Merchant Cash Advance for Startups and Small Businesses: The Complete Guide to MCA Financing in 2026

14

mins read

TL;DR

MCAs are purchases of future receivables, not loans, with effective APRs of 40-350% that most founders miscalculate using factor rates alone. Startups with 500+ credit scores and $10K+ monthly revenue can qualify, but platform MCAs like Shopify Capital skip credit checks entirely. The SBA can no longer refinance MCA debt as of June 2025, closing the most common exit ramp for overleveraged businesses. Predatory red flags include stacking, confessions of judgment, double-dipping holdbacks, and factor rates above 1.5 on sub-9-month terms. Alternatives like revenue-based financing, SBA microloans, and dynamically-priced capital from Luca AI offer lower costs with better-aligned repayment structures. A structured four-step exit framework covering assessment, negotiation, refinancing, and post-MCA financial path can reduce MCA payments by up to 89%.

Q1: What Is a Merchant Cash Advance and Why Isn't It a Loan? [toc=MCA Definition and Legal Status]

A merchant cash advance (MCA) is a commercial transaction in which a financing provider purchases a portion of a business's future credit card and debit card sales at a discount, in exchange for delivering an upfront lump sum of cash. The business then repays by automatically surrendering a fixed percentage of its daily or weekly card sales until the purchased amount is fully collected.

⚠️ An MCA Is Not a Loan: Here's Why That Matters

The critical legal distinction: in an MCA, the provider is buying future receivables, not lending money. This means MCAs historically fall outside the regulatory frameworks that govern traditional lending:

No Truth in Lending Act (TILA) coverage: providers are not required to disclose an APR equivalent

No usury law protection: state interest rate caps typically do not apply

No standardized disclosure: total cost, effective interest rate, and fee breakdowns are not mandated in most states

Limited borrower recourse: consumer protection statutes designed for loans often do not cover MCA agreements

This classification has allowed MCA providers to operate with minimal regulatory oversight for over two decades. However, the landscape shifted dramatically in January 2025, when New York Attorney General Letitia James announced a $1 billion-plus judgment against Yellowstone Capital for issuing predatory loans disguised as merchant cash advances to over 18,000 small businesses. The settlement cancelled $534 million in outstanding merchant debts, banned Yellowstone from the MCA business entirely, and signaled that courts are increasingly willing to reclassify MCAs as illegal loans when the structure functions as one.

💰 How the MCA Industry Got Here

MCAs originated in the early 2000s as a niche financing product for restaurants and retail stores with high daily credit card volume. The model expanded significantly after the 2008 financial crisis, when banks tightened small business lending standards and rejection rates climbed. By 2020, platform-embedded MCAs from Shopify Capital, Stripe Capital, and Amazon's partnership with YouLend brought the product into the mainstream e-commerce ecosystem.

Today, the global MCA market is valued at $20.99 billion in 2026, projected to reach $26.87 billion by 2030 at a 6.4% CAGR. Approximately 34.75 million small businesses in the U.S. alone drive MCA financing demand.

📊 Why Small Businesses Turn to MCAs Despite the Cost

The 2024 Federal Reserve Small Business Credit Survey reveals the core driver: access. Among small businesses that applied for financing, applicants at small banks were fully approved only 54% of the time, and satisfaction with online lenders fell sharply, dropping to just 2% net satisfaction in 2024 (down from 15% in 2023). High interest rates and unfavorable repayment terms were the most common complaints at online lenders.

MCAs fill this gap with approval rates exceeding 80%, minimal documentation, and funding in 1 to 3 days:

MCA vs. Traditional Bank Loan

Dimension

Merchant Cash Advance

Traditional Bank Loan

⏰ Funding Speed

1 to 3 business days

4 to 12 weeks

✅ Approval Rate

80%+

~50% (full approval)

Credit Requirement

500 to 550 minimum

680+ typical

Repayment

% of daily sales or fixed ACH

Fixed monthly installments

Regulatory Oversight

Minimal (shifting in 2026)

Full TILA/state regulation

How Luca AI Helps You Evaluate an MCA Before You Commit

Luca AI functions as an AI intelligence layer over your entire business data warehouse, connecting Shopify, Stripe, Xero, and bank accounts into a single reasoning engine. Before accepting any MCA offer, ask Luca: "If I take a $50K advance at 1.35 factor rate, what happens to my cash runway over the next 6 months given my current sales velocity?" Luca simulates the repayment impact against your real historical data, flags months where holdback may strain operating cash, and pushes weekly cash runway forecasts via Slack or email so capital decisions are modeled, not guessed.

Q2: How Does Merchant Cash Advance Financing Work? (Complete Step-by-Step Mechanics) [toc=How MCA Financing Works]

The MCA process follows five stages from application to full repayment. Each stage involves specific documents, timelines, and mechanics that vary depending on whether you use a platform-embedded provider (Shopify Capital, Stripe Capital) or an independent MCA company.

The MCA process follows five distinct stages, each with specific documents, timelines, and mechanics that founders must understand before signing.

Step 1: Application and Underwriting

Independent MCA providers (Credibly, Rapid Finance, OnDeck) typically require:

Platform-embedded MCAs work differently. Shopify Capital, Stripe Capital, and Square Capital auto-underwrite using your existing transaction history on their platform, with no separate application and no document uploads. If you process cards through Stripe, Stripe Capital already has the data it needs to generate an offer automatically.

MCA providers partner directly with payment processors (Fiserv, Square, Stripe, Worldpay) to automate the daily sales split. The processor diverts the agreed holdback percentage to the MCA provider before depositing the remainder into your account.

Step 2: The Offer: Factor Rates and Holdback Percentages

Once underwriting is complete (often within hours), the provider issues an offer built on three components:

Advance amount: the lump sum you receive (typically $5K to $500K)

Factor rate: the multiplier determining your total repayment (typically 1.1 to 1.5)

Holdback percentage: the share of daily sales automatically withheld (typically 5 to 20%)

Holdback rates are determined by your monthly revenue, industry risk profile, time in business, and card processing volume. Higher volume and lower risk translate to lower holdbacks:

Holdback Rates by Revenue Tier

Monthly Card Volume

Typical Holdback Range

Risk Tier

$5K to $15K

15 to 20%

Higher risk, early-stage

$15K to $50K

10 to 15%

Moderate risk

$50K to $100K

8 to 12%

Lower risk, established

$100K+

5 to 10%

Lowest risk, strong volume

Step 3: Funding and Repayment Model 1: Percentage Holdback

Funds are deposited in 1 to 3 business days. Repayment begins immediately via automated split at the processor level.

