Revenue Based Financing for Ecommerce: How It Works, Costs, Providers Serve, Business Models, Contract Terms

14

mins read

In this article

TL;DR

RBF flat fees mask effective APRs of 28% to 56%+ depending on repayment speed and revenue trajectory.

Blanket UCC liens, weekly minimums, and discretionary defaults are the three most damaging hidden contract terms.

Wayflyer, Clearco, 8fig, Uncapped, and Shopify Capital each serve different business models with materially different risk profiles.

148 verified merchant reviews reveal a pattern: founders sign for speed, not clarity, and pay the price in hidden terms.

RBF fits time-bound growth initiatives with short cash conversion cycles; it damages businesses covering operating losses.

The RBF market is projected to reach $42.3B by 2027, but capital without intelligence remains the structural problem.

Luca AI eliminates blind spots by modeling effective APR, 180-day cash position, and contract red flags before signing.

Q1: What Is Revenue-Based Financing and Why Do Ecommerce Brands Use It Instead of Bank Loans? [toc=What Is RBF]

Revenue-based financing (RBF) gives ecommerce businesses a lump sum of capital upfront in exchange for a fixed percentage of daily or weekly revenue until the total amount, principal plus a flat fee, is repaid. There are no fixed monthly installments, no compounding interest, and no set end date. Repayment speed rises and falls with your sales volume.

How the Mechanics Work

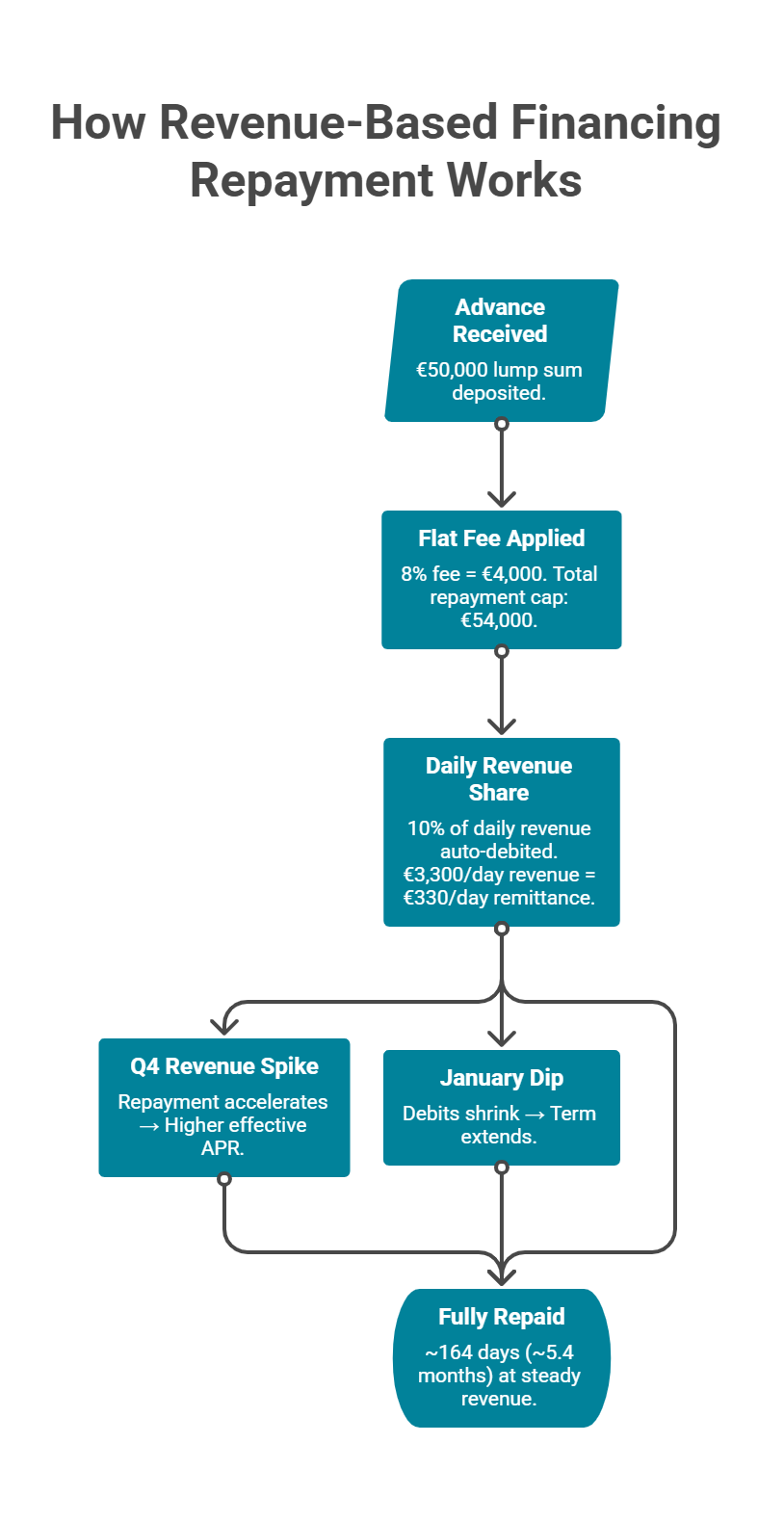

Here is a simplified example of how a typical RBF deal plays out:

💰 Advance amount: €50,000

Flat fee: 8% (€4,000 total cost)

Total repayment cap: €54,000

Revenue share (remittance rate): 10% of daily revenue

Monthly revenue: €100,000 (~€3,300/day)

At €330/day in remittance, the advance is fully repaid in approximately 164 days (~5.4 months). If sales spike during Q4, repayment accelerates. If January slows down, daily remittances shrink automatically.

Flowchart showing four stages of RBF repayment from advance to payoff with revenue spike and dip scenario branches.

Every RBF deal contains three variables that interact: the advance amount, the flat fee or repayment cap (often expressed as a multiple like 1.08x to 1.3x), and the remittance rate. A low flat fee paired with a high remittance rate can be more punishing to daily cash flow than a higher fee with a gentler remittance percentage.

⏰ Speed: RBF providers fund within 24 to 72 hours. Bank loans take 6 to 8 weeks, often longer for businesses without extensive credit histories.

No personal guarantees: Most RBF providers don't require founders to pledge personal assets, unlike SBA or term loans.

No equity dilution: You retain 100% ownership, critical for bootstrapped brands that have fought to reach product-market fit.

