7 Types of Inventory Financing Compared: Costs, Risks, and How to Choose the Right One

14

mins read

TL;DR

Seven distinct inventory financing types exist, each designed for a different stage of the inventory lifecycle and business profile. Costs range from 5% APR for revolving lines to 72% effective APR for PO financing, with hidden fees adding 3-8% annually. Choosing the wrong structure can waste thousands per restock cycle; match structure to purchase frequency, speed needs, and cost tolerance. AI-native capital platforms offer dynamically-priced advances with no collateral, continuous underwriting, and same-day deployment. Negotiate appraisal methods, prepayment penalties, and borrowing base formulas to reduce total cost of capital by 15-30%. Avoid inventory financing entirely if gross margins fall below 25% or turnover exceeds 90 days.

Q1: What Is Inventory Financing and How Does It Actually Work? [toc=What Is Inventory Financing]

Inventory financing is a category of asset-based lending where a business uses its existing or to-be-purchased inventory as collateral to secure working capital. Unlike unsecured loans that depend heavily on credit scores or years of business history, the physical goods themselves back the facility, meaning approval hinges more on inventory quality and turnover velocity than traditional creditworthiness metrics. E-commerce brands commonly use it for seasonal restocking, capturing bulk purchase discounts from suppliers, and bridging the cash conversion cycle gap, the costly window between paying manufacturers and collecting customer revenue.

⏰ From Application to Funding: How the Process Works

The end-to-end mechanics follow a structured six-step cycle:

Application - Submit inventory records, financial statements, and recent bank statements to the lender.

Appraisal - The lender orders an inventory valuation to determine liquidation value (not retail value).

Advance rate setting - The lender assigns an advance percentage, typically 50-80% of appraised value.

Capital disbursement - Funds are released as either a lump sum or a revolving credit facility.

Repayment - Scheduled interest-plus-principal payments proceed while the lender monitors inventory levels.

Lien release - Upon full repayment, the collateral lien is removed from your assets.

The full cycle takes anywhere from 1-6 weeks depending on lender type. Online and alternative inventory lenders typically fund within 24-72 hours, while traditional banks average 2-4 weeks with significantly heavier documentation requirements.

💰 How Lenders Actually Value Your Inventory

Lenders don't use your retail price to calculate the funding ceiling; they use liquidation value. Two primary valuation methods dominate the market:

Forced Liquidation Value (FLV): What your inventory would sell for in a fire-sale scenario, typically 30-50% of retail value.

Net Orderly Liquidation Value (NOLV): What it would fetch in a planned, orderly wind-down, typically 50-70% of retail value.

The distinction directly impacts how much capital you can access. NOLV-based appraisals yield 15-25% more funding than FLV-based ones, making it critical to confirm which valuation method your lender uses before proceeding with any application.

Advance Rates: What Determines Your Funding Amount

The advance rate, the percentage of appraised inventory value the lender will actually fund, varies significantly by product category:

Advance Rates by Inventory Type

Inventory Type

Typical Advance Rate

✅ Finished goods

60-80%

✅ Raw materials

40-60%

⚠️ Work-in-progress

30-50%

⚠️ Perishables

20-40%

Factors that increase your advance rate include high inventory turnover ratios, a diversified SKU base, non-perishable product categories, real-time inventory tracking systems (e.g., Shopify or NetSuite integration), and at least 6-12 months of established sales history. Most lenders require minimum annual revenue of $50,000-$100,000 for non-bank facilities.

Why E-commerce Brands Face a Structural Cash Flow Gap

DTC and e-commerce businesses face a unique working capital problem that makes inventory financing especially relevant. Suppliers typically demand payment 60-120 days before customer revenue materialises. Ad spend on platforms like Meta, Google, and TikTok is collected upfront. Marketplaces such as Amazon hold seller payouts for 14+ days. This creates a compounding cash vacuum where growth itself becomes the bottleneck; the faster you sell, the more capital you need to restock.

Inventory financing bridges this gap without diluting equity. It's particularly effective for covering short-term cash gaps, preparing for seasonal demand spikes, and capitalising on bulk purchase discounts. However, the specific structure you choose, whether term loan, revolving line, purchase order financing, or warehouse receipt lending, determines whether that capital strengthens or quietly erodes your unit economics.

Q2: What Are the 7 Types of Inventory Financing? [toc=7 Types of Inventory Financing]

Inventory financing is not a single product; it's a family of seven distinct structures, each designed for a different stage of the inventory lifecycle and business profile. The right choice depends on whether you already hold inventory or need to acquire it, whether your need is one-time or recurring, and how quickly capital must be deployed.

1. Inventory Term Loan

A fixed lump-sum loan secured against existing inventory. The lender appraises your goods, advances 50-80% of liquidation value, and sets a fixed monthly repayment schedule over 6-24 months.

💰 Typical APR: 7-25%

Best for: Large one-time purchases, e.g., pre-season Q4 inventory buys exceeding $100K

Real-world example: A DTC skincare brand borrows $100K to place a single holiday gift-set order with their contract manufacturer, repaying ~$9K/month over 12 months at 14% APR

❌ Drawback: Interest accrues on the full amount from day one, even if inventory sells ahead of schedule

2. Inventory Line of Credit

A revolving credit facility where you draw and repay against inventory collateral as needed, paying interest only on the drawn amount. Draw $30K this month, $70K next month, repay, and re-draw as sales dictate.

💰 Typical APR: 5-18%

Best for: Brands with variable monthly restocking needs and unpredictable bestsellers

✅ Advantage: Maximum flexibility and lowest effective cost when monthly utilisation varies significantly

3. Floor Plan Financing

Unit-level financing for high-value, serialised goods. The lender pays the manufacturer directly for specific units; you pay interest while goods sit in your warehouse or showroom, then repay principal when each individual unit sells.