💰 Worked example: $50,000 advance x 1.35 factor rate = $67,500 total repayment. At 15% holdback on $2,000/day average sales = $300/day. Estimated repayment: ~225 business days (~11 months).

This model genuinely flexes with revenue. If daily sales drop to $1,200 during a slow month, the daily payment drops to $180. If sales surge to $4,000 during peak season, the daily payment rises to $600, accelerating repayment.

Step 4: Repayment Model 2: Fixed Daily/Weekly ACH Debits

⚠️ Some providers use fixed daily ACH withdrawals regardless of actual sales volume. If your sales drop 40%, you still owe the same daily amount. This structure is functionally identical to a loan, and it is the model courts targeted in the Yellowstone Capital judgment.

Funding Speed by Provider Type

Provider Type

Funding Speed

Repayment Model

Platform MCAs (Stripe, Shopify)

⏰ 1 to 2 business days

Percentage holdback (flexes)

Independent MCA brokers

⏰ 2 to 3 business days

Mixed (holdback or fixed ACH)

Bank-affiliated MCAs

⏰ 5 to 7 business days

Typically fixed ACH

"A merchant cash advance is a business funding option that you can repay using a percentage of sales, plus a small fee. It's best for small businesses that accept card payments from their customers." u/Whole-Shallot-3374, r/smallbusiness Reddit Thread

How Luca AI Models Your Repayment Scenario

Luca AI connects to your Shopify, Stripe, and bank accounts to simulate both repayment structures against your actual daily sales patterns, including seasonal fluctuations. Ask: "Based on my last 90 days of sales, how long will it take to repay a $50K advance at 15% holdback, and what's my lowest cash-on-hand day during repayment?" Luca runs the simulation using your real transaction data, not provider estimates.

Q3: What Does a Merchant Cash Advance Really Cost? (Factor Rate, APR Conversion and Cost Calculator) [toc=True MCA Cost and APR]

Factor rates are the primary pricing mechanism for MCAs, and they are specifically designed to make the cost appear lower than it actually is. A factor rate of 1.35 sounds like 35%. It is not. Understanding the true annualized cost requires converting the factor rate into an APR equivalent.

💸 The Factor Rate to APR Conversion Formula

The standard conversion formula:

APR = ((Factor Rate - 1) / Factor Rate) x (365 / Repayment Term in Days) x 100

Worked example: A $50,000 advance at 1.35 factor rate, repaid over 180 days:

APR = ((0.35 / 1.35) x (365 / 180)) x 100 = 52.6% APR

The same 1.35 factor rate repaid in 90 days:

APR = ((0.35 / 1.35) x (365 / 90)) x 100 = ~105.2% APR

⚠️ The critical insight: the faster you repay, the higher your effective APR, the exact opposite of traditional loans where early repayment reduces total interest. MCA providers benefit when your sales are strong because they collect their fixed total faster at a higher annualized rate.

The same factor rate produces wildly different effective APRs depending on repayment speed, the exact opposite of traditional loans where early repayment saves money.

Factor Rate to APR Conversion Table

Factor Rate to APR Conversion by Repayment Term

Factor Rate

90 Days

180 Days

270 Days

365 Days

1.15

52.8%

26.4%

17.6%

13.0%

1.20

67.4%

33.7%

22.5%

16.7%

1.25

81.1%

40.6%

27.0%

20.0%

1.30

93.5%

46.8%

31.2%

23.1%

1.35

105.2%

52.6%

35.1%

26.0%

1.40

115.6%

57.8%

38.5%

28.5%

1.50

135.2%

67.6%

45.1%

33.3%

Hidden Fees That Inflate Cost Beyond the Factor Rate

The factor rate is not the complete picture. Additional fees often embedded in MCA agreements include:

Origination fees: 1 to 5% of advance amount (a $100K advance may carry a $3,000 to $5,000 origination fee)

Underwriting fees: $250 to $500 flat

Administrative/processing fees: $100 to $300

Broker commissions: 1 to 10% of advance, typically invisible to the borrower and embedded in the factor rate

❌ The early repayment trap: Unlike traditional loans where paying off principal early reduces total interest owed, most MCA contracts require the full purchased amount regardless of repayment speed. You pay the same $67,500 on a $50K advance whether it takes 6 months or 3 months, but the annualized cost doubles.

💰 MCA Cost Calculator: Three Scenarios

MCA Cost Calculator Across Three Advance Amounts

Scenario

$25K Advance

$50K Advance

$100K Advance

Factor Rate 1.20

Total: $30,000 / Fee: $5,000

Total: $60,000 / Fee: $10,000

Total: $120,000 / Fee: $20,000

Factor Rate 1.35

Total: $33,750 / Fee: $8,750

Total: $67,500 / Fee: $17,500

Total: $135,000 / Fee: $35,000

Factor Rate 1.50

Total: $37,500 / Fee: $12,500

Total: $75,000 / Fee: $25,000

Total: $150,000 / Fee: $50,000

Daily Payment (15% holdback, $3K/day sales)

$450/day

$450/day

$450/day

Est. Repayment (at $450/day)

~67 days

~150 days

~300 days

"It is basically a payday loan for businesses. I don't doubt it pays well, but it is a very predatory product. These companies are generally pretty predatory and although not necessarily doing anything illegal, I'd imagine it's hard to sell a 50%+ interest loan to a struggling small business owner and feel good about it." u/Bodacious_Dad_Bod, r/sales Reddit Thread

How Luca AI Calculates Your True Cost Automatically

Luca AI eliminates manual APR conversion by running cost analysis against your actual business data. Ask: "What's the true APR of a $50K advance at 1.35 based on my current daily sales velocity?" Luca pulls your real Shopify and Stripe transaction data, simulates repayment timing accounting for your seasonal patterns, and returns an effective APR adjusted for your specific sales cadence rather than generic estimates.