Seasonal alignment: Repayment automatically slows during low-revenue months (January, February) and accelerates during peaks (Q4), matching ecommerce's inherent cyclicality.

When a DTC brand identifies a winning Meta campaign in October and needs €50K for inventory within 48 hours, a 6-week bank approval process isn't structurally compatible with that opportunity window.

RBF vs. Merchant Cash Advance: A Distinction Most Articles Blur

One of the most common sources of confusion in ecommerce financing is the conflation of RBF with merchant cash advances (MCAs). Shopify Capital and Amazon Lending are MCAs, not RBF, and the differences matter.

RBF vs. Merchant Cash Advance

Dimension

Revenue-Based Financing

Merchant Cash Advance

Legal structure

Loan or revenue-sharing agreement

Purchase of future receivables

Repayment trigger

% of actual daily revenue (flexes)

Fixed daily/weekly debit (often rigid)

Cost expression

Flat fee as % of principal

Factor rate (e.g., 1.2x to 1.5x)

Flexibility

Genuinely variable with revenue

Appears flexible, often has minimum floors

Regulatory treatment

Subject to lending regulations in most jurisdictions

Often unregulated (not technically a loan)

Understanding which structure you're actually signing determines your legal protections, cost transparency, and exit options.

How Luca AI Approaches Ecommerce Capital

Luca AI offers ecommerce-native capital with dynamic pricing that adjusts in real-time based on current business health, not an application snapshot from weeks ago. Advances start at €10K with same-day deployment, no personal guarantees, and a remittance structure designed for how ecommerce cash flows actually work.

Q2: What Are the Real Pros and Cons of Revenue-Based Financing for Ecommerce Brands? [toc=RBF Pros and Cons]

Revenue-based financing solves a real timing problem for ecommerce brands, capital that arrives at the speed of opportunity rather than the speed of bank bureaucracy. But the flexibility comes at a price most founders underestimate until repayment is already underway.

✅ The Advantages

⏰ Speed to fund: Capital in 24 to 72 hours vs. 6 to 8 weeks for bank loans, matching ecommerce's fast-moving windows for Q4 inventory, winning campaign scale-up, or flash supplier deals.

💰 No equity dilution: Retain full ownership, critical for bootstrapped founders who've clawed their way to product-market fit.

No personal guarantees (most providers): Business risk stays in the business, your home isn't collateral.

Flexible repayment: Auto-adjusts to revenue, so slow months don't trigger default. January's dip reduces your daily debit automatically.

Low documentation burden: Most providers underwrite from platform data (Shopify, Stripe, Amazon Seller Central), no business plans, tax returns, or financial projections required.

❌ The Disadvantages

💸 High effective APR: Flat fees of 6% to 12% translate to 20% to 100%+ annualized depending on repayment speed. The faster your business grows, the more you actually pay in annualized terms, a counterintuitive trap.

Cash flow compression: Daily auto-debits reduce available cash for ad spend, inventory restocking, and operations, potentially constraining the very growth the capital was supposed to fund.

Small advance sizes: Typically capped at 1 to 3 months of revenue. If you need €500K for a major inventory buy or market expansion, RBF alone won't cover it.

Revenue requirements: Most providers require €10K to €50K+ in monthly revenue and 6+ months of trading history, excluding early-stage brands that arguably need capital the most.

⚠️ Misaligned incentives: Providers profit from deploying maximum capital, not from sizing capital optimally for your business. A €200K offer that generates more fees for the provider may be worse for your cash flow than €75K timed correctly.

"If you get money from them, make sure you do the math. 6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% to 4 months = 12 months to 36% APR. In the best case." -Julian Fernau Trustpilot Verified Review

The flat fee is marketing. The effective APR is reality. The faster your ecommerce business grows, the more you actually pay in annualized terms for the same RBF advance.

"They will pretend to understand your business and act as if they want to help you continually grow. The worst part is, as typical with these kinds of companies, the underwriters are behind the scenes. If they come back with something nonsensical, you can't prove them otherwise." -Mike M Trustpilot Verified Review

How Luca AI Addresses the Core Cons

Luca AI's dynamic pricing means your rate drops as your business improves, not locked to a static application snapshot. Optimal capital sizing means Luca recommends €50K when you need €50K, not €200K that sits idle while you pay fees on the full amount. Frequent smaller advances at real-time rates consistently produce lower total cost of capital than competitors' infrequent large lumps.

Q3: Which RBF Providers Serve Which Ecommerce Business Models? [toc=Provider Directory]

Not all ecommerce capital providers underwrite the same way, and applying to the wrong one wastes the one thing RBF is supposed to save: time.

Why Provider-Model Fit Matters

Amazon FBA sellers authenticate through Seller Central data. DTC Shopify brands verify revenue through Shopify + Stripe + Meta. A provider optimized for subscription commerce with predictable MRR may reject a seasonal DTC brand with 4x Q4 spikes. Multi-channel operators (DTC + wholesale + Amazon) face the longest due diligence because most providers can't reconcile revenue across disparate platforms.

Choosing a provider that doesn't fit your business model means 2 to 4 weeks lost in application cycles, precisely the window your inventory purchase or campaign scale-up can't afford to miss.

⭐ Provider Comparison Table

Ecommerce RBF Provider Comparison

Provider

Business Models

Min. Monthly Revenue

Funding Range

Fee Structure

Disbursal Speed

Geography

Luca AI

DTC, Multi-channel

€10K+

€10K to €500K

Dynamic (adjusts with health)

Same-day

EU/UK/US

Wayflyer

DTC, Amazon FBA, Multi-channel

~€20K+

€10K to €20M

5% to 10% flat fee

24 to 48 hours

US/UK/EU/AU

Clearco

DTC, SaaS-commerce

~€10K+

€10K to €20M

6% to 12% flat fee

48 hours

US/UK/EU/CA

Uncapped

DTC, Amazon, Subscription

~€15K+

£10K to £5M

6% to 12% flat fee

24 to 48 hours

UK/EU/US

8fig

Amazon FBA, DTC

~$8K+

$10K to $1M+

Varies by growth plan

3 to 5 days

US/UK/CA

Shopify Capital

Shopify merchants only

Platform-determined

$200 to $2M

MCA factor rate (1.1x to 1.3x)

1 to 3 days

US/UK/CA/AU

Amazon Lending

Amazon sellers only

Platform-determined

$1K to $750K

Fixed interest (varies)

1 to 5 days

US/UK/EU/JP

Outfund

DTC, SaaS

~£10K+

£10K to £2M

2% to 8% flat fee

48 hours

UK/EU

Viceversa

DTC, Subscription

€20K+

€10K to €1M

4% to 10% flat fee

48 to 72 hours

EU

Guidance by Business Model

If you're DTC on Shopify doing €30K to €100K/month → Luca AI offers same-day disbursal with dynamic pricing that adjusts to your trajectory. Wayflyer and Outfund are also strong options but use static fee models.

