Alternative Lenders for Small Business: 2026 Guide to the Best Non-Bank Funding Options Compared

14

mins read

In this article

TL;DR

Alternative lenders use AI-driven underwriting and open banking APIs to fund businesses in days, not months. The global alternative lending market has reached $556.45 billion in 2026 at 13.8% CAGR. Luca AI ranks #1 for e-commerce with dynamic pricing, instant deployment, and no personal guarantee. MCAs carry 40 to 350% effective APR and bypass most lending regulations, making cost transparency critical. CFPB Section 1071 Tier 1 compliance begins July 2026, but RBF and MCAs remain largely excluded. Match repayment structure to revenue pattern: daily holdback for card-based sales, RBF for recurring revenue.

Q1. What Are Alternative Lenders and How Does Non-Bank Lending Work in 2026? [toc=What Are Alternative Lenders]

Alternative lenders are non-bank entities, including online lenders, fintech platforms, CDFIs, marketplace lenders, and revenue-based financing providers, that offer business financing using technology-driven underwriting instead of legacy credit models. Unlike traditional banks that rely on manual reviews and FICO-centric decisioning, alternative lenders leverage AI/ML credit scoring, real-time bank transaction analysis via open banking APIs, and commerce data from platforms like Shopify and Amazon to evaluate borrowers. This architectural difference is why approval is faster, eligibility requirements are lower, and capital reaches founders in days rather than months.

⏰ How the Mechanics Work

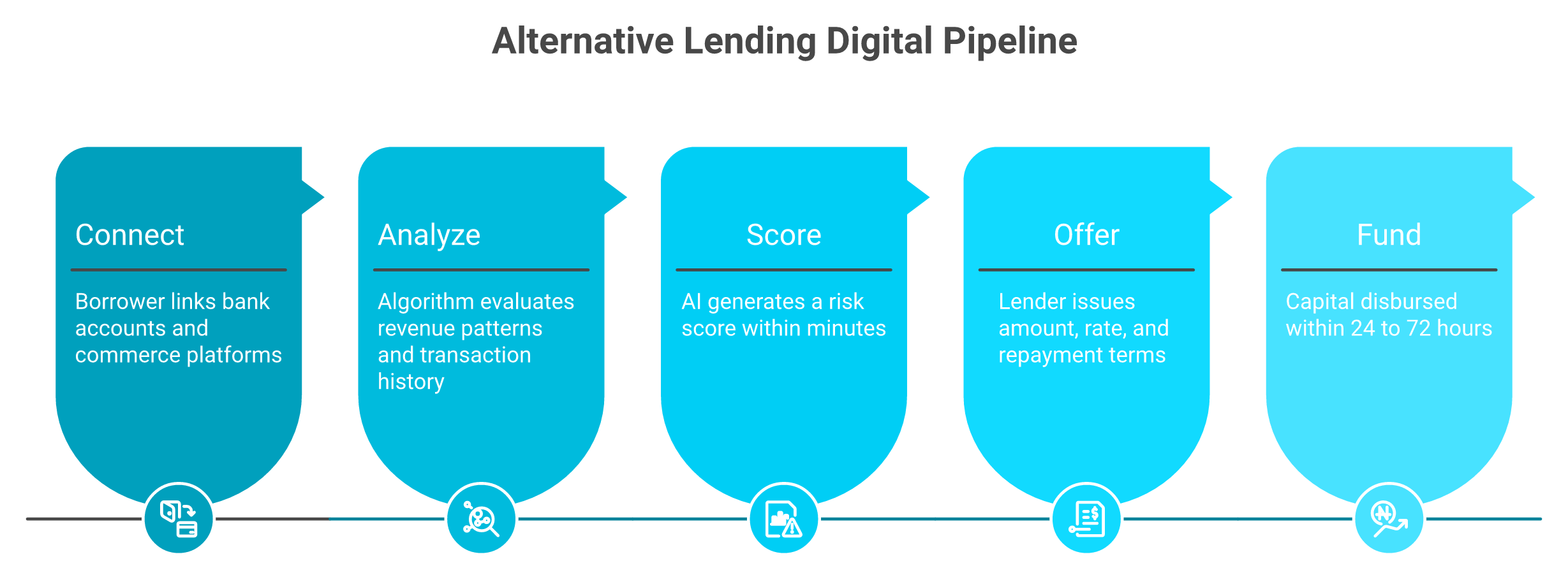

The process follows a streamlined digital pipeline:

Alternative lenders replace the 4-to-8-week bank pipeline with a 5-step digital process that funds businesses in days.

Connect: A borrower links bank accounts and/or commerce platforms (Shopify, Stripe, Amazon).

Analyze: The lender's algorithm evaluates revenue patterns, transaction history, cash flow consistency, and sometimes marketing metrics.

Score: A risk score generates within minutes, not weeks.

Offer: An offer is issued with amount, rate, and repayment terms.

Fund: Capital is disbursed, often within 24 to 72 hours.

Contrast this with the traditional bank pipeline: paper application, manual review, collateral appraisal, committee decision, and 4 to 8 weeks to funding. As one Reddit user noted:

"Cash flow can't afford a 30-day wait for approval. That's where alternative lending steps in. Instead of 'maybes' and manual reviews, you receive AI-driven decisions in hours, not weeks." u/Logical_Landscape, r/Businessloans Reddit Thread

📈 From Post-Crisis Origins to a $556 Billion Market

The 2008 financial crisis created a small business credit vacuum as banks tightened lending standards dramatically. Fintech lenders stepped into the gap: OnDeck (founded 2006), Kabbage (2009), and Funding Circle (2010) pioneered data-driven models. By 2015, online lending had entered the mainstream. The 2020 pandemic accelerated digital adoption further. By 2026, the global alternative lending market has reached $556.45 billion, growing at 13.8% CAGR, with projections to hit $924.34 billion by 2030. The revenue-based financing segment alone is projected to reach $84.2 billion by 2035 at 16.4% CAGR.

✅ Advantages vs. ❌ Disadvantages

Alternative Lending: Advantages vs. Disadvantages

✅ Advantages

❌ Disadvantages

Faster approval (24 hours vs. 4 to 8 weeks)

Higher cost (15 to 99%+ APR vs. 5 to 12% bank)

Lower eligibility (500+ credit vs. 680+)

Shorter repayment terms

Less documentation required

Potential for predatory actors, especially MCAs

No collateral for many products

Less regulatory protection than bank loans

Flexible repayment structures

Daily/weekly repayment can strain cash flow

By the end of this guide, you'll understand every loan type available, see actual cost comparisons with worked dollar amounts, know which lenders match your business stage and industry, and understand the regulatory protections and gaps that affect borrowers in 2026.

