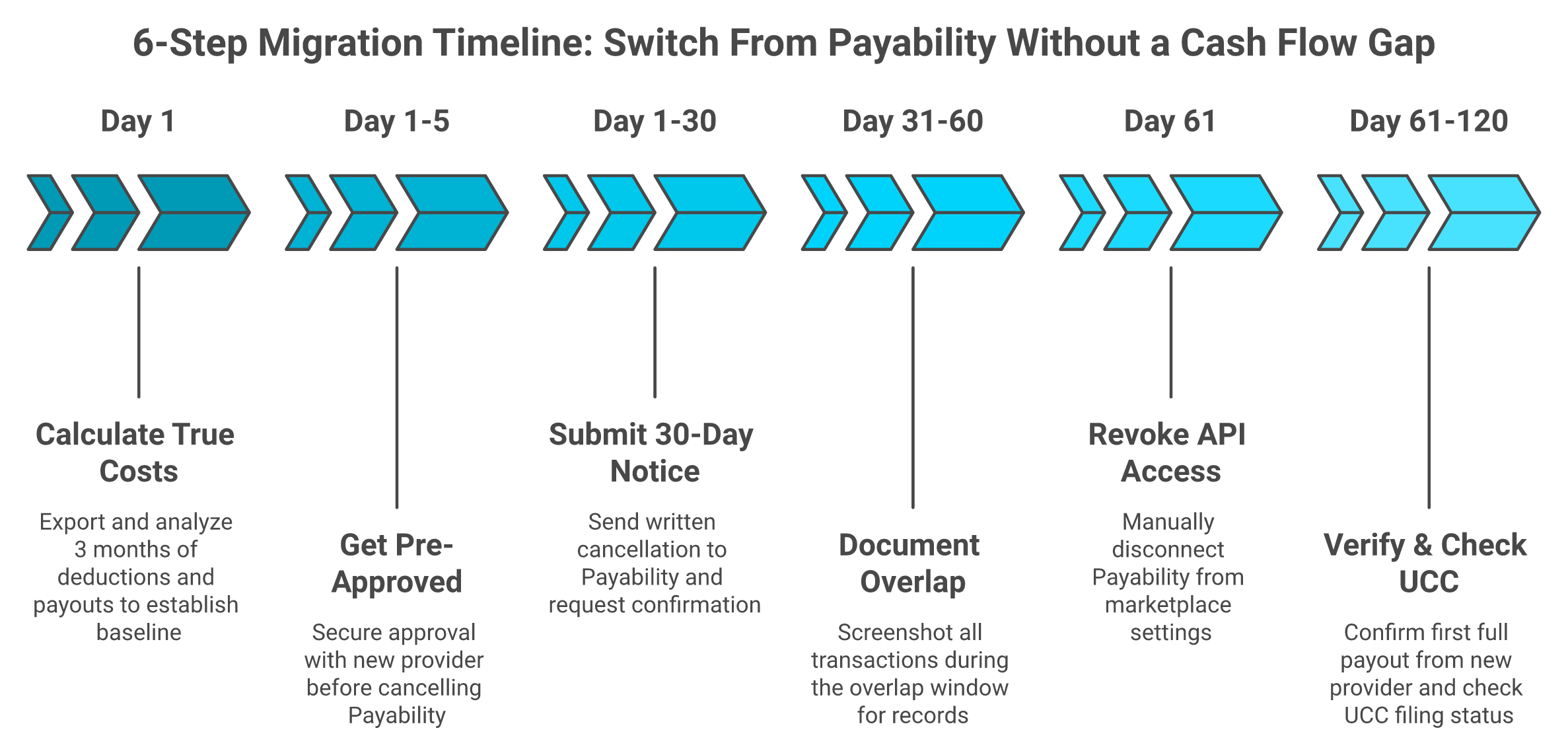

Q9: How Do You Switch From Payability Without a Cash Flow Gap? (Step-by-Step Migration Guide) [toc=Migration Guide]

Payability requires 30 days' written notice to unenroll from Instant Access. During that window, fees continue to be deducted daily. If you have an outstanding Instant Advance, you must repay the full balance plus accrued fees before fully exiting. This creates a 30 to 45 day overlap period where you may be paying for two services simultaneously.

💸 Budget for Your Switching Cost

At $100K/month gross and a 2% rate, the 30-day overlap costs approximately $2,000. Treat this as the price of migration. For sellers with an outstanding Instant Advance at 1% weekly, add the remaining weekly fees to that figure. Sellers who don't budget for this window often panic and delay the switch indefinitely, locking themselves into higher long-term costs.

⏰ The 6-Step Migration Timeline

Follow these six steps in order to migrate away from Payability without creating a cash flow gap during the 30-day overlap period.