If you're Amazon FBA → 8fig and Amazon Lending have the deepest Seller Central integration. Amazon Lending is invitation-only with competitive rates but zero flexibility on terms.

If you're multi-channel (DTC + wholesale + Amazon) → Luca AI and Wayflyer underwrite across channels. Most other providers struggle with multi-platform revenue reconciliation, which is why merchants report rejections despite strong overall performance.

If you're subscription/SaaS-commerce → Uncapped and Viceversa specialize in recurring revenue models with predictable MRR.

Eligibility Reality Check

Most providers require 6+ months of trading history. Geography matters: Outfund and Viceversa are Europe-heavy; Amazon Lending is marketplace-only. Platform-integrated providers like Shopify Capital and Luca AI need zero paperwork; others may request bank statements, P&L, and tax returns. Always verify current eligibility before beginning an application process.

"I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues, this was incredibly disappointing." -Joshua Hannan Trustpilot Verified Review

Luca AI matches capital to your actual business data, channel mix, revenue trajectory, cash cycle, rather than making you apply blind to three providers and hope one fits. Dynamic pricing means the rate you see reflects today's performance, not a 90-day-old snapshot.

Q4: What Do RBF Contract Terms Not Make Obvious, and What Are Ecommerce Founders Actually Reporting? [toc=Hidden Contract Terms]

You accepted a €75K RBF offer with a 10% revenue share. The pitch was speed, flexibility, and zero equity dilution. Three weeks in, you discover the weekly auto-debits have a minimum floor, even when sales dip, the debit doesn't flex down. By month two, the provider has filed a UCC-1 blanket lien on your business assets, something the sales team never mentioned during onboarding. By month four, you want to take capital from a second provider, but the lien blocks it.

This is not hypothetical. It mirrors experiences reported by merchants across multiple providers and geographies.

⚠️ The 6 Contract Terms That Catch Founders Off Guard

These six contract terms appear in the fine print of most RBF agreements. Merchants across Wayflyer, Clearco, Uncapped, and 8fig report discovering them weeks after signing.

UCC-1 blanket lien filings: Providers quietly secure a lien against all business assets. Banks see the lien and decline your applications for other financing. One merchant discovered their provider claimed the right to "enter your building and take your property in excess of the value of what is owed."

Weekly minimum repayment floors: Override the "flexible percentage" during slow months, creating fixed-payment-like pressure when revenue dips. Your "flexible repayment" is only flexible upward.

"Default at discretion" clauses: The provider can call the full remaining balance for subjective reasons, including anything they believe you misrepresented in their opinion.

Clawback on refunded orders: You paid the revenue share on a sale that was later returned. The provider doesn't refund their cut.

Payout redirection rights: Contract clauses allowing the provider to redirect your Shopify or Stripe payouts directly to their own account if they deem you in default.

Lien release delays after payoff: Providers sitting on UCC filings for months after your balance reaches zero, blocking subsequent financing. One seller reported: "I have already paid these people off and they put a lien on my marketplace account. I asked for a letter of payoff and they have been lagging since November."

What Founders Are Actually Reporting

💸 Bait-and-switch on funding amounts. Merchants receive written approval for a specific amount, make critical business decisions based on that commitment, then get slashed at the last minute.

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M. Then, months later, right as we hit our 5% EBITDA margin, they cut it again to $350K." -Xin Shui Trustpilot Verified Review

❌ Ghost support post-signing. Sales teams vanish after contract execution. No phone support. Emails go unanswered for weeks.

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly, and then could never resolve these issues. We had to finally turn off the ACH ourselves." -Thomas Bishop Trustpilot Verified Review

⚠️ Unauthorized or accelerated debits. Repayments pulled faster than contracted, inflating the effective interest rate without notice.

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still file UCC. They can deem you in default for any reason at their discretion. They can redirect your Shopify funds to their account." -Zachary Piech Trustpilot Verified Review

How Luca AI Structures Capital Differently

Luca AI's capital terms are built for operators who've seen what opaque contracts look like. Dynamic pricing is always visible and always current, no static offers that get revised after signing. No UCC blanket liens. No weekly floors that override flexibility. No "default at discretion" language. Repayment genuinely flexes with revenue, and the terms you see before accepting are the terms that hold. Capital decisions should be made with full visibility into downstream impact, not discovered three weeks into repayment.

Q5: What Are the Most Common Grievances Ecommerce Founders Have With RBF Providers? [toc=Common RBF Grievances]

The most common grievances from ecommerce founders using RBF providers cluster around five recurring themes, and they are remarkably consistent across Wayflyer, Clearco, Uncapped, and 8fig regardless of provider size, geography, or how polished the onboarding experience felt. These aren't edge cases. They're structural patterns rooted in how most providers prioritize capital deployment over merchant outcomes.

⚠️ The Five Grievance Themes

💸 Bait-and-switch on funding amounts: Merchants receive written approval for a specific amount, make critical business decisions based on that commitment, then get slashed at the last minute. One 8fig merchant signed a $3M deal only to have funding cut to $1M weeks later, and then again to $350K during a critical expansion phase. A Wayflyer merchant received funding approval with confirmed terms, only for the decision to be "abruptly reversed at the last minute," causing "significant disruption to operations and cash flow".

❌ Ghost support post-signing: Sales teams are responsive, warm, and eager during onboarding. After the contract is signed, they vanish. No phone support. Emails unanswered for weeks. Multiple Clearco merchants reported that their sales rep "was always at hand prior to signing and accepting, now no longer responds". Uncapped merchants described sending emails and receiving nothing: "12 days later I have nothing. No refusal. No acceptance. Nothing".

💰 Unauthorized or accelerated debits: Repayments pulled faster than the contract stated, inflating the effective interest rate without merchant consent. One Clearco merchant had to "turn off the ACH ourselves" after the provider pulled funds ahead of schedule and went dark. An 8fig merchant reported a $23K debit "that was never owed," which 8fig later admitted was their mistake.

⏰ UCC lien retention after payoff: Providers sitting on blanket liens for months after the balance hits zero, blocking the merchant from accessing other financing. One 8fig merchant reported: "I have already paid these people off and they put a lien on my marketplace account. I asked for a letter of payoff and they have been lagging since November". Another had a lien remain active for over six months on a contract where zero funds were ever received.