💰 Typical APR: 5-15%

Best for: Electronics retailers, furniture dealers, automotive dealerships, or any business selling identifiable high-ticket items

Real-world example: A DTC furniture brand finances 50 sofas at $2K each directly from the manufacturer, paying only interest until each sofa sells online

4. Warehouse Financing

Inventory is deposited in a controlled third-party facility that issues warehouse receipts. The lender advances 60-80% against those receipts, and goods are released incrementally as the loan is repaid.

💰 Typical APR: 8-20% (plus warehouse fees of 1-3%)

Best for: Importers with large container shipments or commodity businesses holding high raw-material value

Real-world example: A wholesale electronics importer stores $500K of containerised goods in a bonded warehouse, draws $350K against warehouse receipts while goods clear customs and are distributed

5. Purchase Order (PO) Financing

Capital advanced against confirmed customer purchase orders, before inventory even exists. The PO lender advances 60-90% of order value directly to your supplier, then collects from the end buyer upon delivery.

💰 Typical cost: 1.5-6% per 30 days (effective APR: 18-72%)

Best for: Businesses fulfilling large wholesale orders from creditworthy retail partners

Real-world example: A DTC brand receives a $200K order from Nordstrom, uses PO financing to pay their manufacturer $140K, and Nordstrom pays the lender directly upon delivery

6. Consignment Financing

The supplier retains ownership of inventory until it sells. You hold goods on consignment and pay only after a sale occurs, with zero upfront financing cost, but margins shrink 10-20% as suppliers price in their carrying risk.

Best for: New brands without capital history, or test-run product launches

❌ Drawback: Limited inventory control; suppliers may prioritise their own direct channels over yours

7. Inventory Factoring

Selling inventory-backed receivables or projected sales at a discount for immediate cash. A factor purchases outstanding invoices at 70-90% of face value, collects from buyers, then remits the balance minus fees.

💰 Typical cost: 2-5% per invoice (effective APR: 20-60%)

Best for: High-invoice-volume businesses needing same-week liquidity

⚠️ Fastest structure available, but the most expensive per dollar of capital accessed

Q3: How Much Does Each Type of Inventory Financing Cost in 2026? [toc=Inventory Financing Costs 2026]

Inventory financing costs span an enormous range, from 5% APR for a bank-backed line of credit to 72% effective APR for high-risk purchase order financing. The type you choose determines your cost far more than your credit score or business history. Below is a master comparison of 2026 rate benchmarks across all seven structures, followed by two worked dollar-amount examples that reveal how much the wrong choice can actually cost.

💰 Master Cost Comparison Table: All 7 Types (2026 Benchmarks)

Option A - Inventory Line of Credit: Draw $50K at 12% APR, repay over 4 months. Total interest cost: ~$1,000.

Option B - Inventory Term Loan: Borrow $50K at 16% APR on a 12-month term. Even if you could repay in 4 months, a prepayment penalty locks you into the full schedule. Total interest + fees: ~$4,300.

💸 The dollar gap: Choosing the wrong structure wastes $3,300 on a $50K restock, a 6.6% margin hit that goes straight off your bottom line.

The same $50K restock costs $1,000 or $4,300 depending on which inventory financing structure you choose. That $3,300 gap is a 6.6% margin hit.

Worked Example 2: Large Import Container ($200K)

Option A - Warehouse Financing: $200K at 10% APR + 2% warehouse fee + $3K appraisal = ~$16,000 total cost over 6 months. Setup time: 3 weeks.

Option B - PO Financing: $200K at 3% per 30 days for 4 months = ~$24,000 total cost. Setup time: 5 days.

⚠️ The trade-off: Warehouse financing saves $8,000 but takes 3 weeks to arrange. PO financing costs 50% more but deploys capital in under a week. When the container arrives before peak season, those extra selling days may offset the premium entirely.

⚠️ Hidden Costs Most Lenders Won't Volunteer

The advertised APR rarely reflects your true all-in cost of capital. LendingTree's January 2026 market listings show inventory financing products ranging from high single-digit starting rates to APRs above 30% depending on repayment structure, confirming that the sticker rate is rarely the final number. Watch for these line items:

Quarterly re-appraisal fees: $1,500-$5,000 per appraisal, potentially $6K-$20K annually

Field exam charges: $2,000-$4,000 per lender visit to inspect collateral

Monitoring/reporting fees: $200-$500/month for ongoing inventory tracking

Prepayment penalties: 1-3% of outstanding balance if you repay early

Forced-placed insurance: Lender-arranged coverage at premium rates if your inventory insurance lapses

Unused line fees: 0.25-0.5% charged on undrawn balances of revolving credit facilities

Q4: What Are the Key Benefits of Inventory Financing Over Traditional Business Loans? [toc=Benefits Over Traditional Loans]

✅ Operational Advantages: Speed, Flexibility, and Cash Flow Alignment

The most immediate benefits of inventory financing are operational, and for e-commerce brands running on thin margins and tight seasonal windows, these advantages directly impact revenue capture. Online inventory lenders typically fund within 2-7 days, compared to the 6-8 weeks required by traditional bank loans, a speed differential that determines whether you restock a viral product before momentum dies or watch a competitor capture the demand you created. Collateral flexibility is another structural advantage: your inventory itself secures the loan, eliminating the personal guarantees or real-estate liens that most bank facilities demand. This means founders don't risk personal assets to fund business growth. Revolving structures like inventory lines of credit take this further; draw $20K in a slow month and $80K ahead of Q4, paying interest only on what you've actually used. For e-commerce businesses with cyclical demand, this cash flow alignment prevents the costly double penalty of paying interest on idle capital during off-peak months while scrambling for liquidity when seasonal spikes arrive.