Q4: Who Qualifies for a Merchant Cash Advance? (Eligibility for Startups, E-Commerce and Small Businesses) [toc=MCA Eligibility Requirements]

MCA eligibility is fundamentally different from traditional loan qualification. The primary underwriting criterion is not your credit score or asset base; it is your daily credit and debit card processing volume. If your business generates consistent card sales, you are likely eligible for some form of MCA regardless of credit history.

✅ General Eligibility Requirements

Most MCA providers evaluate four criteria:

Minimum credit score: 500 to 600 (significantly lower than the 680+ required for SBA loans)

Minimum monthly revenue: $5,000 to $15,000 in card sales

Minimum time in business: 3 to 12 months depending on provider

Card processing volume: The single biggest factor in approval and terms; higher volume means lower holdback rates, better factor rates, and larger advance amounts

Unlike bank loans, MCAs do not require collateral, audited financials, or multi-year tax returns. Providers care about the velocity and consistency of your future sales, not your balance sheet history.

Startup Eligibility Matrix by Provider

MCA Provider Eligibility Requirements for Startups

Provider

Min. Time in Business

Min. Monthly Revenue

Min. Credit Score

Platform Required?

Shopify Capital

~6 months on Shopify

Based on Shopify sales

No credit check

✅ Shopify only

Stripe Capital

~3 to 6 months on Stripe

Based on Stripe volume

No credit check

✅ Stripe only

PayPal Working Capital

3+ months

$15K+ annual PayPal sales

No credit check

✅ PayPal Business

Square Capital

Varies

Based on Square volume

No credit check

✅ Square only

Credibly

6+ months

$15K/month

500+

❌

Rapid Finance

6+ months

$10K/month

500+

❌

OnDeck

12+ months

$100K+ annual

625+

❌

🏪 Industry-Specific Qualification Differences

Not all businesses qualify equally. MCA eligibility is closely tied to how your customers pay:

Restaurants and food service: ✅ High fit. High daily card volume makes qualification straightforward, though thin margins mean holdback sizing must be conservative.

E-commerce / DTC brands: ✅ High fit through platform MCAs (Shopify Capital, Stripe Capital). Independent MCA providers may apply higher holdbacks due to return rate risk.

Retail stores: ✅ Medium-high fit. Consistent card volume, but seasonal swings can make fixed-ACH models dangerous during slow months.

B2B service businesses: ❌ Low fit. Revenue arrives monthly or quarterly via invoice/wire, not daily card transactions. Limited MCA options.

SaaS companies: ❌ Low fit. Recurring subscription revenue is typically collected via ACH, not card processing. Revenue-based financing is better suited.

🚀 Startup-Specific Guidance: A Decision Tree

For early-stage businesses, the timeline matters more than the credit score:

Less than 3 months operating: MCAs are not available (no receivables to purchase). Explore grants (SBA, SBIR, state programs), equity crowdfunding, or accelerator programs.

3 to 6 months, $5K+/month: Platform-embedded MCAs only (Shopify Capital, Stripe Capital, PayPal Working Capital). Auto-underwritten, no external application.

6 to 12 months, $10K+/month: Independent MCA providers become available (Credibly, Rapid Finance). Compare offers carefully; factor rates for newer businesses skew toward 1.3 to 1.5.

12+ months, $100K+/year: Full range of options unlocked, including SBA microloans (6 to 13% APR), business lines of credit, and revenue-based financing; all cheaper than MCAs.

"Small business drowning in a merchant cash advance or loan? Here's what you need to know... I've seen many small business owners struggle with overwhelming debt at various stages of their journey." u/AZLawFirm, r/legaladvice Reddit Thread

How Luca AI Maps Your Current Eligibility

Luca AI analyzes your real-time revenue trends, processing volume, and cash position to determine which capital products you currently qualify for, and projects when you will unlock better options. Ask: "Based on my current monthly revenue growth, when will I qualify for an SBA microloan?" Luca models your trajectory against each provider's eligibility thresholds and delivers a data-backed timeline, not a guess.

Q5: What Are the Pros, Cons, and Best Use Cases for Merchant Cash Advances? [toc=Pros, Cons and Use Cases]

Merchant cash advances offer a clear tradeoff: unmatched funding speed and accessibility in exchange for the highest cost of capital available to small businesses. Whether the tradeoff makes sense depends entirely on your use case, margins, and the projected ROI of the capital deployed.

✅ Pros of Merchant Cash Advances

⏰ Fastest funding available: 1 to 3 business days vs. 4 to 12 weeks for SBA loans

Accessible to more businesses: Credit scores as low as 500 accepted; no collateral required

Revenue-linked repayment: Percentage holdback model flexes with daily sales (percentage-based only; fixed ACH does not flex)

No equity dilution: 100% ownership retained regardless of advance size

No personal guarantee with most providers: Business assets only

❌ Cons of Merchant Cash Advances

💸 Highest cost of capital: Effective APR ranges from 40% to 350% depending on factor rate and repayment speed

Daily cash drain: Holdback of 5 to 20% reduces daily operating cash flow immediately

No credit building: MCAs are not reported to business credit bureaus; they don't strengthen your credit profile

Debt cycle risk: Stacking MCAs to cover shortfalls is the #1 path to insolvency

Early repayment trap: Paying off faster increases effective APR without reducing total cost

💰 Best Use Cases for E-Commerce and Small Businesses

Seasonal Inventory Funding

A DTC brand takes a $40K MCA in August to fund Q4 inventory, repaying from holiday sales by January. The seasonal revenue spike absorbs the holdback without straining operations.

Restocking Proven Best-Sellers

A Shopify brand's top SKU is selling out. A $25K MCA funds the restock. Product margin (60%+) covers the MCA fee ($8,750 at 1.35 factor) and generates net profit.

Emergency Payroll Coverage

A restaurant bridges a 2-week payroll gap after an unexpected slow month. The MCA covers $15K in immediate obligations while revenue normalizes.

⚠️ When NOT to use an MCA: Covering operating losses with no clear path to recovery, funding speculative product launches without proven demand, or bridging debt payments on existing obligations.