Underwriting that doesn't understand ecommerce: Rejecting profitable, growing businesses because the underwriting model can't interpret multi-channel revenue, seasonal patterns, or non-standard data. Wayflyer rejected a merchant selling across "almost a dozen channels" because "marketing metrics weren't up to par on Facebook," ignoring profitability across every other platform.

What Merchants Are Saying

"One of the worst companies I've ever dealt with. They trick you into signing a low APR contract, and then one month into the term, they hike up the rates by offering more funds. They divide the lending into cycles. I only received one, the second and third funding were pulled at the last minute." -Khalid Trustpilot Verified Review

"They have the absolute worst customer service we have ever experienced. You won't hear back for WEEKS after sending an email. They will charge you OUTSIDE of the scheduled parameters. They've incorrectly charged me $4,600 and have had it for over a month with NO resolution." -AS Trustpilot Verified Review

"We genuinely thought they would be our partner, and that's what they've stated. As our business has gotten better in terms of growth and profitability, they had guaranteed they would lend us at a certain time only to let us down. Their salespeople are sleazy." -M Trustpilot Verified Review

How Luca AI Is Built Differently

Luca AI was built by ecommerce operators who experienced these exact frustrations firsthand. Capital terms are transparent from the start, dynamic pricing that adjusts with your real-time business health, no UCC blanket liens, no weekly minimum floors that override flexibility, and no "default at discretion" clauses. The terms you accept are the terms that hold. When the intelligence behind capital decisions lives inside the same system that deploys the capital, there's no gap between what's promised and what's delivered.

Q6: How Do the Biggest Ecommerce Brands Handle Working Capital, and What Can Scaling Founders Learn? [toc=Working Capital Best Practices]

Every DTC founder scaling past €1M looks at brands like Gymshark, Allbirds, or Warby Parker and asks the same question: how did they fund growth without losing control? The answer is more instructive than most realize, and it's not "they raised venture capital early." Gymshark bootstrapped to over £400M in revenue and a $1.45B valuation before accepting its first outside investment from General Atlantic in 2020, with zero debt on its books. Allbirds used a mix of equity rounds and structured credit facilities, recently securing a $75M facility from Second Avenue Capital to fund inventory and product expansion.

The Common Thread: Capital as Strategy, Not Panic

The connecting principle is that these brands treated working capital as a strategic function, planned 90 to 180 days ahead, matched to specific use cases, and modeled against cash conversion cycles. They didn't accept the first capital offer that arrived during a stockout. They built financial discipline into their operating rhythm.

Most scaling ecommerce brands do the opposite. They treat capital as an emergency lever pulled during Q4 crunches or when a winning Meta campaign needs fuel yesterday. This reactive approach leads to accepting whatever RBF offer arrives fastest, regardless of terms, the financial equivalent of buying plane tickets on the day of travel.

✅ Best Practices Worth Stealing

Separate inventory capital from ad-spend capital. These have fundamentally different payback profiles. Inventory has a 60 to 120 day cash conversion cycle; ad spend should return within 14 to 30 days. Funding both with the same RBF terms creates a mismatch that the faster-returning use case subsidizes.

Model cash conversion cycle before accepting any funding. If your inventory takes 90 days to convert to cash and your RBF repayment starts on Day 1, you're servicing debt from existing cash flow, not from returns the capital generates.

Maintain at least two funding relationships. Single-provider dependency means one underwriting policy change can strand your business mid-growth phase, exactly what multiple Wayflyer and 8fig merchants experienced.

❌ Worst Practices to Avoid

Stacking multiple RBF loans simultaneously without understanding UCC lien priority or combined daily debit load.

Using RBF to cover operational losses rather than growth investment, the auto-debits accelerate the cash drain rather than solving the underlying profitability problem.

Accepting the first offer without calculating effective APR at your specific revenue trajectory. A "7% flat fee" can translate to 30%+ APR depending on repayment speed.

How Luca AI Replaces the CFO Spreadsheet

Luca AI operates as the strategic capital planning layer that brands like Gymshark built with dedicated CFO teams and financial advisors, but accessible to founders without a full finance department. It models which capital type fits which use case, forecasts repayment impact on your cash conversion cycle, and surfaces funding at the moment the math supports it. The Intelligence + Capital thesis, not panic-driven borrowing.

The Lesson for €1M to €20M Founders

Gymshark's Ben Francis built a billion-pound brand by reinvesting profits methodically and resisting external capital until the timing was strategically right. For the founder without Gymshark's brand leverage or organic demand, the lesson is clear: the intelligence behind when and how to deploy capital matters more than the capital itself. Speed without strategy is just expensive chaos.

Q7: Revenue-Based Financing vs. Merchant Cash Advance vs. Line of Credit, Which Fits Your Ecommerce Model? [toc=RBF vs MCA vs Credit Line]

Ecommerce founders evaluating non-dilutive capital typically encounter three options: revenue-based financing (RBF), merchant cash advances (MCA), and revolving lines of credit. They sound similar in pitch decks and provider landing pages, but they operate on fundamentally different mechanics. Choosing wrong doesn't just cost more, it constrains your cash flow in ways that limit the very growth the capital was supposed to fund.

How Each Option Actually Works

Revenue-Based Financing charges a flat fee (typically 6% to 12% of the advance) and collects a fixed percentage of daily or weekly revenue until the total repayment cap is reached. Repayment genuinely flexes with sales volume, slow months mean smaller debits. Best for brands with consistent revenue wanting predictable, flexible payback on a specific growth initiative.

Merchant Cash Advances provide a lump sum in exchange for a factor rate applied to future receivables (e.g., 1.2x to 1.5x). Technically not a loan, it's a purchase of future revenue. Shopify Capital and Amazon Lending operate as MCAs. Daily debits are often fixed or have minimum floors regardless of revenue dips, making the "flexible" marketing claim misleading in practice.

Lines of Credit let you draw and repay as needed, with interest charged only on the drawn amount. Best for brands with variable, ongoing capital needs. Requires stronger credit history, longer approval timelines (2 to 6 weeks), and often personal guarantees, but carries the lowest effective cost for qualified borrowers.