Calculate your true Payability costs over the past 3 months using the gross-to-net effective rate framework. Export daily deduction records from Payability and cross-reference with your marketplace payout reports. This is your baseline for measuring improvement.

Get approved with your new provider BEFORE submitting Payability cancellation. Provider onboarding timelines vary significantly:

Submit 30-day written cancellation to Payability. Email is acceptable, but follow up with a phone call and request written confirmation of the cancellation date.

Document all transactions during the overlap period. Screenshot daily deductions, payout amounts, and any discrepancies. This protects you if there are billing disputes post-cancellation.

Revoke Payability's API access to your marketplace account manually after final settlement. Payability's data connection persists post-cancellation unless you disconnect it from your Amazon/Shopify/Walmart settings.

Verify first full payout cycle from your new provider, then confirm Payability has fully offboarded. Critical: check your UCC filing status within 60 days. If the lien has not been removed, send a formal demand letter. UCC filings can persist for up to five years if you don't actively request removal.

⚠️ 5 Common Switching Mistakes

❌ Canceling Payability before new provider is approved creates a cash flow gap during Amazon's 14 to 21 day payout cycle

❌ Forgetting to revoke API access means Payability retains your data connection post-cancellation unless manually disconnected

❌ Not checking UCC lien removal is a costly oversight; sellers report liens persisting 2+ years after payoff, and lenders generally remove them but only if you proactively request it

❌ Ignoring the overlap cost by not budgeting for the 30-day double-fee window leads to cash flow surprises

❌ Switching during Q4 peak is the worst time to introduce working capital uncertainty. Plan transitions for Q1 or Q2 when sales volume is lower and the financial impact of the overlap period is minimized

No. Payability is a payout acceleration service (Instant Access) and merchant cash advance provider (Instant Advance). It does not report to credit bureaus, does not charge interest (fees are flat), and does not require credit checks. However, it does file UCC-1 liens for Instant Advance, which functionally behaves like secured lending.

🔍 Is Payability Legit or a Scam?

Payability is a legitimate, established fintech company operating since 2015 with 476+ Trustpilot reviews and a 4.4/5 rating. It is not a scam, but its fee structure (gross vs. net) creates real confusion that leads to justified complaints. Net sentiment: 6/10. The product works; the pricing transparency does not.

"I think most of the 5 star reviews here are fake or incentivized. The only positive is that once you stop working with Payability, you appreciate every penny you get directly from Amazon." Leandro Payability - Trustpilot Verified Review

💰 Can I Use Payability and Another Financing Provider Simultaneously?

Yes, but proceed with caution. Multiple providers drawing from the same payout stream can create cash flow conflicts. Payability's daily deduction model means less cash available for revenue-share repayments to other providers like Wayflyer or Clearco.

⏰ How Does Payability Compare to Just Waiting for Amazon's Payout?

For sellers with healthy cash reserves, waiting costs $0. Amazon's DD+7 reserve policy holds seller funds for seven days after the customer's delivery date, resulting in a 14 to 21 day total gap between sale and bank deposit. Payability's value only materializes when early access to capital generates returns exceeding the fee. For most sellers with margins above 25% reinvesting into inventory, the math works. For PPC reinvestment with uncertain ROAS, it's riskier.

🌍 Does Payability Work for Non-Amazon Sellers?

Yes. Payability supports Walmart, Shopify, eBay, Etsy, NewEgg, TikTok Shop, and other marketplaces. However, Instant Advance minimum revenue thresholds differ: $50K/month for Amazon/Walmart, and $10K/month for other marketplaces.

💸 What's the Cheapest Payability Alternative in 2026?

Cheapest Payability Alternative by Seller Situation

⚠️ Can Payability Affect Other Business Financing?

Yes. The UCC-1 lien filed for Instant Advance can complicate applications for bank loans, SBA loans, or other secured financing. Some lenders will not extend credit while an active UCC lien exists from another provider. UCC filings can take up to five years to drop off your report if you don't actively request removal.

"I paid off the advance in full, but two years later the UCC filing still hasn't been removed. Keeping a satisfied UCC in place this long should be a crime." Neal S. Payability - Trustpilot Verified Review

Partially. At 2% fee and 2% cashback, you'd need to route 100% of business spending through the Seller Card to fully offset the fee, and only if your business expenses equal your gross sales (which they don't). Realistically, if 40% of your gross sales equals your business expenses run through the card, the cashback offsets roughly 40% of the fee, bringing effective cost from 2% to approximately 1.2% of gross. For a more complete picture of how unit economics interact with financing costs, sellers should model the net fee impact against their actual expense-to-revenue ratio.

FAQ's

What is the real effective cost of Payability after Amazon fees in 2026?

Payability's advertised 2% fee is calculated on gross marketplace sales, not on your net payout after Amazon takes its cut. This distinction fundamentally changes the math. On $100K in monthly gross sales, after Amazon referral fees (~15%), FBA fulfillment (~15%), and returns (~5%), your net payout is roughly $65,000. Payability's $2,000 monthly fee divided by that $65,000 net equals a 3.08% effective rate on your actual take-home cash.