💰 Strategic Benefits: Margins, Credit Building, and Growth Velocity

Beyond daily operations, inventory financing unlocks compounding strategic advantages. Bulk purchase leverage is among the most overlooked: paying suppliers early can yield 2-5% discounts that partially or fully offset financing costs, effectively turning borrowed capital into a margin improvement tool. A DTC brand financing $200K in Q3 inventory at 12% APR but capturing a 4% early-payment discount reduces its effective financing cost to roughly 8%, a meaningful difference at scale. Successful repayment history with asset-based lenders builds a credit trajectory that opens doors to larger, cheaper facilities over time, a virtuous cycle entirely unavailable to bootstrapped brands that avoid debt. And unlike venture capital or angel investment, inventory financing involves zero equity dilution: you retain 100% ownership and full operational control while accessing growth capital. The revenue impact is direct; brands that maintain consistent inventory availability during demand surges capture significantly more revenue than competitors who stock out and lose customers to alternatives permanently.

⭐ Why Inventory Financing Structurally Outperforms Traditional Loans for E-commerce

The comparison against traditional business loans reveals why inventory financing has become the default growth capital structure for scaling DTC brands. Traditional term loans require 2+ years of financial history, strong personal credit scores (typically 680+), and frequently demand personal guarantees that put founders' homes and savings at risk. Inventory financing is accessible to businesses with as little as 6-12 months of operating history, because the physical goods themselves reduce lender risk; approval depends on what you sell and how fast it turns, not how long you've been selling.

For e-commerce specifically, modern inventory lenders accept real-time sales velocity data from platforms like Shopify, Amazon, and WooCommerce as underwriting evidence, a digital-native approval path entirely unavailable through traditional banking relationships. Transaction volume, return rates, customer lifetime value, and inventory turnover all feed into automated underwriting models that traditional banks have not replicated. According to the Federal Reserve's 2025 report, 59% of small employer firms sought new financing in the prior 12 months, yet traditional bank approval processes remain fundamentally misaligned with the speed at which e-commerce businesses need to deploy capital. This accessibility matters most at the growth inflection point: the stage where a brand has proven product-market fit and identified winning channels but lacks the working capital to scale. At that stage, a 6-week bank approval cycle isn't just slow; it's a direct competitive advantage surrendered to brands with faster capital access.

Q5: What Are the Real Risks of Inventory Financing and When Should You Avoid It? [toc=Risks and When to Avoid]

If you default on an inventory-secured facility, the lender seizes your goods. That's the risk every guide covers, and it's the least likely scenario for most e-commerce brands with healthy sell-through rates. The real dangers are subtler, more common, and far more expensive. Lenders rarely volunteer them during the sales process, and founders often discover them only after the facility is already active.

Collateral seizure is the risk every guide covers. The four hidden risks below the waterline are subtler, more common, and far more expensive.

⚠️ The Depreciation and Obsolescence Trap

Fashion, seasonal, and trend-driven inventory loses value on a timeline that doesn't care about your repayment schedule. If your advance was based on a $200K valuation and the liquidation value drops to $80K because a trend expired or the season ended, you're underwater, owing more than the collateral is worth. This is especially dangerous for fast-fashion, consumer electronics, and novelty products where shelf life is measured in weeks, not months. Ramp's 2026 inventory financing analysis confirms that if inventory becomes obsolete, damaged, or harder to sell, its collateral value declines, reducing the effectiveness of the loan security and increasing default risk.

💸 Over-Leveraging and the Lender Incentive Problem

Many financing providers have structural incentives to push larger advances because they earn more fees on bigger facilities. Founders who take $300K when they need $50K pay interest on $250K of idle capital, eroding margins silently every month. This isn't theoretical. Multiple founders have documented being pressured into larger advances than needed, only to face repayment stress when growth didn't materialise as projected. One Wayflyer borrower described the experience bluntly:

"They will pretend to understand your business and act as if want to help you continually grow... The worst part is, as typical with these kinds of companies, the underwriters are behind the scenes. If they come back with something nonsensical, which they did, you can't prove them otherwise." Mike M Wayflyer - TrustPilot Verified Review

"After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute. This caused significant disruption to our operations and cash flow." Geoff Brand Wayflyer - TrustPilot Verified Review

⏰ Seasonal Mismatch and Covenant Violations

Taking inventory financing in August for Q4 stock means 3-4 months of interest accrual before revenue flows. If the season underperforms by even 20%, you're servicing debt from operating cash flow, precisely the cash you need for ads, fulfilment, and payroll. Covenant violations compound this: many facilities require minimum inventory turnover ratios, maintenance of borrowing base, or periodic financial reporting. Breaching these triggers acceleration clauses, the full balance due immediately, even if you've never missed a single payment.

❌ When You Should Avoid Inventory Financing Entirely

Gross margins below 25%, financing costs will erode profitability to breakeven or worse

Inventory turnover slower than 90 days, carrying costs compound faster than revenue arrives

Financing speculative inventory, unproven SKUs, untested markets, or first-run products

Existing significant debt, stacking inventory financing on top of active obligations increases blowup risk

Highly perishable or trend-dependent goods with unpredictable shelf life

✅ Risk Mitigation Strategies

Take only what you can deploy within 30 days, never let financed capital sit idle

Model the worst-case scenario before committing: what if this inventory sells 50% slower?