⭐ Side-by-Side Comparison

RBF vs. MCA vs. Line of Credit Comparison

Dimension

Revenue-Based Financing

Merchant Cash Advance

Line of Credit

Repayment structure

% of daily/weekly revenue

Fixed daily debit or % with floors

Interest on drawn amount, flexible repay

Typical effective APR

15% to 60%

40% to 350%

8% to 25%

Speed to fund

24 to 72 hours

1 to 3 days (platform-integrated)

2 to 6 weeks

Personal guarantee

Rarely required

Rarely required

Often required

Equity dilution

None

None

None

Best-fit model

DTC, subscription, multi-channel

Platform-native sellers (Shopify, Amazon)

Established brands with strong credit

Best-fit use case

Inventory buys, campaign scaling

Quick bridge financing, small advances

Ongoing variable needs, payroll, operations

Provider examples

Luca AI, Wayflyer, Uncapped, Outfund

Shopify Capital, Amazon Lending, PayPal Working Capital

Brex, Mercury, traditional banks

💰 When to Choose What

Choose RBF if you have predictable revenue and need capital for a specific, time-bound growth initiative, inventory for Q4, scaling a proven campaign, or bridging a cash conversion gap.

Choose MCA if you need speed above all else, the advance is small relative to your revenue, and you can tolerate a higher effective cost. Platform-native MCAs (Shopify Capital) require zero application effort.

Choose a Line of Credit if you have ongoing, variable capital needs across multiple use cases and can qualify. The lower APR and draw-as-needed flexibility make it the cheapest option for brands that meet the credit bar.

⚠️ Avoid stacking RBF + MCA simultaneously, the combined auto-debits can consume 25%+ of daily revenue, creating a cash flow vise that forces reactive cost-cutting across marketing and operations.

How Luca AI Helps You Choose

Luca AI doesn't just help you pick between these three, it models each option against your actual data. "Show me my cash position in 90 days if I take this RBF offer vs. this line of credit," answered in seconds, with the math your CFO would spend a day building in a spreadsheet. The right capital structure isn't a category decision. It's a business-specific calculation.

Q8: What Happens to Your Cash Flow After You Accept RBF, the Post-Funding Reality No One Models? [toc=Post-Funding Cash Flow Impact]

It's Month 2 of your €60K RBF advance. Your 12% daily revenue share seemed manageable when you signed, your store was generating €3,500/day. But you reinvested the capital into inventory that won't convert for 75 days. Meanwhile, €420/day is being auto-debited from your account. Your Meta ad budget just got quietly cut by your ops team because there isn't enough cash to fund both repayment and acquisition. The capital that was supposed to accelerate growth is now constraining it.

This scenario plays out across hundreds of ecommerce businesses every quarter, and no RBF provider models it for you before you sign.

Why the Cash Squeeze Happens

Most founders model RBF cost in isolation: "I can afford 12% of revenue." What they don't model is the interaction between repayment timing and cash conversion cycle. Consider the math:

For 75 days, you're servicing the RBF from existing cash flow, not from returns the capital generates. That's €31,500 in auto-debits before a single unit of funded inventory converts to revenue.

❌ The Negative Feedback Loop

The downstream effects compound:

Reduced ad spend during repayment → lower top-of-funnel traffic → lower revenue → slower repayment → extended term → higher effective APR

Deferred inventory restocking on non-funded SKUs → stockouts on best-sellers → lost revenue during peak conversion windows

Team bandwidth diverted to managing cash flow crises instead of executing growth strategy

This isn't a design flaw in RBF, it's a design flaw in how RBF is sold. Providers profit from deploying maximum capital. They have no incentive to model whether the deployment timing aligns with your cash conversion reality. Their model works whether yours does or not.

When inventory takes 75 days to convert and auto-debits start Day 1, the math creates a compounding cash squeeze that no provider models for you before signing.

💰 The P&L Impact: A Worked Example

Here's what a €100K/month DTC brand's monthly cash flow looks like with a 15% daily revenue share over 6 months:

Post-Funding Cash Flow Impact Over 6 Months

Month

Revenue

RBF Debit (15%)

Remaining for Operations

Impact

Month 1

€100K

€15K

€85K

Manageable, ad spend intact

Month 2

€90K (seasonal dip)

€13.5K

€76.5K

⚠️ Budget cuts begin

Month 3

€80K (dip continues)

€12K

€68K

❌ Meta spend cut 30%

Month 4

€70K (reduced acquisition)

€10.5K

€59.5K

❌ Inventory reorders delayed

Month 5

€75K (partial recovery)

€11.25K

€63.75K

⚠️ Stockouts on 2 top SKUs

Month 6

€85K (recovery)

€12.75K

€72.25K

Revenue below pre-funding baseline

The brand entered RBF at €100K/month and exits at €85K/month, with six months of reduced acquisition investment creating a hole that takes another quarter to recover from.

How Luca AI Models This Before You Sign

Before you accept any offer, Luca AI runs a forward-looking P&L simulation: your daily cash position for 180 days, factoring in the auto-debit schedule, your COGS cycle, your ad spend requirements, and seasonal revenue projections. If the model shows a cash squeeze in Month 2, you know before signing, not after. If the capital deployment should be staged in two smaller tranches 45 days apart instead of one lump sum, Luca surfaces that recommendation. Intelligence before capital, not regret after it.

Q9: How Should You Evaluate an RBF Offer Before Signing? A Pre-Signing Checklist for Ecommerce Founders [toc=Pre-Signing Checklist]

Before you sign any revenue-based financing agreement, score the offer against these 10 criteria. If you can't confidently answer 8 or more, you're signing with dangerous blind spots, and those blind spots are exactly where the most damaging contract terms live.