Q2. How Do Alternative Lenders Compare to Traditional Banks? [toc=Alternative Lenders vs Banks]

Both traditional banks and alternative lenders serve legitimate needs, but they serve fundamentally different borrower profiles at different business moments. The comparison below maps the ten dimensions that matter most when deciding between the two paths.

💰 Side-by-Side Comparison

Traditional Bank vs. Alternative Lender Comparison

Dimension

Traditional Bank Loan

Alternative Lender

⏰ Approval speed

4 to 8 weeks

1 to 7 days

Min. credit score

680+

500 to 600

Min. time in business

2+ years

6 months

Annual revenue requirement

$250K+

$50K to $100K

Collateral

Usually required

Often unsecured

APR range

5 to 12%

15 to 99%+

Personal guarantee

Yes

Varies by product

Loan amounts

$50K to $5M

$5K to $500K

Application process

In-person paperwork

Online, 15 minutes

Regulatory protection

Full TILA/federal oversight

Partial; varies by product

Repayment structure

Monthly

Daily/weekly/monthly

✅ When Alternative Lenders Make More Sense

Alternative lenders are the stronger choice when:

Your business is under 2 years old, and banks won't consider you

Your credit score sits below 680, but revenue is healthy

You need funds in days, not weeks, because urgency matters (scaling a proven campaign, time-sensitive inventory)

Revenue is seasonal or project-based and doesn't fit rigid bank underwriting models

The loan amount is under $100K, where bank overhead makes them uninterested in serving you

As one r/smallbusiness commenter shared:

"SBA loans are a good alternative to traditional bank loans and have great rates and terms. However, these do require quite a bit of documentation and time." r/smallbusiness Reddit Thread

🏦 When Traditional Banks Are Still the Better Choice

Traditional bank loans remain the smarter path when your business has 3+ years of history, credit above 700, no urgency on timing, and you need larger amounts ($500K+) at the lowest possible cost. SBA-backed loans with government-guaranteed terms represent the gold standard for qualifying businesses. The guideline is simple: if you qualify for a bank loan and can wait for it, the lower cost almost always makes it the right choice. Alternative lenders serve the businesses, and the situations, that banks won't or can't.

Q3. What Types of Alternative Business Financing Are Available? [toc=Types of Alternative Financing]

The alternative lending landscape spans far beyond a single loan type. Understanding the full taxonomy helps you match the right product to your specific cash flow need, risk tolerance, and business model.

💰 Mainstream Debt Products

Online term loans: Fixed lump sum, 3 to 24 month terms, daily/weekly repayment. APR ranges from 27 to 99% depending on lender and risk profile. Best for one-time investments like inventory or equipment. Providers: Luca AI, OnDeck, Fora Financial.

Business lines of credit: Revolving access; draw as needed, pay interest only on what you use. APR 10 to 35%+. Best for managing cash flow gaps and seasonal variability. Providers: Bluevine, Fundbox.

Equipment financing: Asset-backed (the equipment itself is collateral). APR 5 to 30%, terms match the equipment's lifespan. Best for purchasing machinery, vehicles, or technology. Providers: Taycor Financial, National Funding.

📊 Specialized Debt Products

Invoice factoring: Sell unpaid invoices to a factor at 70 to 90% advance rate. The factor collects payment directly. Fee: 1 to 5% per month. Best for B2B businesses with long payment cycles.

Invoice financing: Use invoices as collateral for a loan while retaining collection responsibility. Key difference: factoring transfers collection risk; financing does not.

Revenue-based financing (RBF): Repayment flexes as a percentage of monthly revenue (typically 1 to 25%) until a 1.2 to 1.8x multiple is repaid. No equity dilution, no personal guarantees. Especially strong for e-commerce and DTC brands. Providers: Luca AI (dynamic real-time pricing, instant deployment), Wayflyer, Clearco, Uncapped.

Bridge loans: 3 to 12 month terms designed to cover temporary gaps; higher rates reflect the short duration.

⚠️ High-Risk Products

Merchant cash advances (MCAs): An advance against future credit/debit card sales, repaid via daily percentage holdback (typically 10 to 20% of daily sales). Factor rates of 1.1 to 1.5 translate to effective APR of 40 to 350%. MCAs are technically a purchase of future receivables, not loans, and they fall outside most lending regulations, including usury caps. As one Reddit user warned:

"I got from MCA to MCA to 'restructure' the debt... I've probably borrowed over $300K total over the years." r/smallbusiness Reddit Thread

🌱 Non-Debt Alternatives

Crowdfunding: Donation-based (GoFundMe), reward-based (Kickstarter), equity-based (Republic, Wefunder), and debt-based (Kiva). Best for consumer products and pre-revenue validation.

Grants: SBA grants, state/local programs, and minority/women-owned business grants. Free capital, but highly competitive and restricted in use.

Angel investors and venture capital: Equity financing exchanging ownership for growth capital. Best for high-growth startups, not for founders wanting full ownership.

Personal loans for business: Using personal credit for business expenses. Risky (personal liability) but sometimes the only early-stage option.

CDFIs and SBA microloans: Community Development Financial Institutions provide mission-driven lending to underserved businesses. SBA microloans (up to $50K) offer below-market rates through nonprofit intermediaries.

P2P lending: Platforms like Prosper connect individual investors with borrowers at 6 to 36% APR.

Bootstrapping and ROBS: Self-funding via reinvested revenue or Rollover for Business Startups (using retirement funds).