MCA vs. Equity Dilution: The Math Founders Ignore

For startup founders weighing MCA against equity: a $100K MCA at 1.35 factor rate costs $35,000 in fees. A $100K equity raise at a $2M valuation costs 5% of your company. At a $20M exit, that 5% is worth $1,000,000. The MCA costs $35K; the equity costs $1M. For short-term, high-ROI use cases where capital generates clear returns within 6 to 12 months, MCAs can be dramatically cheaper than dilution.

How Luca AI Offers Speed Without MCA-Level Costs

For e-commerce founders who need capital velocity without factor-rate pricing, Luca AI offers same-day capital deployment at dynamically-priced rates that adjust to your real-time business health. Rates decrease as your performance improves, the opposite of static MCA factor rates. No personal guarantees, no fixed daily debits, and capital sized to what you actually need rather than the maximum a provider can profit from.

Q6: Top MCA and Capital Providers Compared: How to Choose the Right One for Your Business [toc=Provider Comparison 2026]

With dozens of MCA and capital providers operating in 2026, choosing the right one can mean the difference between capital that accelerates growth and capital that suffocates it. The comparison below evaluates nine providers across the metrics that matter most: cost, speed, flexibility, and terms.

📊 2026 Provider Comparison Table

2026 MCA and Capital Provider Comparison

Provider

Advance Range

Cost / Factor Rate

⏰ Funding Speed

Min. Revenue

Repayment

Personal Guarantee

Luca AI

€10K to €500K

Dynamically priced (decreases as business health improves)

Same-day

€1M+ annual

Revenue-linked, flexible

❌ None

Credibly

$5K to $600K

1.09 to 1.45 factor

1 to 2 days

$15K/mo

Daily/weekly ACH

Varies

OnDeck

$5K to $250K

1.1 to 1.5 factor

1 to 3 days

$100K+ annual

Daily/weekly ACH

✅ Required

Rapid Finance

$5K to $10M

1.16 to 1.45 factor

24 hours

$10K/mo

Daily ACH

Varies

Stripe Capital

$2K to $305K

Varies by merchant

1 to 2 days

Stripe volume based

% of Stripe sales

❌ None

Shopify Capital

Up to $2M

Fixed fee (varies)

1 to 3 days

Shopify sales based

% of daily sales

❌ None

PayPal Working Capital

$1K to $300K

Single fixed fee

Instant

$15K+ annual PayPal

% of PayPal sales

❌ None

Clearco

$10K to $20M

6 to 12% flat fee

1 to 3 days

$10K/mo

Weekly revenue share

❌ None

Fundbox

$1K to $150K

4.66 to 8.99% per term

Next business day

$30K+ annual

Weekly fixed

Varies

💰 Why Luca AI's Dynamic Pricing Changes the Capital Equation

Unlike traditional MCA providers that lock in a factor rate based on a static snapshot of your business at application time, Luca AI uses a dynamic pricing model where each tranche of capital reflects your current business health. Take €50K in March at one rate; if your business improves by April, the next €50K is priced cheaper. Over 12 months, this approach results in lower total capital cost than a single large MCA at a fixed factor rate, while ensuring zero capital sits idle earning nothing for the provider.

How to Choose the Right Provider

Already on Shopify/Stripe/Square/PayPal? Start with your platform's embedded capital. Lowest friction, auto-underwritten, no separate application.

Need >$100K fast? Evaluate Credibly, Rapid Finance, or Clearco for advance size and speed.

Want the lowest total cost with health-based dynamic pricing?Luca AI: rates decrease as performance improves, capital repriced per tranche.

Have 12+ months of history and can wait? SBA microloan at 6 to 13% APR will always be cheaper than any MCA.

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Now I am left looking for another option at short notice which is very annoying!" Joshua Hannan Wayflyer - Trustpilot Verified Review

"Our experience with Wayflyer has been extremely disappointing and professionally damaging. After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute." Geoff Brand Wayflyer - Trustpilot Verified Review

"I would avoid if possible unless you are desperate. At the end of the day they are no different than any merchant advance company, loan shark with insanely high interest rates." Terry Clearco - Trustpilot Verified Review

Q7: What Are the Red Flags of a Predatory MCA? (Contract Warnings, Legal Risks and 2026 Regulation) [toc=Predatory MCA Red Flags]

Score your current or prospective MCA agreement against these 10 red flags. Any single checkmark is a warning. Three or more means consult a business attorney before signing.

Any single red flag is a warning; three or more means consult a business attorney before signing any MCA agreement.

⚠️ 10-Point Predatory MCA Red Flag Checklist

❌ Confession of Judgment (COJ) clause: Allows the provider to seize assets without trial or notice

❌ Factor rate above 1.4 with repayment under 6 months: Effective APR exceeds 100%

❌ Fixed daily payments labeled "variable": The contract says holdback flexes, but payments are fixed ACH regardless of sales

❌ No clear disclosure of total repayment amount: You can't find the actual dollar amount you owe

❌ Personal guarantee required: Your personal assets (home, savings) become collateral

❌ Early repayment doesn't reduce total amount owed: You pay the full purchased amount regardless of speed

❌ Provider encourages stacking multiple MCAs: A sign they prioritize volume over your business health

❌ UCC-1 blanket lien on ALL business assets: Should be limited to receivables, not equipment, inventory, and IP

❌ Mandatory arbitration in a distant state: No dispute resolution mechanism accessible to you

❌ Broker commission exceeds 5%: Often invisible to you, embedded in the factor rate

📋 How to Read and Evaluate an MCA Contract

Key Sections to Locate and Scrutinize

"Purchase Price" = Your advance amount (what you receive)

"Purchased Amount" = Total you owe (advance x factor rate)

"Specified Percentage" = Your holdback rate

"Reconciliation" clause = Whether you can request payment adjustment if sales drop (if this clause is buried or absent, major red flag)

"UCC-1 filing" scope = Check if it's limited to receivables or blankets all assets

⚠️ UCC filings explained: Providers file a UCC-1 lien on your business, which appears on your credit profile and can block you from securing other financing. The lien remains until the provider files a termination statement, and many providers delay this even after full repayment.