With 2026 Amazon FBA fee increases (standard-size products above $50 saw an average $0.31/unit increase effective January 15, 2026), sellers whose net drops to 57-60% of gross face effective costs of 3.3-3.5%. We built a full cost calculator to help sellers model their true rate by seller profile.

$25K/month gross at 2%: 3.08% effective (65% net) to 4.00% effective (50% net)

$125K/month at 1.5% negotiated: 1.92-2.50% effective

$250K/month at 1.25% volume discount: 1.54-2.00% effective

For Instant Advance, the hidden APR ranges from ~13% ($250K advance) to ~26% ($10K advance) over the maximum 20-week term.

Which Payability alternative is best for Amazon FBA sellers with thin margins?

For Amazon FBA sellers operating on thin margins (10-20%), any percentage-of-gross-sales model like Payability or SellersFi can destroy profitability. At 5-15% net margins, even a 1% gross fee consumes a disproportionate share of your actual profit.

We recommend matching your financing provider to your margin profile using this framework:

Margins under 15% (wholesale/arbitrage): Use credit lines like BlueVine or Fundbox. If you qualify, a bank line of credit at 10-12% APR is the cheapest option. Amazon Lending (6% floor) is ideal if you receive an invitation.

Margins 15-30% (private label):Dynamic-rate capital from Luca AI or flat-fee advances from Wayflyer work best. The rate improves as your business performance strengthens.

Margins above 30%: Daily payout acceleration (Payability, SellersFi) can work if the time value of early capital access exceeds the fee.

For FBA arbitrage sellers specifically, Luca AI's dynamic pricing rewards fast inventory turns with lower rates, or Payability Free Access works if you can route 100% of spending through the Seller Card at $0 cost.

How do I cancel Payability without creating a cash flow gap?

Payability requires 30 days' written notice to unenroll from Instant Access, during which fees continue to be deducted daily. If you have an outstanding Instant Advance, the full balance plus accrued fees must be repaid before exiting. This creates a 30-45 day overlap where you may pay for two services simultaneously.

We recommend following this 6-step migration timeline:

Calculate your true Payability costs over 3 months using the gross-to-net framework.

Get approved with your new provider before submitting cancellation. Luca AI offers 10-minute integration with same-day access; Wayflyer takes 3-5 days; Clearco takes 5-7 days.

Submit 30-day written cancellation and request written confirmation.

Document all transactions during the overlap period.

Manually revoke Payability's API access from your marketplace settings.

Verify your first full payout from the new provider and check UCC filing status within 60 days.

At $100K/month gross and 2% rate, budget approximately $2,000 as your switching cost. Plan transitions for Q1 or Q2 to avoid introducing cash flow uncertainty during Q4 peak season.

Does Payability file a UCC lien and can it block other business financing?

Yes. Payability files a UCC-1 lien on your business when you take an Instant Advance. While this is standard practice for merchant cash advances, the critical issue is the removal process after payoff. Multiple sellers on Trustpilot report UCC filings remaining active for 2+ years after full repayment, directly impeding their ability to secure bank loans, SBA loans, or other secured financing.

UCC filings can persist for up to five years if you don't actively request removal. Some lenders will refuse to extend credit while an active lien from another provider exists on your record. We recommend demanding written confirmation of the removal timeline before signing any advance agreement.

Key differences across providers:

Payability: UCC lien filed for Instant Advance; removal delays documented

Wayflyer, Clearco, 8fig, and SellersFi: UCC lien filed

If you have already paid off a Payability advance and the lien persists, send a formal demand letter requesting immediate termination of the UCC filing.

What happens to my Payability financing if my Amazon account gets suspended?

If Amazon suspends your seller account while you are enrolled with a financing provider, the financial exposure varies dramatically. With Payability, Instant Access fees continue accruing on your gross sales balance while payouts are frozen. Instant Advance must still be repaid in full, plus accrued weekly fees, regardless of payout status. The UCC lien remains on file throughout the suspension period.

Provider-by-provider suspension impact:

Payability: Fees accrue; full Advance repayment required; UCC lien persists

Wayflyer: Revenue-share pauses if zero sales, but UCC lien persists

Clearco: ACH-based repayment from your bank continues regardless of marketplace status

Amazon Lending: Both sales and lending facility can freeze simultaneously

Luca AI: Small, frequent advances ($10K-$50K) limit maximum exposure; disbursal pauses automatically if account health degrades; no UCC lien

We recommend maintaining 1-2 months of repayment obligations in liquid reserves outside your marketplace ecosystem. Providers using frequent small advances inherently limit worst-case financial exposure versus single large lump-sum models.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.png)