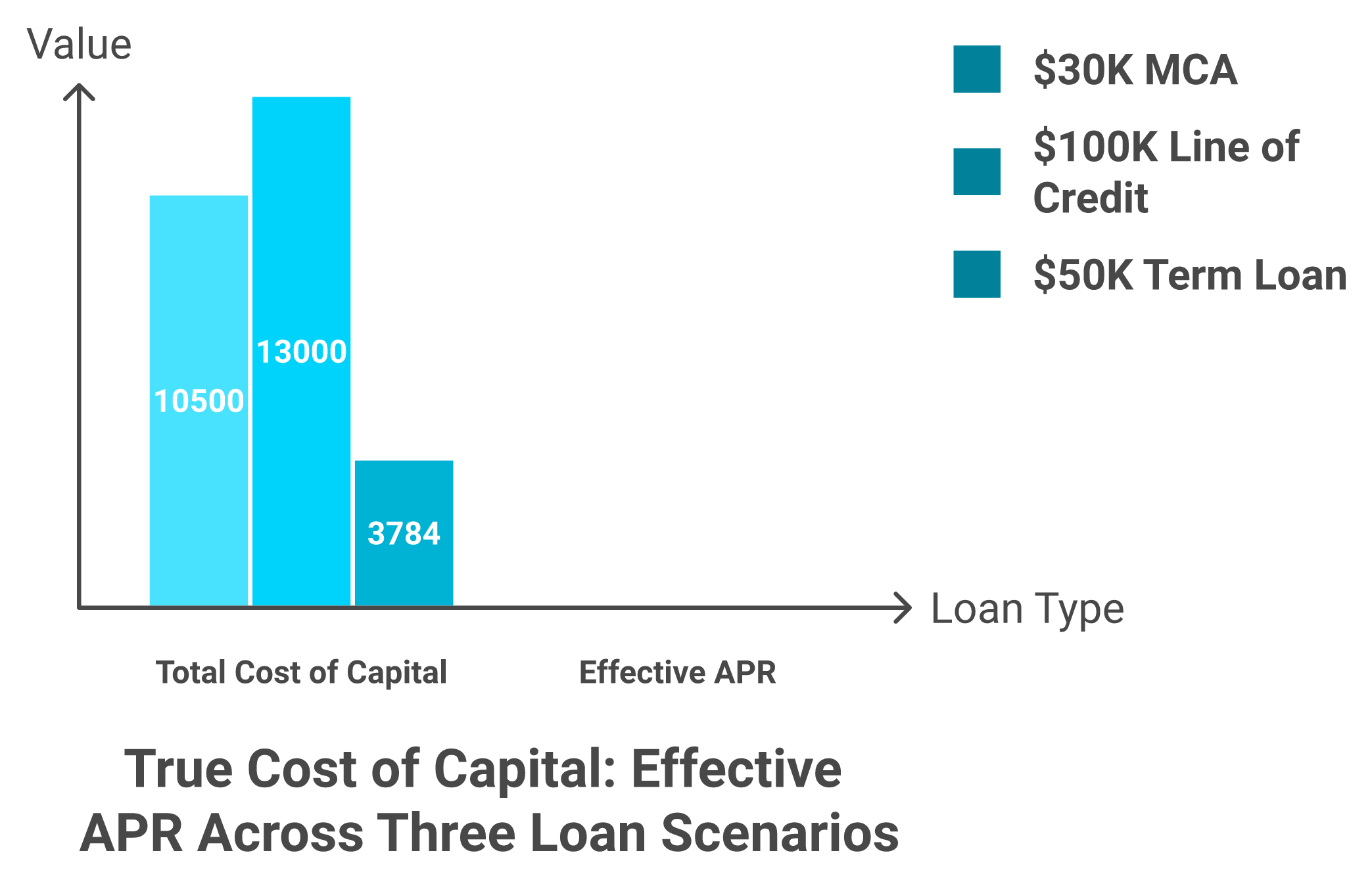

Q4. What Do Alternative Business Loans Actually Cost? (Worked Examples) [toc=Actual Loan Costs]

The single biggest problem borrowers face isn't finding capital; it's understanding what that capital truly costs. Alternative lenders use different pricing models, including APR, factor rates, flat fees, and revenue-share multiples, making apples-to-apples comparison nearly impossible.

💸 The Pricing Confusion Problem

A 1.3 factor rate sounds low but translates to 60 to 80%+ effective APR depending on repayment speed. A 6% flat fee on a 4-month advance equals 36%+ APR when properly annualized. The industry has an opacity problem, and borrowers who don't convert everything to APR equivalents consistently overpay. OnDeck, for example, lists a starting APR of 35.26% for term loans, but average rates run closer to 57.90%.

📊 Three Real-Cost Scenarios

Alternative Loan Cost Comparison: Three Scenarios

Metric

$50K Term Loan

$100K Line of Credit

$30K MCA

Pricing structure

18% APR

20% APR

1.35 factor rate

Term

18 months

12-month draw

~8 months

Repayment frequency

Monthly ($2,988)

Interest on avg. balance

Daily holdback

Total repaid

$53,784

~$113,000

$40,500

💰 Total cost of capital

$3,784

~$13,000

$10,500

Effective APR

18%

~20%

~80%

The MCA costs nearly 3x more than the term loan for a smaller advance. This is why converting every offer to effective APR and total repayment is non-negotiable.

When converted to effective APR, a $30K MCA at 1.35 factor rate costs nearly 3x more than a $50K term loan at 18% APR.

⚠️ Hidden Fees to Watch

Origination fees (1 to 5%): Deducted from disbursement; you receive less than the stated amount. OnDeck charges 0 to 4% origination.

Prepayment penalties: Some lenders penalize early payoff, trapping you in high-cost financing.

Maintenance/servicing fees: Monthly account charges that add up.

UCC filing fees: Administrative costs for lien filings.

NSF fees: If auto-debit fails due to insufficient funds.

Always demand a complete amortization schedule showing every payment and fee before signing.

⏰ Repayment Structures and Funding Speed

Repayment Frequency and Funding Speed by Product Type

Product Type

Repayment Frequency

Typical Funding Speed

MCAs / Platform capital

Daily

Same-day to 48 hours

Online term loans

Daily/weekly

1 to 5 days

Lines of credit

Monthly (draws: same-day)

1 to 3 days initial

Equipment financing

Monthly

3 to 10 days

SBA microloans

Monthly

2 to 4 weeks

Credit bureau reporting: Not all alternative lenders report to business credit bureaus. Ask before signing if building business credit is a priority.

✅ Cost of Capital vs. Cost of Inaction

A 25% effective APR sounds expensive in isolation, but context changes everything. A $50K advance at 20% APR that funds an inventory purchase with 60% margins or a campaign returning 4x ROAS generates $150K+ in gross profit against $5K in financing cost. As one r/smallbusiness thread framed it when debating a $150K RBF offer at 1.35x cap: the question isn't "is this expensive?" but rather "can I deploy this capital profitably?" Borrowers who understand their unit economics make fundamentally better capital decisions than those who fixate on rate alone.

Q5. Top Alternative Lenders Compared and Ranked for 2026 [toc=Top Lenders Ranked]

Choosing between alternative lenders requires more than reading marketing pages. The table below ranks 14 providers across the dimensions that matter most: maximum funding, credit requirements, revenue thresholds, minimum operating history, funding speed, and ideal borrower profile.