What Happens If You Default, and Why Stacking Kills Businesses

Default consequences include: bank account freezes (via the ACH authorization you signed), lawsuits, COJ enforcement (in states that still allow it), debt sale to aggressive collectors, and asset seizure under the UCC-1 lien.

MCA stacking, taking a second or third advance to cover shortfalls from the first, is the single most dangerous practice in MCA financing. Combined holdbacks can reach 25 to 40% of daily revenue, suffocating cash flow entirely.

"I was lured by the promise of fast cash with minimal paperwork and hassle. This merchant cash advances are notorious for their exorbitant fees and daily repayment structures. The MCA industry's lack of regulation allows unscrupulous lenders to prey on vulnerable small business owners." u/deleted, r/smallbusiness Reddit Thread

🏛️ 2026 Regulatory Landscape, Tax Treatment and Credit Impact

Federal and State-Level Regulation

Federal: MCAs remain largely unregulated at the federal level, though the CFPB has increased scrutiny. State-level: New York banned COJs for out-of-state borrowers in 2019. The 2025 NY AG Yellowstone Capital $1B+ judgment reclassified certain MCAs as illegal loans, cancelling $534 million in merchant debts. California, Virginia, and Utah now require providers to disclose APR-equivalent costs under commercial financing disclosure laws.

Tax deductibility: MCA fees (total repayment minus advance amount) are generally deductible as a business expense. Credit impact: MCAs are not reported to credit bureaus; they don't build credit. However, UCC filings are visible and can block other financing until terminated.

How Luca AI Eliminates Every Item on This Checklist

Luca AI's capital terms are structured to remove each red flag: no confessions of judgment, no personal guarantees, no blanket UCC liens, transparent total cost disclosure, dynamically-priced rates based on real-time business health, and capital sized to what you need, not the maximum a provider can profit from.

Q8: Real MCA Case Studies: When It Works, When It Destroys Cash Flow [toc=MCA Case Studies]

The difference between a successful MCA and a business-ending one is not luck. It is whether the founder modeled the cash flow impact before signing. These three anonymized case studies, drawn from patterns reported across small business forums and MCA advisory firms, illustrate the range of outcomes.

🏪 Case Study 1: Restaurant, Successful Seasonal Use

The Situation

Maria owns a family restaurant generating $180K/year in card sales. She needs $30,000 to renovate the patio before summer season.

The MCA Terms

$30K advance at 1.22 factor rate. Holdback: 12% of daily card sales (~$60/day average). Total repayment: $36,600.

The Outcome

Patio renovation completed in 3 weeks

Summer revenue increased by $45,000 due to expanded seating

MCA fully repaid in ~8 months

💰 Net profit after MCA cost: $8,400

Why it worked: Specific, short-term use case with strong seasonal ROI. The holdback was sized within margin tolerance (12% on a restaurant running 15 to 20% net margin during summer peak). Maria never felt cash-strapped because the revenue uplift from the patio exceeded the daily holdback from day one.

💸 Case Study 2: E-Commerce Startup, The Stacking Death Spiral

The Situation

Raj runs a DTC supplements brand on Shopify doing $25K/month. He takes a $40K MCA at 1.38 factor rate to fund inventory for a new product launch.

What Went Wrong

New product underperforms; sales drop to $18K/month

Daily holdback of $170/day (15%) eats into operating cash

Takes a second MCA ($25K at 1.45 factor) to cover the cash shortfall, classic stacking

The Damage

Total owed across both MCAs: $91,450

Combined daily payments: $290/day on $600/day sales (48% holdback)

Cash flow suffocated; unable to fund marketing, restock winning SKUs, or service both advances

"I've seen businesses where 40 to 60% of their daily gross revenue disappears before they can cover labor or materials. By taking multiple advances, you often end up in a 200%+ APR cycle." u/FundingAdvisory, r/Businessloans Reddit Thread

🛍️ Case Study 3: Retail, Strategic Inventory Acquisition

The Situation

Priya operates a boutique retail chain doing $50K/month in card sales. A competitor is liquidating, offering premium inventory at 60% below wholesale.

The MCA Terms

$75K advance at 1.28 factor rate. Holdback: 10% of daily sales ($167/day). Total repayment: $96,000.

The Outcome

Liquidation inventory purchased at 60% below wholesale

Generated $210K in revenue at 65% gross margin

MCA fully repaid in ~8 months

💰 Net profit after MCA cost: $115,500

Why it worked: Clear, quantifiable ROI exceeding MCA cost by 5x. The opportunity was time-sensitive, requiring capital in 48 hours, which only an MCA could deliver. The product had proven market demand (same SKUs at full wholesale had sold consistently).

The Contrast, and How Luca AI Prevents Case Study 2

The difference between Maria (Case 1) and Raj (Case 2) is not luck; it is pre-decision modeling. Luca AI prevents Raj's scenario by simulating the full outcome before signing. Ask: "If I take this $40K advance at 1.38 and my new product hits only 60% of projected sales, can I still make payroll and service the advance?" Luca models your actual sales forecast, existing costs, holdback impact, and cash runway into one answer, so you stack out of confidence, never desperation.

Q9: MCA Alternatives: What Else Should You Consider? (Full Comparison and Decision Framework) [toc=MCA Alternatives Comparison]

In 2026, small businesses have more capital options than ever: MCAs, SBA loans, online term loans, business lines of credit, revenue-based financing, invoice factoring, grants, and crowdfunding. But most founders evaluate them on only two dimensions (speed and approval odds), ignoring the dimension that matters most: total cost relative to the ROI of the use case.