Diversify collateral, don't put all SKUs into one facility

Maintain insurance on financed inventory at all times

Build exit planning into every financed purchase, know your breakeven before signing

An AI-powered data layer that can simulate the downstream cash-flow impact of any financing decision against your actual sales velocity, margin structure, and operating costs before you commit transforms risk mitigation from guesswork into modelled confidence.

Q6: How Do You Qualify for Inventory Financing and What Do Lenders Require? [toc=Qualification Requirements]

Eligibility for inventory financing varies dramatically depending on whether you're approaching a traditional bank, an online alternative lender, or a specialty asset-based lender. Understanding which tier you qualify for, and what documentation to prepare, can shave weeks off the funding timeline and significantly improve the terms you receive.

💰 Eligibility by Lender Type

Inventory Financing Eligibility by Lender Type

Lender Type

Min. Time in Business

Min. Annual Revenue

Credit Score Required

Primary Underwriting Focus

Traditional Banks

2+ years

$500K+

650+ (business)

Financial statements, collateral quality

Online/Alternative Lenders

6-12 months

$100K+

500+ (flexible)

Sales velocity, platform data

Specialty ABL Lenders

6+ months

Varies

Less relevant

Inventory quality, turnover, liquidation value

Banks require audited financials, personal guarantees, and extensive credit history. Online lenders like Fundbox or BlueVine lean on real-time commerce data, Shopify sales reports, Amazon payout history, and can approve businesses that banks would reject outright. Specialty asset-based lenders focus almost entirely on the inventory itself: turnover rate, SKU diversity, perishability, and liquidation value.

⭐ The 5 Universal Factors That Determine Approval and Terms

Regardless of lender type, five factors consistently drive both approval decisions and the advance rate you receive:

SKU concentration, lenders prefer diversified inventory across many products vs. 2-3 hero SKUs

Inventory type, finished goods receive higher advance rates (60-80%) than raw materials (40-60%) or work-in-progress (30-50%)

Storage conditions, goods in a controlled, insured warehouse score higher than self-stored inventory

Sales channel reliability, Amazon/Shopify sellers with 12+ months of verified sales history receive preferred treatment from most modern lenders

📝 The Complete Documentation Checklist

Prepare these before approaching any lender to avoid delays:

Last 12 months of bank statements

Most recent annual financial statements (P&L, balance sheet, and cash flow statement)

Detailed inventory list with SKU-level quantities, costs, and retail values

Inventory aging report showing how long each product category has been held

Accounts receivable and accounts payable aging reports

Tax returns (last 2 years, required by bank lenders, optional for online)

Business licences and entity formation documents

Insurance certificates covering inventory

Sales forecasts for the next 6-12 months

Supplier contracts and purchase order records

⏰ Step-by-Step Application Process

Prepare documentation above, completeness is the single biggest factor in approval speed

Get 2-3 quotes from different lender types (bank + online + specialty) to create pricing leverage

Lender conducts inventory appraisal, desk appraisal for online lenders, field exam for banks and ABL

Receive term sheet with advance rate, interest rate, fee schedule, and covenants

Negotiate terms (see Q8 for specific tactics)

Sign agreement, a UCC lien is filed against your inventory

Funds disbursed, 1-5 days for online lenders, 2-6 weeks for banks

Begin repayment per schedule while maintaining required inventory levels

✅ A Pro Tip for E-commerce Founders

Connect your Shopify or Amazon analytics during the application to demonstrate real-time sales velocity. Modern inventory lenders who can see live turnover data will typically offer 10-15% higher advance rates than those working from static spreadsheets. An AI layer that consolidates commerce, accounting, and inventory data into a single view can auto-generate most of the documents above and present lender-ready financials on demand, turning a 10-hour preparation exercise into a 30-second query.