💰 Master Comparison Table

Top 14 Alternative Lenders Compared for 2026

#

Lender

Max Funding

Min. Credit

Min. Revenue

Min. Time in Business

Funding Speed

Best For

1

Luca AI

€500K

550+

€100K/yr

6 months

Instant / same-day

E-commerce and DTC brands needing dynamically-priced capital

2

OnDeck

$250K

625

$100K/yr

1 year

1 to 3 days

Established businesses needing fast term loans

3

Bluevine

$250K LOC

625

$10K/mo

2 years

Same-day draws

Revolving line of credit with flexible draws

4

Fundbox

$150K

600

$100K/yr

6 months

Next business day

Startups needing quick LOC

5

Fora Financial

$1.5M

500

$240K/yr

6 months

72 hours

Bad-credit borrowers needing larger amounts

6

National Funding

$500K

600

$250K/yr

6 months

24 hours

Equipment financing + term loans

7

Kapitus

$5M

625

$250K/yr

2 years

2 to 5 days

Larger established businesses

8

Taycor Financial

$2M

550

Varies

1 year

3 to 7 days

Equipment financing specialists

9

Credibly

$600K

500

$180K/yr

6 months

1 to 3 days

Businesses with poor credit

10

Accion Opportunity Fund

$250K

No min

$50K/yr

Varies

1 to 2 weeks

Underserved communities / CDFIs

11

Rapid Finance

$1M

550

$120K/yr

6 months

24 hours

Fast MCA + working capital

12

iBusiness Funding

$500K

600

$150K/yr

1 year

2 to 3 days

Multiple product types via single application

13

Reliant Funding

$400K

500

$100K/yr

6 months

Same-day

High-risk / bad-credit MCA

14

Prosper

$50K

640

Varies

N/A

3 to 5 days

P2P personal loans for business use

⭐ #1 Luca AI: Purpose-Built for E-commerce

Luca AI competes on capital metrics that traditional RBF providers can't match. ✅ Dynamic pricing adjusts rates with each advance based on real-time business health: take €50K in March at one price, then €50K in April at a cheaper price as performance improves. ✅ Frequent small advances (€10K to €50K) ensure capital never sits idle, lowering total cost over 12 months compared to one large lump sum. ✅ One-click deployment: no application paperwork, no negotiation. Capital is unlocked by performance, not applied for. ✅ No personal guarantee, no equity dilution, and revenue-responsive repayment.

Contrast this with the pattern borrowers report from traditional RBF providers:

"After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute." Geoff Brand Wayflyer - Trustpilot Verified Review

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly." Thomas Bishop Clearco - Trustpilot Verified Review

📊 Lenders #2 to #7 Profiles

OnDeck: One of the largest online term loan providers; APR 35.26% to 97.3%, weekly/daily repayment, and reports to credit bureaus.

Bluevine: Top-rated for revolving LOC; same-day draws after approval, APR 14% to 95%, and 625+ credit minimum.

Fundbox: Strong for newer businesses; AI-driven underwriting and 6-month operating minimum.

Fora Financial: Accepts scores as low as 500, up to $1.5M, but higher cost reflects higher risk.

National Funding: Equipment financing + working capital; 24-hour funding.

Kapitus: Up to $5M for established businesses; requires 2+ years history.

📊 Lenders #8 to #14 Profiles

Taycor Financial: Equipment financing specialist; terms match asset lifespan.

Credibly: MCA and working capital for underserved credit tiers.

Accion Opportunity Fund: CDFI lender, no minimum credit, and ideal for minority-owned and women-owned businesses.

Rapid Finance: Same-day MCA + working capital for urgent needs.

iBusiness Funding: Term loan, LOC, and MCA through one application.

Prosper: P2P platform for personal loans usable for business; up to $50K.

Q6. Which Loan Type Fits Your Business Stage? (Decision Framework) [toc=Loan Type by Stage]

Not every alternative lending product fits every business. The stage of your company, from pre-revenue idea to established enterprise, determines which products you qualify for, which make financial sense, and which create unnecessary risk.

Your business stage determines which alternative lending products you qualify for and which create unnecessary risk.

🌱 Pre-Revenue / Idea Stage (0 to 6 Months)

Options are limited but real. Grants (SBA, state/local, and minority/women-owned programs) provide free capital with no repayment obligation. Crowdfunding (Kickstarter, Indiegogo) validates demand while raising funds. SBA microloans via CDFIs offer up to $50K at below-market rates. Personal loans or ROBS (Rollover for Business Startups) strategies carry personal liability risk and are best treated as last resorts.

Mini case study: A founder launching a DTC skincare brand secures a Kiva microloan ($15K, 0% interest) for initial inventory and runs a Kickstarter campaign ($30K in pre-orders) to validate product-market fit, all before seeking external capital.

⏰ Early-Stage (6 to 24 Months)

The business has revenue but limited operating history. Best options include online lines of credit (Fundbox, Bluevine with a 6-month minimum), some online term loans (Fora Financial accepts 500+ credit), and revenue-based financing for e-commerce brands meeting minimum thresholds. Luca AI requires just €100K annual revenue and 6 months operating history, with no application process and capital unlocked by performance. MCAs should only be considered if daily card volume is high and no other option exists.

Key eligibility profile: 500 to 600 credit, $50K to $100K annual revenue, and 6+ months operating.

💰 Growth Stage (2 to 5 Years)

This is the sweet spot for alternative lending: enough history for favorable terms, but often still underserved by traditional banks. Online term loans (OnDeck, National Funding), larger LOCs (Bluevine up to $250K), RBF for e-commerce (Luca AI with dynamic pricing that rewards improving business health with progressively lower rates), equipment financing (Taycor, National Funding), and invoice factoring for B2B businesses all become accessible.

At this stage, compare at least three lender offers and calculate total cost, not just the sticker rate.

🏦 Established Business (5+ Years)

The full range of options is available. Pursue bank loans or SBA 7(a) financing (up to $5M, competitive rates) for large, long-term needs. Use alternative lenders only for speed-sensitive opportunities or to complement bank credit lines. Kapitus serves this tier with up to $5M in funding.

✅ The Graduation Strategy

Alternative lending should not be permanent. The trajectory: start with accessible products (microloans, small LOCs), build business credit and revenue track record, graduate to online term loans and RBF at better rates, and eventually qualify for SBA or bank financing at 5 to 12% APR. Each stage of responsible borrowing builds the credit history that unlocks cheaper capital next time. Key actions: ensure your lender reports to credit bureaus, maintain clean repayment history, and periodically re-apply to banks to test eligibility.

Q7. What Industry-Specific and Underserved-Community Lending Options Exist? [toc=Industry-Specific Lending]

The best alternative lending choice depends not just on your business stage but on your industry. Revenue patterns, cash flow cycles, and capital needs vary dramatically between a DTC e-commerce brand, a restaurant, and a construction company.

🛒 E-commerce and DTC Brands

E-commerce businesses face a unique capital timing problem: inventory cycles demand upfront capital 60 to 90 days before revenue materializes, marketing spend requires rapid scaling when campaigns prove profitable, and Q4 seasonal peaks create severe cash flow crunches. Revenue-based financing is the natural fit because repayment flexes with revenue, making it perfect for seasonal businesses.