📊 Full Alternatives Comparison Table

Capital Alternatives Comparison for Small Businesses in 2026

Product

Typical APR/Cost

⏰ Funding Speed

Min. Credit Score

Repayment

Collateral/Guarantee

Best For

Luca AI Dynamic Capital

Dynamically priced (decreases as health improves)

Same-day

550+

Revenue-linked, flexible

❌ No PG

E-commerce brands needing fast, fairly-priced capital

Merchant Cash Advance

40 to 350% effective

1 to 3 days

500+

Daily holdback or fixed ACH

Varies

Emergency/short-term high-ROI needs

SBA Microloan

8 to 13%

4 to 12 weeks

680+

Fixed monthly (up to 7 years)

May require collateral

Low-cost capital for patient borrowers

Online Term Loan (OnDeck, Fundbox)

15 to 80%

1 to 7 days

600+

Fixed monthly/weekly

Varies

Medium-term needs, moderate credit

Business Line of Credit

8 to 60%

1 to 4 weeks

600+

Revolving (interest only on drawn)

Varies

Ongoing working capital

Revenue-Based Financing (Clearco, Wayflyer)

15 to 40% effective

1 to 5 days

Varies

Monthly revenue share

❌ No PG typically

E-commerce inventory/marketing

Invoice Factoring

1 to 5% per invoice

1 to 3 days

530+

Factor collects from your customer

❌ No PG

B2B with outstanding invoices

Grants / Crowdfunding

💰 0% (free)

Weeks to months

N/A

None

None

Pre-revenue startups, mission-driven

⚠️ Critical Update: SBA Can No Longer Refinance MCAs

As of June 1, 2025, the SBA's updated Standard Operating Procedure (SOP 50 10 8) explicitly states: "Merchant cash advance (MCA) and factoring arrangements are not eligible for debt refinancing." This closes what was historically the most common MCA exit ramp: using a low-cost SBA loan to pay off high-cost MCA debt. Business owners can no longer refinance existing MCAs through SBA 7(a) or microloan programs.

💸 Bad-Credit and Startup-Specific Alternatives

If your credit score is below 500:

Platform MCAs (Shopify Capital, Stripe Capital) don't run credit checks; underwriting is based purely on platform transaction history

Invoice factoring evaluates your customers' creditworthiness, not yours

Revenue-based financing providers focus on revenue data, not credit scores

For pre-revenue startups: grants (SBA, SBIR, state programs), equity crowdfunding, and accelerator programs remain the only viable non-dilutive options.

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

"We worked with Clearco for a couple of years and had a great experience early on. Unfortunately, things changed when our account was reassigned. Despite no change in our cash position or risk profile, we started facing stricter cash-on-hand demands that made little sense." Melissa Clearco - Trustpilot Verified Review

🎯 Decision Framework: When to Choose Each Option

✅ Choose MCA if: You need capital in under 48 hours, have high daily card volume, and the use case has projected ROI exceeding 50%+ effective APR

✅ Choose SBA if: You can wait 6+ weeks, have 680+ credit, and want the lowest cost (8 to 13% APR)

✅ Choose RBF if: You want monthly (not daily) repayment tied to revenue with no personal guarantee

✅ Choose Luca AI if: You want same-day capital at rates that reflect your real-time business performance, repriced dynamically with each tranche so you pay less as your business improves

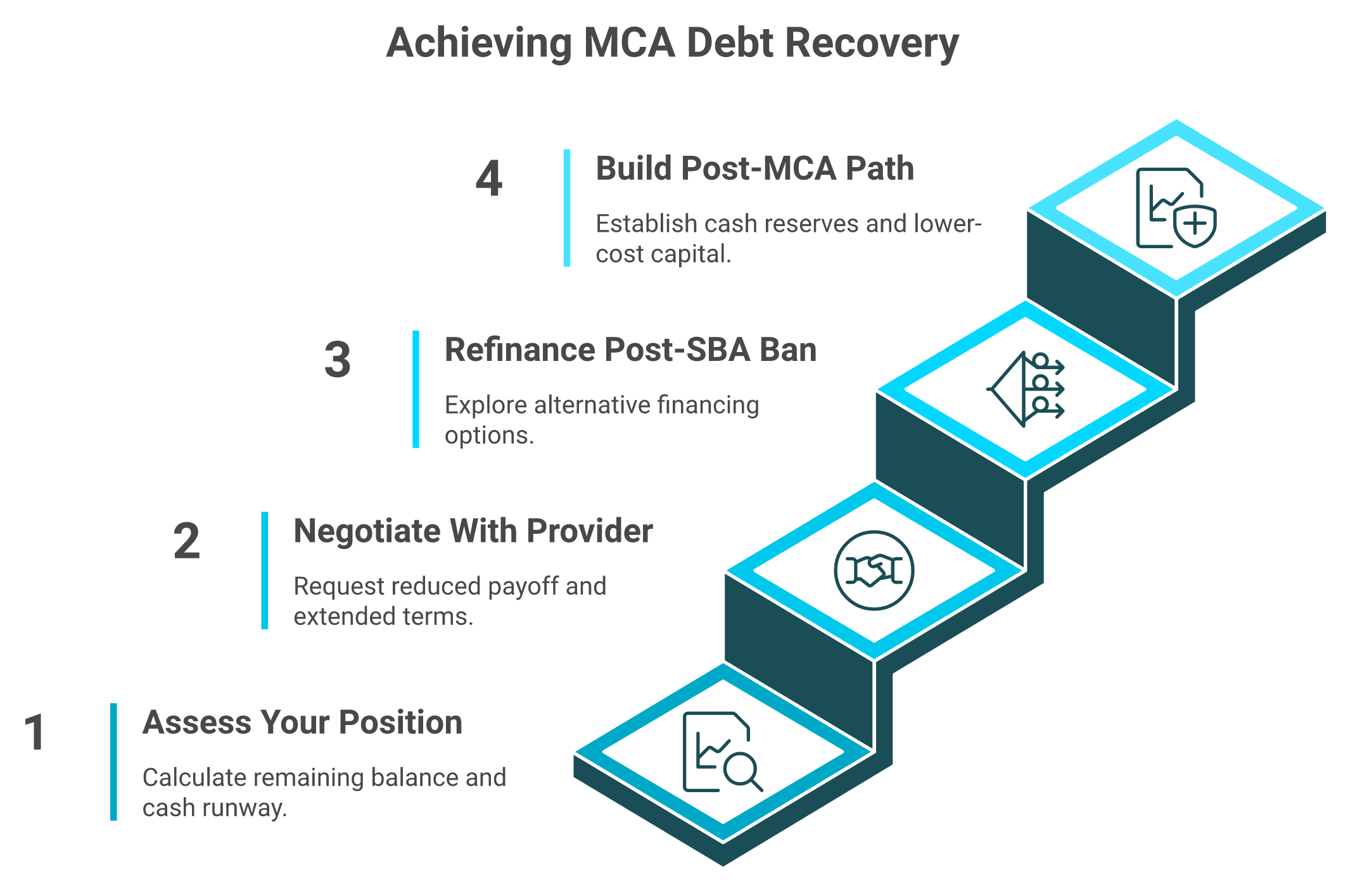

Q10: How to Get Out of MCA Debt: Exit Strategy Framework [toc=MCA Debt Exit Strategy]

If daily MCA holdbacks are draining your cash flow and stacking has compounded the problem, you need a structured exit plan, not another advance. This four-step framework provides a clear path from MCA debt to healthier financing.