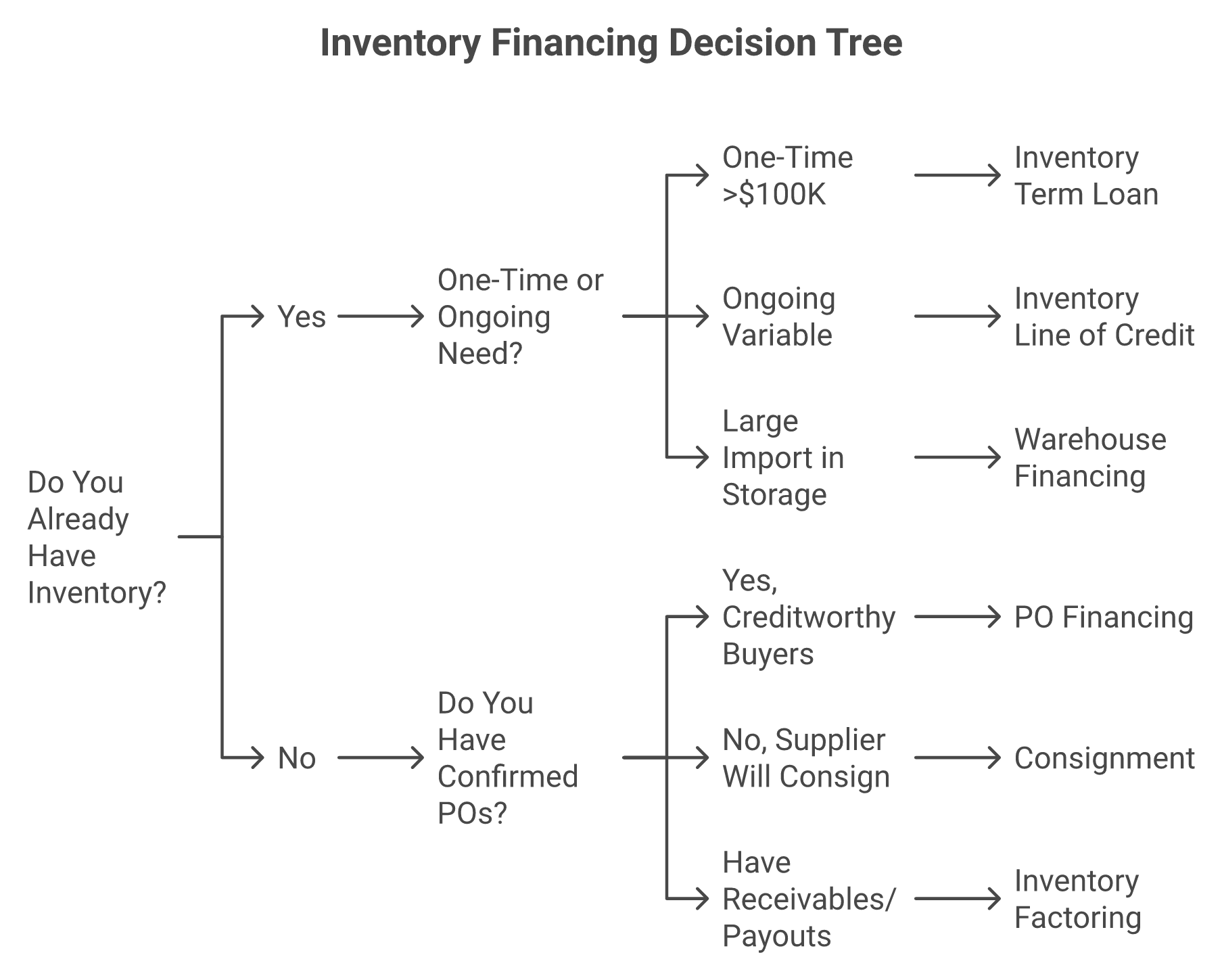

Q7: How Do You Choose the Right Type and Can You Stack Multiple Types? [toc=Choosing and Stacking Types]

Choosing the right inventory financing structure isn't about finding the "best" type; it's about matching the structure to your specific inventory lifecycle stage, purchase frequency, and speed requirements. The wrong match costs more than the financing itself: it ties up capital, creates repayment friction, and constrains the very growth it was meant to fund.

💰 The 4 Decision Variables

Every inventory financing decision starts with four questions:

Do you already have inventory, or do you need to buy it?

Is this a one-time large purchase or an ongoing revolving need?

How fast do you need capital?

What's your total cost tolerance?

Your answers determine which branch of the decision tree applies, and choosing the wrong branch is the most expensive mistake founders make with inventory financing.

Start with two questions to narrow seven financing types down to the one that matches your inventory stage, purchase pattern, and speed requirement.

✅ Decision Path 1: "I Already Have Inventory and Need Cash Against It"

Inventory Line of Credit, best for ongoing, variable needs where you pay interest only on draws

Inventory Term Loan, best for one-time, fixed-amount needs with predictable repayment

Warehouse Financing, best for large import shipments already in storage, with the highest advance rates but slower 2-4 week setup

✅ Decision Path 2: "I Need to Buy Inventory but Don't Have Cash"

PO Financing, if you have confirmed purchase orders from creditworthy buyers (fastest, but most expensive at 18-72% effective APR)

Consignment, if your supplier will retain ownership until sale (zero financing cost, but 10-20% margin trade-off)

Inventory Factoring, if you have receivables or pending payouts you can sell for immediate cash (1-3 day funding)

⚠️ Industry-Specific Guidance

Best-Fit Inventory Financing by Business Type

Business Type

Best-Fit Structure

Watch Out For

DTC / E-commerce

Inventory LOC or PO Financing

Amazon FBA inventory stored in Amazon's warehouses, some lenders won't accept it as collateral

Retail (high-ticket)

Floor Plan Financing

Curtailment penalties if units don't sell within the floor plan window

Wholesale / Distribution

Warehouse Financing or ABL

Warehouse fees (1-3%) stacking on top of interest

Manufacturing

Consignment for raw materials; Term Loans for finished goods

WIP (work-in-progress) typically receives lowest advance rates (30-50%)

One Reddit user running a small-margin e-commerce business shared a practical alternative to formal inventory financing that highlights the importance of matching structure to need:

"One effective strategy has been to negotiate terms with our vendors and manufacturers. At the very least, we secure 30-day payment terms, while larger manufacturers often provide us with 90-day terms. For seasonal inventory and promotional orders, we can sometimes negotiate terms extending to 120-180 days." u/Kelvinh6354, r/ecommerce Reddit Thread

💸 Hybrid Stacking Strategies

Many scaling e-commerce brands use 2-3 types simultaneously for different stages of the inventory cycle. A common stack: (1) PO financing to fund the supplier order, (2) warehouse financing while the container clears customs, (3) inventory LOC for ongoing restocking once goods arrive and start selling. The critical risk with stacking: multiple lenders each file UCC liens on your assets, and subordination agreements become essential. Make sure lien priority is explicitly documented before signing multiple facilities.

The Question Most Frameworks Miss

"Should I take financing at all for this inventory?" requires modelling downstream impact. If you finance $80K at 15% APR and it turns in 60 days at 45% gross margin, the ROI is clear. But if turnover stretches to 120 days and margin drops to 30%, the math breaks entirely. An AI simulation layer that models these scenarios against your actual historical sales velocity, ad spend efficiency, and cash position answers this question before you commit, something no spreadsheet or lender dashboard can do dynamically.