Top providers ranked: Luca AI (#1: dynamic pricing drops as performance improves, instant one-click deployment, frequent small advances of €10K to €500K keep total cost below competitors who push one large lump sum, and no personal guarantee), Wayflyer, Clearco, Uncapped, 8fig, and Onramp Funds.

However, borrowers should vet carefully. As one 8fig user reported:

"They sucker you in by saying how they will scale you big and then since you're hooked legally now, they create a disbursement and payment plan that gets extremely confusing to follow in a dashboard and you end up using the prior disbursement to cover the next, like one of those high interest payday advances." Suckered In 8fig - Trustpilot Verified Review

📱 Platform-Embedded Capital

The first alternative funding many e-commerce founders encounter: Shopify Capital (MCA or term loan based on Shopify sales, invitation-only, daily repayment at 10 to 17% of sales), Amazon Lending (invitation-only, marketplace performance-based), PayPal Working Capital (based on PayPal sales history, no credit check), and Stripe Capital (for Stripe payment processors). These are convenient but limited: you can only access what the platform offers, with no negotiation on terms.

As one Reddit user shared:

"My business experienced an 80% year-over-year growth from 2023 to 2024, which would have been unattainable without that capital. At that time, I couldn't secure an SBA loan due to being under two years in operation." r/shopify Reddit Thread

🏥 Other Key Verticals

Restaurants/food service: Equipment financing for kitchen buildouts, MCAs for high daily card volume, and SBA microloans for startup costs. Revenue-responsive repayment is critical given inherent weekly variability.

Healthcare/medical: Medical equipment financing, practice acquisition loans, and AR financing against insurance reimbursements.

SaaS: RBF aligns naturally with recurring revenue; providers like Pipe and Capchase serve this vertical.

Construction: Equipment leasing, invoice factoring against progress billing, and LOCs for bridging between project payments.

🤝 CDFIs and Underserved-Community Programs

Community Development Financial Institutions provide mission-driven lending with lower rates and more flexible underwriting than any commercial alternative lender. The SBA 8(a) Business Development Program supports small disadvantaged businesses. Accion Opportunity Fund targets minority-owned, women-owned, veteran-owned, and rural businesses with no minimum credit score.

⚠️ The Universal Matching Principle

Match repayment structure to revenue pattern. Daily card sales businesses work well with daily holdback products. Lumpy project-based revenue (construction, agencies) demands monthly repayment. Subscription/recurring revenue (SaaS) aligns perfectly with RBF. Mismatched repayment structures are the #1 cause of alternative lending distress.

Q8. How Do You Evaluate, Apply for, and Get Approved for an Alternative Business Loan? [toc=Evaluate and Apply]

Finding capital is step one. Evaluating it correctly, applying strategically, and maximizing your approval odds is where most borrowers either save or waste thousands of dollars.

📊 The 8 Dimensions That Matter

Before accepting any offer, compare across these dimensions:

Effective APR: Convert all pricing (factor rates, flat fees, and revenue-share multiples) to annualized APR.

Total repayment amount: The only number that tells the true cost.

Fees: Origination (1 to 5%), maintenance, prepayment penalties, and UCC filing.

Repayment structure: Daily, weekly, or monthly, and flexibility if revenue dips.

Funding speed: Same-day to 4 weeks depending on product type.

Credit bureau reporting: Does the lender report to Dun & Bradstreet, Experian Business, or Equifax Business?

Customer support: Responsiveness after you've signed matters more than during sales.

Contract terms: UCC lien scope (blanket vs. specific), confession-of-judgment clauses, and default triggers.

Always get at least 3 offers before committing.

⏰ Step-by-Step Application Process

Define your need: Use case, amount, urgency, and repayment capacity.

Check eligibility: Personal + business credit scores, time in business, and revenue.

Gather documentation (see below).

Apply to 3 to 5 lenders simultaneously: Applications are typically soft pulls that won't affect your credit.

Compare all offers using effective APR and total repayment.

Read the full contract: Not just the summary sheet.

Accept and receive funds.

📋 Documents Typically Required

Business bank statements (3 to 6 months)

Tax returns (1 to 2 years, if available)

Profit & loss statement and balance sheet

Business license / registration documents

Personal identification

Voided business check

Platform connections (Shopify, Stripe, and bank account via Plaid)

Having documents organized before applying accelerates approval and signals a serious borrower.

✅ How to Improve Approval Chances

Improve cash flow consistency: Lenders want steady deposits, not lumpy revenue with gaps.

Reduce existing debt: Debt-to-income ratio matters across all lender types.

Build business credit: Pay suppliers on terms, use a business credit card, and ensure lenders report to bureaus.

Clean up personal credit: Pay down balances and correct reporting errors.

Separate business and personal finances: A dedicated business bank account is essential.

Apply for the right product: Don't apply for a $500K term loan from a lender whose sweet spot is $50K LOCs.

❌ Common Denial Reasons and Fixes

Common Denial Reasons and How to Fix Them

Denial Reason

Fix

Insufficient time in business

Apply to lenders with 6-month minimums (Fundbox, Fora Financial) or seek CDFIs.

Low credit score

Target lenders accepting 500+ (Credibly, Reliant Funding) or choose MCAs.

Insufficient revenue

Grow to minimums before reapplying, or seek smaller amounts.

Negative bank activity (overdrafts, NSF)

Clean up 3 months of bank statements before applying.

Existing debt load too high

Pay down or consolidate existing obligations first.

Industry exclusion

Some lenders exclude cannabis, firearms, and adult industries. Check before applying.

Q9. What Are the Predatory Lending Red Flags, Stacking Risks, and Responsible Borrowing Practices? [toc=Predatory Lending Red Flags]

The alternative lending market includes legitimate providers and bad actors. Knowing the difference before you sign can protect your business from contracts designed to extract maximum value rather than support growth.

⚠️ Red Flags That Should Stop You Immediately

If you encounter any of these, walk away:

"Guaranteed approval" with no credit or revenue check: legitimate lenders always assess risk.

Pressure to take a larger amount than you requested: upselling maximizes lender fees, not your ROI.

Refusal to disclose APR or total repayment amount in writing before signing.

Confession-of-judgment clauses: allowing the lender to seize assets without court process.

Blanket UCC liens on all business assets for a small advance.

Daily-changing terms or verbal promises that don't appear in the written contract.

Excessive urgency: "This offer expires today" is a pressure tactic, not a business practice.