💰 The 10-Point RBF Due Diligence Checklist

1. Have you calculated the effective APR at your current revenue, not just the flat fee?

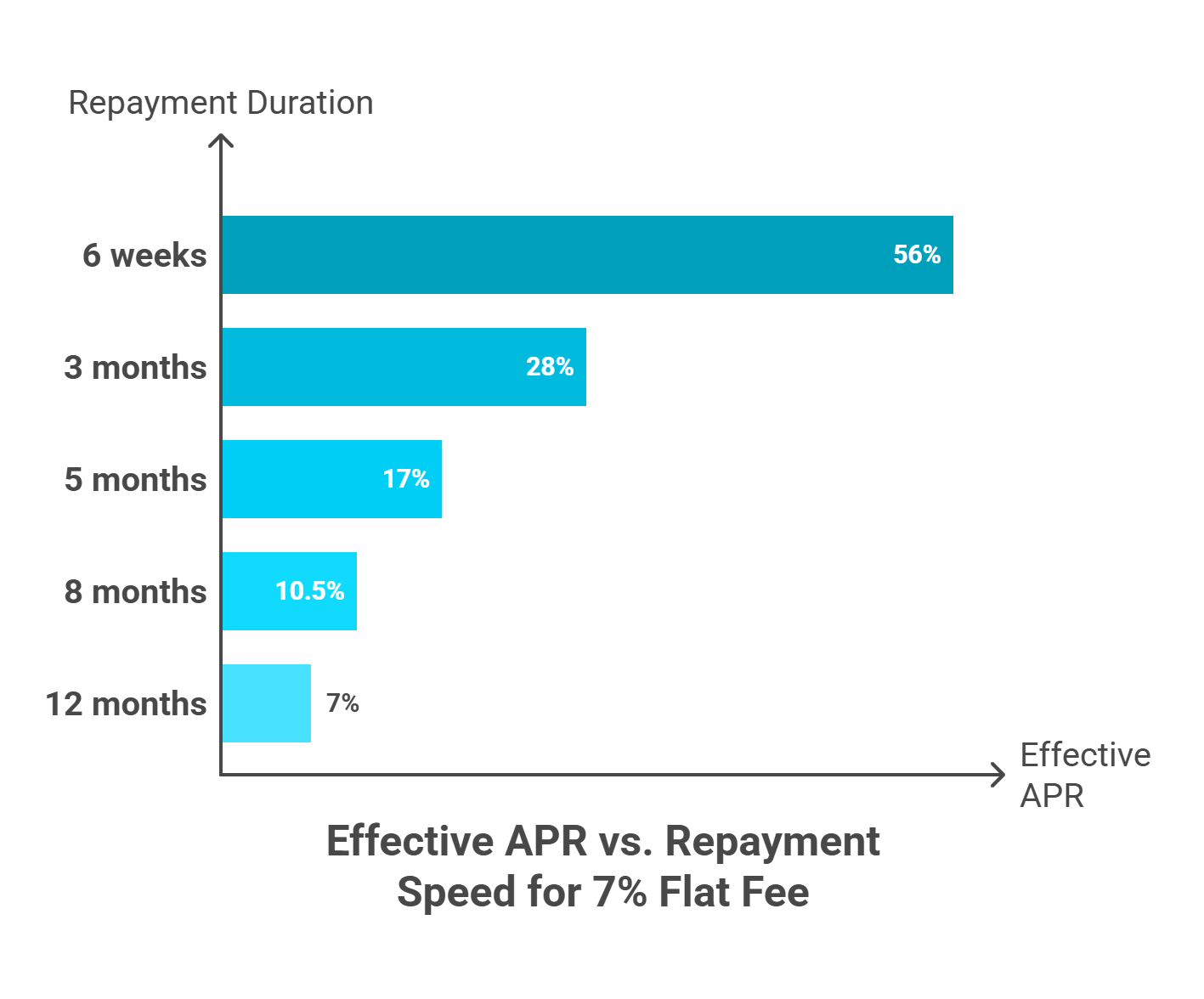

A "7% flat fee" on a €50K advance sounds harmless. But if you repay in 3 months, that's ~28% annualized. If your revenue spikes and you repay in 6 weeks, you're looking at 56%+ effective APR. The flat fee is marketing; the APR is reality.

2. Does the contract include a weekly minimum repayment floor?

Many contracts advertise "flexible repayment tied to revenue" but bury a minimum weekly debit that overrides the percentage during slow months. Ask: "If my revenue drops to zero next week, what gets debited?"

3. Does the provider file a UCC-1 lien, and what assets does it cover?

A blanket UCC lien covers all business assets, not just the funded amount. It blocks access to other financing and gives the provider priority claims. One merchant discovered 17 "horrible, unacceptable clauses" in Wayflyer's contract, including the right to redirect Shopify payouts.

4. What are the default trigger definitions?

Can the provider call the full remaining balance "at discretion"? Some contracts allow default declarations for subjective reasons, including anything they believe you said that wasn't fully correct, in their opinion.

Factor in auto-debits plus your cash conversion cycle. If inventory takes 75 days to convert and debits start Day 1, you'll service debt from existing cash flow for over two months before the funded inventory generates a single euro.

⚠️ The Fine Print Most Founders Skip

6. What is the lien removal process and timeline after payoff?

Providers have been reported sitting on UCC filings for months after balances reach zero, blocking subsequent financing relationships.

7. Do refunded orders trigger a clawback on revenue share already paid?

You paid 12% on a €200 sale. The customer returns it. Does the provider return their €24? In most contracts, no.

8. Is the revenue share applied to gross or net revenue?

Gross includes returns, chargebacks, and shipping fees. Net excludes them. The difference on a €100K/month brand with 8% return rates = €800/month in unnecessary repayment.

9. Is there an early repayment penalty or fee?

Rare but present at select providers. If your revenue spikes and you repay quickly, some contracts charge an additional fee, penalizing success.

10. Do you have a secondary funding relationship in case this provider changes terms mid-contract?

Multiple merchants across Wayflyer, Clearco, and Uncapped report having terms changed, funding slashed, or renewals denied without warning, leaving businesses stranded during critical growth phases.

✅ Score Interpretation

RBF Due Diligence Score Interpretation

Score

Assessment

Action

8 to 10 ✓

Thorough due diligence complete

Proceed with confidence

5 to 7 ✓

Significant blind spots remain

⚠️ Pause and investigate before signing

0 to 4 ✓

Contract not fully understood

❌ Do not sign until every item is resolved

How Luca AI Covers the Gaps

Luca AI answers every unchecked item automatically, calculating effective APR from your real revenue data, modeling post-funding cash position across 180 days, and surfacing contract red flags before you commit. The checklist becomes a single conversation: ask Luca "Model this RBF offer against my current data" and get every answer in one response. No spreadsheets. No guesswork. No discovering the UCC lien three weeks after signing.

Q10: Is Revenue-Based Financing Right for Your Ecommerce Business, Or Is There a Better Model? [toc=Is RBF Right for You]

After reading this guide, you know more about RBF than 95% of founders who sign these contracts. But the deeper question isn't "Is RBF good or bad?" It's "Am I making this capital decision with enough intelligence?" The ecommerce funding landscape offers real options (RBF, MCA, lines of credit, equity), but the decision infrastructure is broken. Founders choose based on who approves fastest, not what fits best.

The Structural Problem With "Capital Without Context"

Traditional RBF providers offer capital without intelligence. They don't tell you whether the investment the capital funds will generate enough return to cover the repayment cost. They don't model your cash conversion cycle. They don't warn you when a funding offer will create more drag than growth.