Q8: What Negotiation Tactics Can Lower Your Inventory Financing Costs? [toc=Negotiation Tactics]

Most founders accept the first term sheet they receive. This is the single most expensive mistake in inventory financing, not the interest rate itself, but the assumption that terms are non-negotiable. The reality: inventory financing terms are highly negotiable, especially for businesses with strong turnover ratios, clean inventory data, and multiple lender options on the table. These seven tactics can reduce your total cost of capital by 15-30%.

💰 Tactics 1-4: Leverage, Valuation, and Fee Reduction

Get competing term sheets and use them as leverage, even if you prefer one lender, presenting a competitor's lower rate creates immediate pricing pressure. Lenders expect this; founders who don't do it leave money on the table.

Negotiate the appraisal method, push for NOLV (Net Orderly Liquidation Value) instead of FLV (Forced Liquidation Value). NOLV-based appraisals value your inventory 15-25% higher, which directly increases your borrowing capacity without changing anything about your actual inventory.

Reduce appraisal frequency, push for semi-annual instead of quarterly field exams. At $1,500-$5,000 per appraisal, this saves $3K-$10K annually, a cost that most founders don't factor into their total cost of capital.

Eliminate prepayment penalties, most lenders will waive these when pressed, especially on revolving lines of credit. Prepayment penalties are pure margin for the lender and add zero value to your facility.

⭐ Tactics 5-7: Performance-Linked and Structural Advantages

Negotiate a step-down interest rate tied to turnover performance, if your inventory turnover ratio improves over 6 months, your rate drops automatically. This aligns lender incentives with your operational efficiency.

Offer real-time inventory visibility in exchange for better terms, giving lenders live API access to your inventory management system (Shopify, NetSuite, or similar) reduces their monitoring risk, which they'll trade for 10-15% higher advance rates.

Negotiate the borrowing base formula, push to include in-transit inventory (not just warehouse stock) in the borrowing base calculation. For importers with 30-60 day shipping windows, this can expand your effective facility size by 20-40%.

Reddit users in the procurement space have echoed this approach of negotiating structure over price:

"It's crucial to negotiate payment terms rather than just focusing on the price. I successfully secured 30/70 payment terms (30% deposit and 70% prior to shipment) instead of the typical 50/50. This arrangement significantly improved my cash flow, far more than a minor price reduction would have." u/procurement user, r/procurement Reddit Thread

📝 Pre-Signing Checklist: 10 Questions to Ask Every Lender

Before signing any inventory financing agreement, get clear answers to these:

What is my all-in cost of capital including every fee?

What appraisal method are you using, FLV or NOLV?

How often will you re-appraise, and what does each appraisal cost?

Is there a prepayment penalty, and can it be waived?

What happens if inventory depreciates below the advance amount?

What covenants or financial ratios must I maintain?

Can I draw and repay flexibly, or is this a fixed-term structure?

Do you require a personal guarantee or a blanket UCC lien?

How quickly can I access funds post-approval?

What reporting and monitoring do you require from me on an ongoing basis?

✅ The Ultimate Negotiating Advantage

Walking into a lender conversation with your exact inventory turnover ratio, days of inventory outstanding, gross margin by SKU, cash conversion cycle, and projected sell-through rate transforms the dynamic entirely. Founders who present this data command better terms because they reduce lender uncertainty, the primary driver of pricing premiums. An AI data layer that consolidates your Shopify, accounting, and inventory data and calculates these metrics in real time, plus generates lender-ready reports on demand, turns what's normally a 10-hour spreadsheet exercise into a 30-second query.

Q9. How Does Inventory Financing Compare to Other Funding Options? [toc=Comparison With Other Funding]

Inventory financing is one tool in a broader working-capital toolkit, and it's not always the right one. Founders frequently confuse it with adjacent funding options or miss better-fit alternatives entirely. The comparison below maps every major alternative against the decision variables that matter most: cost, speed, collateral requirements, and ideal use case.

💰 Master Comparison: Inventory Financing vs. 8 Alternatives

Inventory Financing vs. 8 Alternative Funding Options

AI-native capital platforms represent the newest financing category. Unlike inventory financing that requires physical collateral or RBF providers that rely on static 90-day snapshots, these platforms use real-time commerce, marketing, and financial data for continuous underwriting. Capital pricing adjusts dynamically with each advance; a strong performance month lowers your cost automatically, rather than locking you into rates set during an outdated application window.

The contrast with traditional RBF pricing is significant. Multiple founders have highlighted the opacity and rigidity of legacy providers:

"Pretty expensive product at 35-40% APR. Even worse support… Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% / 4 months = 12 months = 36% APR. In the best case." Julian Fernau Clearco - TrustPilot Verified Review

"Good value for money? No. Quick money in a pinch? Yes." u/nkl7e6h, r/Shopify Reddit Thread

❌ Where Each Alternative Falls Short

RBF, repayment as a percentage of sales means total cost rises when revenue slows; zero guidance on capital deployment

SBA Loans, best rates available, but 60-90 day approval processes eliminate them for seasonal inventory timing

MCAs, fastest funding available, but effective APRs of 40-150% make them viable only as emergency capital

Invoice Factoring, designed for B2B sellers with outstanding invoices; not suited for DTC consumer-facing brands

Vendor Credit, free and flexible, but terms rarely exceed 90 days and don't scale for large orders

✅ Choosing the Right Fit

Inventory financing wins when you have physical goods as collateral and need $50K-$500K. AI-native capital wins when you need speed, dynamic pricing, and right-sized advances without collateral requirements. RBF wins when you lack physical collateral entirely. SBA loans win when time is not a constraint and you want the absolute lowest rate available.