❌ What Real Borrowers Report

Patterns from verified industry reviews reveal systemic issues across traditional RBF providers. Wayflyer borrowers report approved funding reversed at the last minute after critical business decisions were already made, and contract terms that contradict what was communicated during sales:

"Read their terms and contract carefully! They said their offer is not secured, which is false: they still will file UCC. They can deem you in default for any reason at their discretion. The worst bank agreement I have read in 25 years." Zachary Piech Wayflyer - Trustpilot Verified Review

Clearco borrowers report repayments pulled faster than contractually agreed, effectively increasing the interest rate, followed by non-existent customer support:

"They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly, and then could never resolve these issues. A year later we get hit up by a collections agent with zero communications." Thomas Bishop Clearco - Trustpilot Verified Review

Uncapped borrowers describe classic bait-and-switch patterns where signed funding amounts are slashed without warning:

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M. Then months later they cut it again to $350K." Xin Shui, CEO/Founder Uncapped - Trustpilot Verified Review

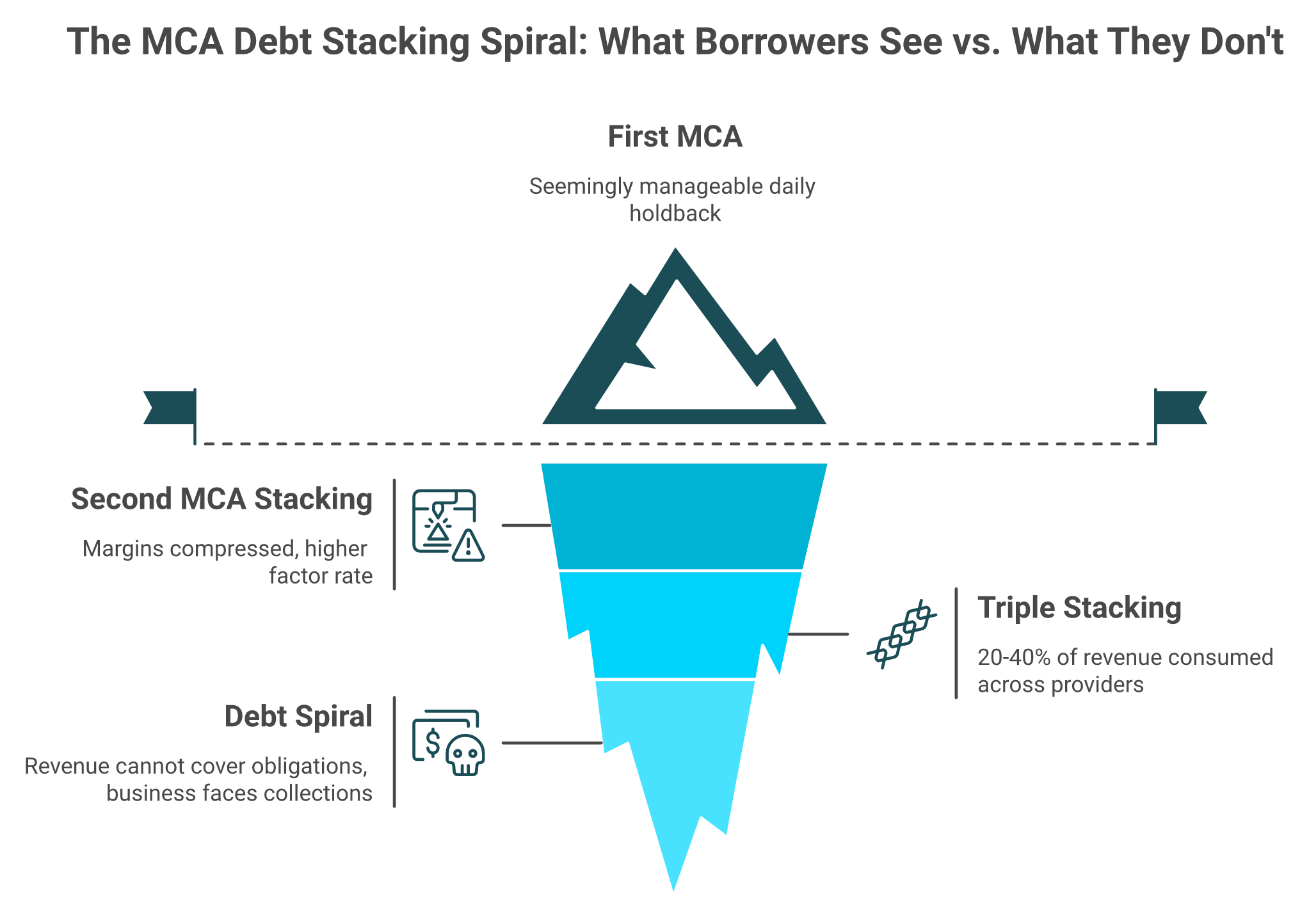

💸 Debt Stacking: The Silent Killer

A business takes an MCA. When daily holdbacks compress margins, a second MCA is taken from a different provider. Then a third. Each new advance carries a higher factor rate because the lender sees existing obligations. The borrower is now repaying 20 to 40% of daily revenue across multiple providers simultaneously, creating a debt spiral that can become unrecoverable.

The real danger of MCA stacking lies beneath the surface: each additional advance deepens the spiral toward 200%+ effective APR.

As one Reddit user warned:

"By taking multiple advances, you often end up in a 200%+ APR cycle. If you're caught in this, break the cycle." r/Businessloans Reddit Thread

✅ Responsible Borrowing Framework

Never borrow more than you have a specific, profitable use case for.

Calculate breakeven: if incremental profit doesn't cover the cost, don't take it.

Limit total debt service to under 15% of monthly revenue.

Never take a second advance to cover repayment of the first.

Read the full contract, not just the summary sheet.

Keep a cash reserve equal to 2 months of repayment obligations.

⏰ Already in Trouble?

Contact your lender immediately; many will restructure before escalating. Explore consolidation products from lenders like Kapitus or National Funding. File complaints with your state Attorney General's office if terms were misrepresented. Consult a free Small Business Development Center (SBDC) advisor. If stacking is severe, a small business attorney can evaluate contracts for unenforceable clauses.

Q10. What Regulatory Safeguards Protect Alternative Lending Borrowers in 2026? [toc=Regulatory Safeguards]

The regulatory landscape for alternative lending is evolving rapidly, but significant gaps remain, particularly for merchant cash advances. Understanding what protects you (and what doesn't) is essential before signing any agreement.