You get money, but not the understanding of whether you should take it, how much you actually need, or when in your operating cycle the capital produces the highest return. Every merchant review in this article points to the same root cause: founders signed because they needed speed, not because they had clarity.

"Clearco vendor financing is a great opportunity to fund inventory purchases, but it comes with 3 material flaws: (1) You immediately start paying off the entire balance even if you have only drawn down a small component. At times you might have paid back more than you have drawn!" -Scott Trustpilot Verified Review

"Their salespeople are sleazy. Never trust somebody that defers to their team when they make promises or pretend to build a relationship with you." -M Trustpilot Verified Review

✅ When RBF Is the Right Fit

You have a specific, time-bound growth initiative (Q4 inventory, proven campaign scaling)

Your cash conversion cycle is shorter than the expected repayment period

You've modeled the auto-debit impact on your daily operating cash

You need speed (24 to 72 hours) and can't wait for bank approval timelines

You want to retain 100% equity

❌ When RBF Is the Wrong Fit

You're using capital to cover operating losses, not fund growth

Your inventory conversion cycle exceeds 90 days and the repayment starts immediately

You can't afford 10 to 15% of daily revenue being auto-debited without cutting ad spend or operations

You haven't calculated the effective APR at your revenue trajectory

You're stacking a second RBF on top of an existing one

Before signing any RBF agreement, run through these four decision gates. Two "STOP" answers mean RBF isn't your best option right now.

The Next Evolution: Intelligence-Led Capital

The shift happening in ecommerce funding isn't about cheaper capital or faster approvals, it's about capital paired with intelligence. A system that can reason: "This campaign is showing 4.2x ROAS, your inventory can support a 40% scale-up, and here's €30K at terms that net you positive cash flow in 45 days." Intelligence that identifies the opportunity AND capital that funds it, in one motion.

Luca AI was built for exactly this. Not just analytics. Not just capital. The synthesis of both, an AI Co-Founder that reasons across your commerce, marketing, and financial data to surface the right capital at the right moment with full visibility into the downstream impact. Intelligence without capital is advice. Capital without intelligence is risk. Luca AI eliminates both gaps.

Q11: Revenue-Based Financing for Ecommerce, Frequently Asked Questions [toc=RBF FAQ]

Is revenue-based financing a loan?

Technically, it depends on the provider's legal structure. True RBF is typically structured as a revenue-sharing agreement, not a traditional loan, meaning it may not be subject to the same consumer lending regulations. However, some providers (particularly MCAs like Shopify Capital) structure the advance as a purchase of future receivables. The distinction matters for your legal protections: loans carry regulatory safeguards around disclosure and interest rate caps; revenue purchases often don't.

Does RBF affect your credit score?

Most RBF providers do not run hard credit checks during underwriting, they rely on platform data (Shopify, Stripe, Amazon Seller Central) instead. However, if a provider files a UCC-1 lien, it appears on your business credit profile and can affect your ability to secure other financing. If you default, some providers reserve the right to report to credit bureaus.

What happens if my revenue drops to zero?

In a true RBF structure, your repayment drops to zero because it's a percentage of revenue. In practice, many contracts include weekly minimum repayment floors that override the percentage. Read the fine print: "flexible repayment" may only flex upward. Ask your provider explicitly: "If I generate €0 next week, what gets debited from my account?"

Can I use RBF capital for anything?

Most providers don't restrict how you deploy the funds, inventory, ad spend, hiring, operations, or bridge financing are all common. However, some providers (like 8fig) structure capital specifically for supply chain and inventory use cases, with disbursements tied to your procurement cycle rather than a single lump sum.

How fast can I get funded?

Timelines range from same-day (Luca AI, Shopify Capital for pre-approved merchants) to 3 to 5 business days (8fig, traditional bank-adjacent providers). Most dedicated RBF providers fund within 24 to 72 hours after connecting your revenue platforms.

Can I repay early without penalty?

Most providers allow early repayment without penalty, you simply hit the repayment cap faster. However, verify this in your contract. A small number of providers charge early repayment fees or require a minimum holding period. Early repayment also means your effective APR is higher, not lower, because you've held the capital for a shorter period while paying the same flat fee.

What's the difference between RBF and a merchant cash advance?

RBF charges a fixed percentage of daily revenue with a repayment cap. MCAs purchase future receivables at a factor rate (e.g., 1.2x to 1.5x) with often-fixed daily debits. MCAs are technically not loans and carry fewer regulatory protections. Shopify Capital and Amazon Lending are MCAs, not RBF, despite often being marketed alongside RBF providers.

What minimum revenue do I need to qualify?

Most providers require €10K to €50K+ in monthly revenue and 6+ months of trading history. Luca AI starts at €10K monthly revenue. Platform-native options like Shopify Capital are invitation-only based on Shopify's internal algorithms, with no publicly stated minimum.

Can I stack multiple RBF agreements?

Technically possible, but dangerous. Combined auto-debits from two providers can consume 20 to 30% of daily revenue. UCC lien priority becomes a legal complexity, the first provider's lien takes precedence, and the second provider may require the first lien to be released before funding. Multiple merchants report being trapped by exactly this dynamic.

Q12: Making the Shift: From Capital Guesswork to Intelligence-Led Growth [toc=Intelligence-Led Growth]

The ecommerce funding landscape in 2026 is at an inflection point. The global revenue-based financing market, valued at $901M in 2019, is projected to reach $42.3 billion by 2027, a 61.8% CAGR that reflects how quickly founders are moving away from traditional bank financing. But the rapid growth of RBF has also exposed a fundamental gap: capital is getting faster, but the intelligence behind capital decisions hasn't kept pace.

The Gap Between Speed and Strategy

Every provider in this guide, Wayflyer, Clearco, Uncapped, 8fig, Shopify Capital, has optimized for one variable: speed to fund. And speed matters. When a DTC brand identifies a winning Q4 campaign and needs €50K for inventory within 48 hours, bank timelines are structurally incompatible with that opportunity.

But speed without strategy creates its own category of damage. Merchants accept oversized advances because bigger feels safer. They don't model repayment against their cash conversion cycle. They discover UCC liens, weekly floors, and discretionary default clauses three weeks into repayment. The reviews across 148 verified merchant experiences in this article tell a consistent story: the problem isn't access to capital, it's the absence of intelligence around that capital.