Q10. Who Provides Inventory Financing in 2026 and How Do You Evaluate Lenders? [toc=Evaluating Lenders in 2026]

The inventory financing provider landscape in 2026 spans five distinct tiers, from AI-native capital platforms to traditional banks, each serving different business profiles, risk appetites, and speed requirements. Choosing the right tier matters as much as choosing the right financing type, because provider architecture directly determines your pricing, flexibility, and experience.

The 2026 provider landscape spans five tiers. Your business profile determines which tier offers the best combination of cost, speed, and flexibility.

⭐ Provider Tier 1: AI-Native Capital Platforms

The newest category in 2026. These platforms use real-time commerce and financial data for continuous underwriting; your facility adjusts automatically as business performance changes. Key characteristics: same-day to 24-hour disbursal, no personal guarantee, dynamic pricing that drops as performance improves, frequent small advances (€10K-€50K) rather than one large lump sum, and one-click deployment with no per-advance application paperwork. Best for e-commerce brands doing €1M-€20M who want capital that scales with them without reapplying.

Provider Tier 2: Traditional Banks, cheapest rates (7-15% APR) but slowest (3-6 week approval), requiring extensive documentation, personal guarantees, and 2+ years operating history. Best for established businesses with strong banking relationships.

💰 Provider Tiers 3-5: Online, Specialty, and Supply Chain

Tier 3: Online/Alternative Lenders (Fundbox, BlueVine, OnDeck, Kickfurther), mid-range rates (12-25% APR), fast approval (2-7 days), and lighter documentation. They pull data directly from accounting software and bank feeds. Kickfurther, for example, funds up to 100% of inventory costs with payments deferred until goods sell. Best for growth-stage businesses that don't yet qualify for bank facilities.

Tier 4: Specialty Asset-Based Lenders, pure-play collateral lenders focused almost entirely on inventory quality (10-22% APR). They employ field examiners for physical appraisals and set detailed borrowing bases. Best for manufacturers, wholesalers, and importers with high-value physical inventory.

Tier 5: Embedded Platform Capital (Shopify Capital, Amazon Lending), zero-application friction with offers based on platform sales data. Shopify Capital offers funding from $200 to $2M with no credit checks, but terms are non-negotiable, invitation-only, and typically more expensive than independent alternatives.

⚠️ Red Flags That Signal a Problematic Lender

The reviews paint a consistent pattern of warning signs across multiple financing providers:

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC… they can enter your building and take your property in excess of the value of what is owed." Zachary Piech Wayflyer - TrustPilot Verified Review

"They trick you into signing a low APR contract, and then one month into the term, they hike up the rates by offering more funds… Almost destroyed my 7-year-old business in a matter of a couple of months." Khalid 8fig - TrustPilot Verified Review

Watch for these specific red flags:

❌ Pressure to take a larger advance than requested

❌ Vague or opaque all-in cost disclosures

❌ Blanket UCC lien requirement for small facilities

❌ No clear process for lien release after repayment

❌ No direct phone support, email-only during disputes

⏰ 2026 Market Trends Reshaping the Landscape

Three shifts are redefining inventory financing in 2026. First, AI-driven inventory valuation, lenders increasingly use machine-learning models trained on sell-through data and seasonal patterns for real-time appraisals, reducing costs and enabling dynamic borrowing bases. Second, continuous underwriting, the shift from static application snapshots to always-on underwriting that updates terms as performance changes, pioneered by AI-native platforms. Third, embedded financing, capital offered directly within Shopify and Amazon with zero-friction applications, though typically at higher effective rates and with limited term negotiability.

Q11. Frequently Asked Questions About Inventory Financing [toc=FAQ]

Can startups get inventory financing?

Most traditional inventory lenders require 6-12 months of operating history and existing inventory on hand. Startups without inventory may qualify for purchase order financing (if they have confirmed POs from creditworthy buyers) or consignment arrangements with suppliers. E-commerce-specific platforms that underwrite based on real-time sales velocity data rather than business age offer the most accessible path for early-stage brands; some AI-native platforms can begin underwriting with as little as 3 months of connected commerce data.

What credit score do you need for inventory financing?

Bank-backed facilities typically require a business credit score of 650+. Online and alternative lenders focus more on inventory quality and turnover velocity than credit score, with some accepting scores as low as 550. AI-native platforms and specialty asset-based lenders may bypass traditional credit scores entirely, underwriting instead on live commerce data, inventory health, and sell-through metrics.

⏰ How long does inventory financing approval take?

Approval timelines vary dramatically by lender type:

Inventory Financing Approval Timelines by Lender Type

Lender Type

Typical Approval Timeline

AI-native capital platforms

Same-day to 24 hours

Invoice factoring

1-3 days

PO financing

3-10 days

Online/alternative lenders

2-7 days

Specialty ABL lenders

1-3 weeks

Traditional banks

3-6 weeks

What happens if my financed inventory doesn't sell?

You remain obligated to repay regardless of sell-through performance. The lender may seize inventory as collateral, but if its liquidation value has dropped below the outstanding balance, you owe the shortfall, known as a deficiency balance. This is precisely why modelling worst-case sell-through scenarios and maintaining margin cushions before committing to any facility is critical. An AI simulation layer that tests "what if this inventory sells 50% slower?" against your actual data provides this safeguard before you sign.

⚠️ Can I use Amazon FBA inventory as collateral?

It's complicated. Because FBA inventory is stored in Amazon's fulfilment centres (not your warehouse), many traditional lenders won't accept it; they can't physically access or seize goods held by a third party. However, e-commerce-specialist lenders and AI-native platforms that integrate directly with Amazon Seller Central can use FBA inventory data for underwriting. Some will lend against it with modified advance rates, typically 10-20% lower than self-warehoused goods.

💰 Is inventory financing tax deductible?