⚠️ The Regulatory Gap Problem

Traditional bank loans fall under the Truth in Lending Act (TILA), Equal Credit Opportunity Act (ECOA), and extensive federal/state banking regulations. Most alternative lending products fall under some of these frameworks. However, MCAs are a critical exception. Because MCAs are structured as "purchases of future receivables" rather than loans, they bypass usury laws, TILA disclosure requirements, and most state lending regulations. An MCA provider can charge the equivalent of 200%+ APR with no legal obligation to disclose that rate.

This gap is the single biggest regulatory risk borrowers face in 2026.

📋 CFPB Section 1071: The Biggest Development of 2026

This rule implements Section 1071 of the Dodd-Frank Act, requiring covered financial institutions to collect and report data on small business lending applications, including demographics of applicants, loan terms, and approval/denial rates.

Key implementation timeline:

CFPB Section 1071 Compliance Timeline

Compliance Tier

New Compliance Date

First Filing Deadline

Tier 1 (highest volume)

July 1, 2026

June 1, 2027

Tier 2 (moderate volume)

January 1, 2027

June 1, 2028

Tier 3 (smallest volume)

October 1, 2027

June 1, 2028

A November 2025 proposed revision would narrow coverage to mainstream business loans, lines of credit, and credit cards, explicitly excluding revenue-based financing and agricultural lending. This means RBF and MCA users won't benefit directly from this data collection.

🏛️ State-Level Protections (The Patchwork)

California (SB 1235): Requires commercial financing providers to disclose total repayment amount, APR equivalent, and prepayment policies.

New York: Mandates similar disclosures for commercial financing including MCAs; banned confession-of-judgment clauses for out-of-state borrowers.

Virginia and Utah: Enacted APR disclosure requirements.

However, the majority of states still have no commercial lending or MCA disclosure requirements. Borrowers in unregulated states must self-protect by demanding disclosure documents voluntarily.

⭐ SMART Box: The Voluntary Trust Signal

The Innovative Lending Platform Association (ILPA) developed the SMART Box (Straightforward Metrics Around Rate and Total Cost), a standardized disclosure providing APR equivalent, total cost of capital, total repayment amount, average monthly payment, and cents-on-the-dollar cost. Several reputable lenders (OnDeck, Fundbox, and Funding Circle) voluntarily adopt it. If a lender offers SMART Box, it signals transparency. If they refuse when asked, treat it as a warning sign.

State Attorney General's office: especially in states with disclosure laws.

Federal Trade Commission (FTC): deceptive business practices.

Better Business Bureau (BBB): file complaints and check lender history before applying.

State banking regulator: if the lender holds a state lending license.

Document everything: save all emails, contracts, payment records, and communications.

Q11. What 2026 Trends Are Reshaping Alternative Lending for Small Businesses? [toc=2026 Lending Trends]

The alternative lending industry is undergoing a structural transformation driven by AI-powered underwriting, embedded finance, open banking APIs, and regulatory evolution. These trends directly impact pricing, accessibility, and speed for borrowers.

🤖 AI/ML-Powered Underwriting and Dynamic Pricing

Traditional credit scoring (FICO-centric) is being replaced by machine learning models that analyze hundreds of data points: bank transaction patterns, commerce platform metrics, marketing efficiency ratios, cash flow consistency, and even customer review sentiment. This means broader access for businesses with thin credit files but strong revenue, faster decisions measured in minutes rather than days, and the emergence of dynamic pricing where rates adjust in real time based on evolving business health rather than a static application snapshot.

Borrowers who maintain healthy, transparent data across connected platforms will increasingly receive better rates than those who don't. ✅ Luca AI exemplifies this shift: we price each advance dynamically based on real-time business performance, meaning rates improve as the business improves, rather than locking borrowers into pricing based on a 90-day-old snapshot.

💰 Embedded Lending and B2B BNPL

Lending is being embedded directly into platforms businesses already use. Shopify Capital, Stripe Capital, Amazon Lending, and Square Loans represent the first wave, but 2026 is seeing embedded credit expanding into accounting software (Xero, QuickBooks), inventory management systems, and B2B marketplaces. B2B buy-now-pay-later (BNPL) allows businesses to pay suppliers on extended 30/60/90-day terms with a financing provider covering the upfront cost.

Open banking via APIs like Plaid is the infrastructure making this possible. Lenders access real-time bank data with borrower permission, eliminating manual statement uploads and enabling continuous underwriting rather than point-in-time snapshots.

🔗 Blockchain Lending and Regulatory Evolution

Decentralized lending platforms (Aave, Compound, and Goldfinch) are exploring real-world asset lending, still nascent for small business but growing. Smart contracts could automate loan origination, disbursement, and repayment without intermediaries. On the regulatory front, beyond CFPB Section 1071's Tier 1 compliance beginning July 1, 2026, expect continued state-level expansion of APR disclosure requirements, potential federal legislation addressing MCA regulation specifically, and greater scrutiny of AI-driven underwriting for bias and fairness.

The direction is clear: more transparency, more disclosure, and more borrower protection, but implementation remains slow and uneven across jurisdictions. ❌ Traditional RBF providers relying on static underwriting and opaque pricing will face increasing pressure to modernize or lose borrowers to intelligence-led platforms that price dynamically and transparently.

Q12. Alternative Lenders FAQ: Quick Answers to the Most Common Questions [toc=Alternative Lenders FAQ]

Q: Are alternative lenders safe?

⭐ Reputable alternative lenders (OnDeck, Bluevine, Fundbox, and Luca AI) are legitimate and regulated. However, the industry includes predatory actors, especially in the MCA space. Always verify credentials via BBB, check Trustpilot reviews, and demand full cost disclosure (APR, total repayment, and all fees) before signing any agreement.

Q: How fast can I get funded through an alternative lender?

⏰ Most online lenders fund within 1 to 7 business days. MCAs and platform capital (Shopify Capital, PayPal Working Capital) can fund same-day. Revenue-based financing providers like Luca AI offer instant one-click deployment. Bank loans typically take 4 to 8 weeks by comparison.

Q: Can I get an alternative business loan with bad credit?

✅ Yes. MCAs typically have no minimum credit score. Some online term loans (Fora Financial, Credibly) accept scores as low as 500. Revenue-based financing evaluates business performance over personal credit. CDFIs like Accion Opportunity Fund have no minimum credit requirement. Lower credit always means higher cost, but access exists.

Q: What is the difference between a merchant cash advance and a loan?

💰 An MCA is technically a purchase of future receivables, not a loan. This means it's not subject to usury laws or many lending regulations. Repayment is a fixed percentage of daily credit/debit card sales. APR disclosures are not always legally required. Always ask for the total repayment amount and calculate the effective APR yourself before signing.

Q: Do alternative lenders require collateral?