Escaping MCA debt requires a structured four-step climb from assessment through negotiation, refinancing, and rebuilding, not another advance.

Step 1: Assess Your Current Position

Calculate three numbers before taking any action:

Total remaining balance across all MCAs (purchased amount minus what's been repaid)

Combined daily holdback as a percentage of daily revenue: if this exceeds 20%, you're in the danger zone

Cash runway at current burn rate: how many days can you operate if revenue drops 25%?

If you have multiple stacked MCAs, prioritize by effective cost. The advance with the highest factor rate and shortest remaining term should be targeted first.

Step 2: Negotiate With Your Current Provider

Many MCA providers will accept a reduced lump-sum payoff (70 to 85% of remaining balance) rather than risk default and collection costs. This negotiation is especially viable if you can demonstrate cash flow distress with bank statements and projections.

⚠️ What to Request

Reduced lump-sum payoff at 70 to 85% of remaining balance

Extended repayment period to lower daily holdback percentage

Temporary holdback reduction during documented slow periods (invoke the "reconciliation" clause if present)

Always get modifications in writing with a signed amendment. If the provider refuses and your contract contains a Confession of Judgment clause or fixed payments labeled as variable, consult an MCA attorney. Courts have increasingly ruled these contracts unenforceable.

"The total payments, both daily and weekly, are simply not manageable. I've attempted to secure traditional loans, reach out to nonprofit lenders, and explore consolidation options, but I keep getting denied because of the existing MCAs." u/ThinkNorth123, r/smallbusiness Reddit Thread

With SBA refinancing of MCAs no longer available as of June 2025, remaining options include:

Business line of credit: Draw only what you need to cover the MCA payoff, then repay at 8 to 60% APR vs. 100%+ effective MCA APR

Revenue-based financing consolidation: Replace multiple stacked MCAs with a single RBF product at 15 to 40% effective cost with monthly (not daily) repayment

Asset-based lending: If you have inventory or equipment, use it as collateral for a lower-cost loan to retire the MCA

MCA workout / debt settlement: Specialized attorneys can negotiate settlements, particularly where contracts are legally vulnerable

"We just helped our client cut their monthly payments from $131,000 to $14,000 by consolidating their MCAs. The existing MCA is paid off, and the payoff is structured into a new loan that is stretched out over a longer term of up to 36 months." u/Competitive_Card4863, r/smallbusiness Reddit Thread

Step 4: Build a Post-MCA Financial Path

Once the MCA is retired:

File a UCC-3 termination request immediately. Remove the lien from your business credit profile. Many providers delay this; follow up aggressively.

Establish a 60-day cash reserve before taking any new capital

Transition to lower-cost capital: business line of credit, RBF, or dynamically-priced capital for future needs

Set a rule: Never take capital where effective APR exceeds the projected ROI of the use case

How Luca AI Fits Into Your Post-MCA Recovery

Luca AI's dynamic capital model is designed to be the financing you graduate into after exiting MCA debt. Same-day funding speed matches MCA velocity, but at dynamically-priced rates that decrease as your business health improves, so the capital that helps you recover also becomes cheaper as you recover. No stacking risk, no fixed daily debits, no confessions of judgment.

Q11: Frequently Asked Questions About Merchant Cash Advances in 2026 [toc=MCA FAQ 2026]

Is a merchant cash advance a good idea?

It depends entirely on use case. ✅ Good for short-term, high-ROI capital needs where projected return exceeds the 40 to 150%+ effective APR: proven campaign scaling, inventory with guaranteed demand, or time-sensitive opportunities. ❌ Bad for covering operating losses, bridging cash flow gaps without a clear repayment path, or any scenario where ROI doesn't exceed total MCA cost.

Can you get a merchant cash advance with bad credit?

Yes. Most independent providers accept credit scores of 500 to 550. Platform-based MCAs (Shopify Capital, Stripe Capital, Square Capital, PayPal Working Capital) don't run credit checks at all; they underwrite purely on transaction history within their platform.

💰 What happens if you default on a merchant cash advance?

Providers may freeze your business bank account via ACH authorization, file a UCC-1 lien claim against business assets, pursue legal action, enforce a Confession of Judgment (in states where still permitted), or sell the debt to collections. The 2025 NY AG Yellowstone Capital judgment expanded borrower protections in New York, but most states still offer limited recourse.

Are merchant cash advance fees tax deductible?

Yes. The fee portion (total repayment minus advance amount) is generally deductible as a business expense in the year it's paid. Consult a tax professional for classification specifics. Some accountants categorize MCA fees as "cost of financing" rather than "interest expense" since MCAs are technically not loans.

⚠️ Can you have multiple merchant cash advances at the same time?

Technically yes; this is called "stacking." However, stacking is one of the most dangerous practices in MCA financing. Combined holdbacks from multiple providers can reach 25 to 40% of daily revenue, suffocating cash flow and triggering a debt spiral. Many providers prohibit stacking via exclusivity clauses in their contracts.

What is the difference between a merchant cash advance and a business loan?

MCA vs. Business Loan: Key Differences

Dimension

Merchant Cash Advance

Business Loan

Legal structure

Purchase of future receivables

Borrowed money with interest

Regulation

Minimal (varies by state)

Full TILA/state regulation

APR disclosure

Not required (most states)

Required by law

Credit building

❌ Not reported to bureaus

✅ Reported to bureaus

Repayment

Daily % of sales or fixed ACH

Fixed monthly installments

How long does it take to get a merchant cash advance?