The interest paid on inventory financing is generally deductible as a business expense. However, specific treatment varies by jurisdiction and business structure; consult your accountant for your particular situation. The financed inventory itself follows your existing inventory accounting method (FIFO, LIFO, or weighted average) for tax purposes, unaffected by the financing structure.

Can I get inventory financing with bad credit?

Yes, through asset-based lenders and factoring companies that focus on collateral value rather than creditworthiness. Expect higher rates (18-35% APR) and lower advance rates (40-60%) compared to borrowers with strong credit profiles. Improving your inventory turnover ratio and providing real-time inventory visibility through connected platforms can partially offset a weak credit profile during negotiations, as these signals reduce lender uncertainty about repayment capacity.

FAQ's

What is the cheapest type of inventory financing for ecommerce brands?

We find that the cheapest type depends entirely on your purchase pattern and repayment speed. For ongoing, variable restocking needs, an inventory line of credit (5-18% APR) consistently delivers the lowest effective cost because you pay interest only on drawn amounts, not the full facility.

For one-time large purchases, an inventory term loan (7-25% APR) can be cost-effective if you negotiate away prepayment penalties. However, the cheapest option on paper isn't always the cheapest in practice. Hidden costs like quarterly re-appraisal fees ($1,500-$5,000 each), field exam charges ($2,000-$4,000 per visit), and unused line fees (0.25-0.5%) can add 3-8% to your true all-in cost annually.

We recommend comparing the total cost of capital, not just the stated APR. For brands that need frequent, right-sized capital injections, AI-native capital platforms offer dynamically-priced advances at 2-8% per advance with no hidden fees, no appraisal charges, and same-day deployment. The structure that is cheapest for your business depends on purchase frequency, turnover velocity, and how quickly you can repay.

Can I use Shopify or Amazon FBA inventory as collateral for financing?

We see this question constantly from ecommerce founders, and the answer depends on your lender type and where inventory is stored.

Shopify-connected inventory stored in your own warehouse or third-party logistics (3PL) provider is generally accepted as collateral by most lenders. Modern inventory lenders can integrate directly with Shopify's inventory management system to verify stock levels, turnover rates, and sales velocity in real time.

Amazon FBA inventory is more complicated. Because FBA goods are stored in Amazon's fulfillment centers (not your warehouse), many traditional lenders won't accept them as collateral since they cannot physically access or seize goods held by a third party. However, ecommerce-specialist lenders and AI-native platforms that integrate directly with Amazon Seller Central can underwrite against FBA data. Expect modified advance rates, typically 10-20% lower than self-warehoused goods.

We recommend connecting your sales platforms during any financing application. Lenders who can see live turnover data typically offer 10-15% higher advance rates than those working from static spreadsheets alone.

How do I choose between an inventory line of credit and a term loan?

We advise founders to start with two questions: Is this a one-time purchase or an ongoing need? and How predictable is your restocking cadence?

>Inventory Line of Credit (5-18% APR): Best when your monthly restocking amounts vary. You draw $30K one month, $70K the next, and pay interest only on what you use. Maximum flexibility and lowest effective cost when utilization fluctuates.>Inventory Term Loan (7-25% APR): Best for a single large purchase, such as a Q4 pre-season buy exceeding $100K, where you know the exact amount needed upfront and can plan fixed repayments.

The critical trap we see founders fall into is choosing a term loan for variable needs. Interest accrues on the full principal from day one, even if inventory sells ahead of schedule. If a prepayment penalty is attached (1-3%), the cost compounds further.

We built our financial management capabilities to model exactly this question. By connecting your sales data, we can simulate which structure produces the lowest total cost of capital based on your actual turnover velocity and seasonal patterns.

What are the biggest risks of inventory financing that lenders won't tell you?

We consistently see five risks that lenders rarely disclose during the sales process:

>Depreciation and obsolescence trap: If your advance was based on a $200K valuation and liquidation value drops to $80K because a trend expired, you owe more than the collateral is worth. This is especially dangerous for fashion, electronics, and seasonal products.>Over-leveraging incentives: Many financing providers push larger advances because they earn more fees on bigger facilities. Founders who take $300K when they need $50K pay interest on $250K of idle capital.>Covenant acceleration clauses: Many facilities require minimum inventory turnover ratios. Breaching these triggers the full balance due immediately, even if you have never missed a single payment.>Hidden fee stacking: Quarterly re-appraisals ($5K each), field exam charges ($4K per visit), and monitoring fees ($500/month) can add 3-8% to your true annual cost.>Blanket UCC liens: Some lenders file liens against all business assets for a small inventory facility, encumbering your entire company.

We designed our AI cash flow forecasting to model worst-case scenarios before you commit to any facility, transforming risk mitigation from guesswork into data-backed confidence.

How fast can I get inventory financing approved and funded in 2026?

We track approval timelines across every lender category, and the range in 2026 is dramatic:

>AI-native capital platforms: Same-day to 24 hours, no per-advance application>Invoice factoring: 1-3 days>PO financing: 3-10 days>Online/alternative lenders: 2-7 days>Specialty ABL lenders: 1-3 weeks (due to field examinations)>Traditional banks: 3-6 weeks with extensive documentation

The speed difference matters more than most founders realize. A 6-week bank approval cycle can mean missing an entire seasonal window. If your Q4 inventory needs to ship from the manufacturer in August, waiting until October for bank approval means the opportunity is gone.

We built our capital deployment to match the speed at which ecommerce actually operates. Through continuous underwriting based on real-time business data, we eliminate the reapplication cycle entirely. Your facility adjusts automatically as performance changes, so capital is available the moment an opportunity surfaces.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.png)