Most online term loans and lines of credit are unsecured but may require a personal guarantee and/or UCC lien filing. Equipment financing uses the equipment itself as collateral. MCAs and RBF are typically unsecured but often involve blanket UCC liens on business assets. Always ask what assets the lien covers.

Q: Can I use alternative lending to build business credit?

Only if the lender reports to business credit bureaus (Dun & Bradstreet, Experian Business, and Equifax Business). Not all alternative lenders do. Confirm before signing. Building credit is a valuable side benefit of responsible borrowing that unlocks cheaper capital over time.

Q: What happens if I can't make repayments?

⚠️ Contact your lender immediately. Many will restructure terms before escalating to collections or legal action. For MCAs, review your contract for reconciliation rights that may allow payment adjustment. If stacking has created unmanageable obligations, consult an SBDC advisor (free) or a small business attorney to evaluate your options.

Q: How is Luca AI different from other alternative lenders?

✅ Luca AI is purpose-built for e-commerce and DTC brands. Unlike traditional RBF providers that price off static 90-day snapshots, Luca dynamically adjusts capital pricing based on real-time business health, meaning rates drop as performance improves. Capital is deployed instantly via one-click with no application process, no personal guarantee, and revenue-responsive repayment. Frequent small advances (€10K to €50K) keep total cost lower than competitors who push one large lump sum.

FAQ's

What is the cheapest type of alternative business loan for e-commerce brands?

We find that the cheapest alternative financing option for e-commerce brands is typically revenue-based financing (RBF) from providers that use dynamic pricing models. Unlike static-rate term loans or merchant cash advances, RBF aligns repayment with your actual revenue, and the best providers adjust pricing based on real-time business health.

For example, Luca AI prices each advance dynamically, meaning your rate drops as your business performance improves. Frequent small advances of 10K to 50K euros keep total cost lower than one large lump sum from competitors.

Here is how the cost spectrum typically breaks down:

RBF (dynamic pricing): Lowest effective cost when performance is strong

Online term loans: 27 to 99% APR depending on lender and risk profile

Business lines of credit: 10 to 35%+ APR, interest only on drawn amounts

MCAs: 40 to 350% effective APR, the most expensive option

We always recommend converting every offer to effective APR and total repayment before signing. A 1.3 factor rate may sound low, but it translates to 60 to 80%+ effective APR. Understanding your unit economics is the only way to determine whether a financing cost is justified by the return it generates.

Can I get an alternative business loan with less than one year in business?

Yes. Several alternative lenders specifically serve businesses with as little as six months of operating history. We cover this in detail because traditional banks typically require two or more years, which locks out most early-stage founders.

Here are the strongest options for businesses under one year old:

Fora Financial: Up to $1.5M, accepts credit scores as low as 500, 6-month minimum

Credibly: Up to $600K for businesses with poor credit and 6 months of history

Luca AI: Up to 500K euros for e-commerce brands with 100K euros annual revenue and 6 months operating, with instant capital deployment unlocked by performance

For businesses with zero revenue (pre-launch), grants, crowdfunding, SBA microloans via CDFIs, and personal loans remain the primary paths. We recommend starting with accessible products, building a clean repayment history, and graduating to better-rate products as your credit profile strengthens. The key is ensuring your lender reports to business credit bureaus so each stage of borrowing unlocks cheaper capital next time.

How do alternative lenders differ from traditional bank loans for small businesses?

We break this comparison across ten dimensions that matter most. The core architectural difference is that alternative lenders use AI and ML-driven credit scoring, real-time bank transaction analysis via open banking APIs, and commerce data from platforms like Shopify and Amazon, while traditional banks rely on manual reviews and FICO-centric decisioning.

Here are the key differences at a glance:

Approval speed: 1 to 7 days (alternative) vs. 4 to 8 weeks (bank)

Minimum credit: 500 to 600 (alternative) vs. 680+ (bank)

Collateral: Often unsecured (alternative) vs. usually required (bank)

APR range: 15 to 99%+ (alternative) vs. 5 to 12% (bank)

Application process: Online in 15 minutes (alternative) vs. in-person paperwork (bank)

The guideline we share is simple: if you qualify for a bank loan and can wait for it, the lower cost almost always makes it the right choice. Alternative lenders serve the businesses and situations that banks will not or cannot. For e-commerce brands with seasonal cash flow, alternative lenders often provide the only realistic path to timely capital.

What are the biggest risks of merchant cash advances and how do I avoid debt stacking?

We consider MCAs the highest-risk product in the alternative lending landscape. MCAs are technically a purchase of future receivables, not loans, which means they bypass usury laws, TILA disclosure requirements, and most state lending regulations. Factor rates of 1.1 to 1.5 translate to effective APR of 40 to 350%, and providers have no legal obligation to disclose that rate in many states.

The silent killer is debt stacking: taking a second or third MCA from different providers to cover repayment shortfalls from the first. Each new advance carries a higher factor rate, and borrowers can end up repaying 20 to 40% of daily revenue across multiple providers simultaneously.

Our responsible borrowing framework recommends:

Limit total debt service to under 15% of monthly revenue

Never take a second advance to cover repayment of the first

Always convert factor rates to effective APR before signing

Demand a complete amortization schedule showing every payment and fee

If you are already in trouble, contact your lender immediately about restructuring. You can also consult a free SBDC advisor or explore consolidation options. For e-commerce brands seeking a safer alternative, revenue-responsive financing with transparent pricing eliminates the stacking risk entirely.

What is revenue-based financing and why is it ideal for Shopify and DTC brands?

Revenue-based financing (RBF) is a non-dilutive funding model where repayment flexes as a percentage of monthly revenue, typically 1 to 25%, until a 1.2 to 1.8x multiple of the advance is repaid. There is no equity dilution, no fixed monthly payment, and often no personal guarantee. This makes RBF especially powerful for e-commerce and DTC brands with seasonal revenue patterns.

Here is why RBF fits the e-commerce model so well:

Inventory timing: Capital is needed 60 to 90 days before revenue materializes from inventory purchases

Marketing scaling: Profitable campaigns need rapid capital injection to scale before the window closes

Seasonal peaks: Q4 cash crunches require flexible funding that adjusts to actual sales volume

Among RBF providers, we built Luca AI to solve the specific limitations founders report with traditional RBF. Our dynamic pricing adjusts rates with each advance based on real-time business health, so a 50K euro advance in March may cost less than one taken the prior month if performance has improved. One-click deployment with no application paperwork means capital is unlocked by performance, not applied for.

Other providers in this space include Wayflyer, Clearco, Uncapped, and 8fig, though borrower reviews indicate inconsistencies in contract enforcement and funding reliability.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.svg)

.svg)

.svg)

.webp)

.avif)