⏰ Platform MCAs (Stripe Capital, Square Capital): 1 to 2 business days, no separate application

⏰ Independent providers (Credibly, Rapid Finance): 1 to 3 business days from application to funding

⏰ Bank-affiliated MCAs: 5 to 7 business days

How do you calculate the true cost of a merchant cash advance?

Use the APR conversion formula: APR = ((Factor Rate - 1) / Factor Rate) x (365 / Repayment Term in Days) x 100. Example: A 1.35 factor rate repaid over 180 days is approximately 52.6% APR. The same factor over 90 days is approximately 105% APR. Always calculate effective APR rather than relying on the factor rate alone.

How Luca AI Helps You Answer Every Question Above With Your Own Data

Every question in this FAQ comes down to having enough intelligence about your own business to make the right capital decision. Luca AI's simulation engine models any MCA scenario against your real Shopify, Stripe, and Xero data, so you answer these questions with your actual numbers and seasonal patterns, not industry averages. Ask Luca before you sign.

FAQ's

How do you convert a merchant cash advance factor rate to an actual APR?

Most MCA providers quote a factor rate (e.g., 1.35) instead of an APR, which makes the true cost appear deceptively low. We see this confusion constantly among e-commerce founders evaluating capital options.

The conversion formula is: APR = ((Factor Rate - 1) / Factor Rate) x (365 / Repayment Term in Days) x 100. For example, a 1.35 factor rate repaid over 180 days translates to approximately 52.6% APR. The same 1.35 factor repaid over 90 days jumps to approximately 105% APR.

This is why repayment speed matters enormously. If your daily holdback percentage is high and you repay faster than projected, your effective APR skyrockets, sometimes exceeding 200%. We recommend every founder calculate effective APR before signing any MCA agreement.

With Luca AI's financial management tools, you can model the exact cost of any MCA scenario against your real Shopify and Stripe data, including the impact of faster-than-expected repayment on your effective APR, so you never sign blind.

Can a startup or new e-commerce business qualify for a merchant cash advance?

Yes, but eligibility depends on your revenue history, not your time in business. Most independent MCA providers require a minimum of 3-6 months of bank statements showing $10,000+ in monthly revenue and a credit score of 500-550.

For newer startups, platform-based MCAs offer the easiest path:

Shopify Capital: No separate application required. Offers appear automatically based on your store's transaction history and velocity.

Stripe Capital: Invitation-only, underwritten entirely on Stripe payment volume. No credit check.

PayPal Working Capital: Requires 90 days of PayPal sales history and a PayPal business account.

The critical question is not whether you can qualify, but whether you should take it. MCAs carry effective APRs of 40-350%, so the use case must generate ROI that clearly exceeds the total cost of capital.

We built Luca AI's data analysis engine specifically to help founders model whether their projected ROI justifies the MCA cost, using their actual revenue data and seasonal patterns rather than guesswork.

What happens if you cannot repay a merchant cash advance?

Defaulting on an MCA triggers a cascade of consequences that can cripple your business operations. Because MCAs are structured as purchases of future receivables rather than loans, the enforcement mechanisms differ significantly from traditional debt.

Here is what providers can do:

Freeze your bank account via the ACH authorization you signed at origination

File a UCC-1 lien against all business assets, blocking your ability to secure other financing

Enforce a Confession of Judgment (COJ) in states where still permitted, obtaining a judgment without trial

Redirect platform payouts (Shopify, Stripe) to their account if the contract allows

Sell the debt to collections or pursue legal action directly

The 2025 NY AG Yellowstone Capital judgment expanded borrower protections in New York, but most states still offer limited recourse. If your combined daily holdbacks exceed 20% of revenue, we consider that the danger zone.

Before reaching default, we recommend using cash flow forecasting to model your runway and negotiate with providers proactively. Getting modifications in writing before distress escalates is always cheaper than litigation after the fact.

What are the best alternatives to a merchant cash advance for e-commerce businesses?

In 2026, e-commerce businesses have more capital options than ever, and most of them cost significantly less than MCAs. The best alternative depends on your credit profile, how quickly you need funds, and your repayment preferences.

SBA Microloans (8-13% APR): Lowest cost option, but requires 680+ credit and 4-12 weeks for approval.

Revenue-Based Financing (15-40% effective cost): Providers like Clearco and Wayflyer offer monthly repayment tied to revenue with no personal guarantee. Ideal for inventory and marketing funding.

Business Line of Credit (8-60% APR): Revolving credit where you pay interest only on what you draw. Best for ongoing working capital.

Invoice Factoring (1-5% per invoice): Evaluates your customers' creditworthiness, not yours. Best for B2B businesses.

Dynamically-Priced Capital:Luca AI offers same-day funding at rates that decrease as your business health improves, combining MCA speed with fairer pricing and no personal guarantee.

The critical rule we recommend: never take capital where the effective APR exceeds the projected ROI of the use case. If a campaign will generate 30% returns, funding it at 100%+ APR destroys value regardless of how fast you get the money.

How do you get out of stacked merchant cash advance debt?

Stacked MCAs, where multiple advances compound daily holdbacks to 25-40% of revenue, represent one of the most dangerous debt spirals in small business financing. We recommend a structured four-step exit framework.

Step 1: Assess your position. Calculate your total remaining balance, combined daily holdback as a percentage of daily revenue, and cash runway if revenue drops 25%. If holdbacks exceed 20%, you are in the danger zone.

Step 2: Negotiate. Many providers accept a reduced lump-sum payoff at 70-85% of remaining balance rather than risk default. Request extended repayment terms or temporary holdback reductions in writing.

Step 3: Refinance. As of June 2025, the SBA can no longer refinance MCA debt. Remaining options include business lines of credit, revenue-based financing consolidation, and asset-based lending to replace stacked MCAs with a single, lower-cost product.

Step 4: Rebuild. File a UCC-3 termination immediately, build a 60-day cash reserve, and transition to dynamically-priced capital that decreases in cost as your business recovers.

Real consolidation cases have reduced monthly payments from $131,000 to $14,000 by restructuring stacked MCAs into longer-term products. The key is acting before default, not after.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.