The ecommerce funding landscape's structural problem isn't access to capital. It's the absence of intelligence around that capital. 148 verified merchant reviews in this article point to the same root cause.

"After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute. This caused significant disruption to our operations and cash flow." -Geoff Brand Trustpilot Verified Review

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M. Then they cut it again to $350K." -Xin Shui Trustpilot Verified Review

What the Next Generation of Ecommerce Capital Looks Like

The next evolution isn't cheaper RBF or faster approvals. It's the convergence of real-time business intelligence with capital deployment, a system that doesn't just offer money but understands whether you should take it, how much you actually need, and precisely when in your operating cycle it produces the highest return.

✅ Dynamic pricing that adjusts with your real-time business health, not a 90-day-old snapshot

✅ Pre-funding cash flow modeling that shows your daily cash position for 180 days before you sign

✅ Same-day capital deployment starting at €10K with no personal guarantees and no UCC blanket liens

✅ Optimal capital sizing, recommending €50K when you need €50K, not €200K that generates fees on idle capital

✅ Revenue-aligned repayment that genuinely flexes with sales volume, no weekly minimums, no discretionary default clauses

Intelligence without capital is advice. Capital without intelligence is risk. Luca AI is the first platform built to eliminate both gaps, giving ecommerce founders the confidence to deploy capital knowing exactly where it leads.

FAQ's

What is the true cost of revenue-based financing for ecommerce businesses?

We find that the true cost of revenue-based financing is almost always higher than the advertised flat fee suggests. A provider quoting a 7% flat fee on a $50K advance appears affordable, but when we calculate the effective APR based on actual repayment speed, the picture changes dramatically.

3-month repayment: That 7% flat fee translates to roughly 28% annualized.

6-week repayment (revenue spike): The effective APR can exceed 56%.

Gross vs. net revenue share: If repayment is calculated on gross revenue (including returns, chargebacks, and shipping fees), an ecommerce brand doing $100K/month with 8% return rates overpays by approximately $800/month.

We recommend every founder calculate the effective APR at their current revenue trajectory, not just accept the marketing-friendly flat fee. Tools like Luca AI's financial management capabilities can model this automatically against your real revenue data, surfacing the actual cost before you sign. The flat fee is what providers advertise. The APR is what you actually pay.

What are the most common contract red flags ecommerce founders miss in RBF agreements?

We have analyzed verified merchant reviews across Wayflyer, Clearco, Uncapped, and 8fig, and the most damaging contract terms are consistently the ones founders skip during due diligence. The recurring blind spots fall into five categories.

Blanket UCC-1 liens: These cover all business assets, not just the funded amount, and block access to other financing. Some providers retain the lien for months after payoff.

Weekly minimum repayment floors: Contracts advertise flexible repayment tied to revenue but bury a fixed weekly debit that overrides the percentage during slow months.

Discretionary default triggers: Some agreements allow the provider to call the full remaining balance for subjective reasons, including anything they believe you stated that was not fully accurate.

No refund clawback: If a customer returns a product, the provider typically does not return the revenue share already collected on that sale.

Mid-contract term changes: Multiple merchants report having terms changed, funding slashed, or renewals denied without warning.

We built Luca AI to surface these red flags automatically before you commit, so no founder signs with dangerous blind spots.

How do the top ecommerce RBF providers compare on fees, speed, and contract terms?

We have mapped the leading RBF and MCA providers across the key dimensions that matter to ecommerce founders. The differences are significant enough to impact your bottom line by thousands of dollars per funding cycle.

Wayflyer: Funds within 24 to 72 hours, fees typically 2% to 8%, requires UCC-1 lien, minimum $20K monthly revenue. Strong for inventory funding but operates as a black box with limited visibility into downstream cash impact.

Clearco: Vendor financing model, 6% to 12% fees, disbursements tied to supplier payments. Merchants report starting repayment before goods arrive or capital is fully drawn.

8fig: Supply-chain-specific funding with staged disbursements, but multiple merchants report bait-and-switch on agreed rates and cycles being pulled mid-contract.

Shopify Capital: Invitation-only MCA (not true RBF), flat fee 1% to 17.7%, repayment as percentage of daily sales. Fast but no transparency on eligibility criteria.

We designed our provider comparison framework to help founders evaluate these options against their specific cash conversion cycle, revenue trajectory, and working capital needs rather than choosing based on who approves fastest.

When should an ecommerce business avoid revenue-based financing entirely?

We believe knowing when NOT to take RBF is more valuable than knowing when to take it. Revenue-based financing creates the most damage when founders use it as a lifeline rather than a growth lever. There are five clear signals that RBF is the wrong fit for your situation.

Covering operating losses: If capital is plugging a profitability gap rather than funding a proven growth initiative, RBF accelerates the bleed.

Long inventory conversion cycles: If your inventory takes 90+ days to convert and auto-debits start Day 1, you will service debt from existing cash flow for months before funded inventory generates any return.

Stacking multiple RBF agreements: Combined auto-debits from two providers can consume 20% to 30% of daily revenue, creating a cash flow death spiral.

No effective APR calculation: If you have not modeled the true annualized cost at your revenue trajectory, you are signing blind.

Cannot absorb 10% to 15% daily deductions: If auto-debits force you to cut ad spend or operations, the capital creates more drag than growth.

We recommend using cash flow forecasting tools to model your 90-day post-funding position before accepting any offer. The best capital decision is sometimes no capital at all.

What is the difference between revenue-based financing and a merchant cash advance for ecommerce?

We see this distinction confused constantly, and the difference has real implications for your legal protections and repayment experience. Revenue-based financing and merchant cash advances are structurally different products despite often being marketed interchangeably.

RBF (Revenue-Based Financing): Charges a fixed percentage of daily or monthly revenue with a defined repayment cap. Repayment genuinely flexes with sales volume. Typically structured as a revenue-sharing agreement.

MCA (Merchant Cash Advance): Purchases future receivables at a factor rate (e.g., 1.2x to 1.5x) with often-fixed daily debits. MCAs are technically not loans and carry fewer regulatory protections around disclosure and interest rate caps.

Key examples: Shopify Capital and Amazon Lending are MCAs, not RBF, despite being marketed alongside RBF providers. Wayflyer and Uncapped offer true RBF structures.

The distinction matters because loans carry regulatory safeguards that revenue purchases often do not. We help founders at Luca AI understand exactly which structure they are signing and model the downstream cash impact of each, so the legal and financial implications are clear before you commit.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.svg)

.svg)

.png)

.png)

.png)

.png)

.svg)

.webp)

.png)