10 Best Alternative Lenders for Ecommerce in 2026 (Compared by Fees, Speed & Eligibility)

14

mins read

TL;DR

We compared 10 alternative lenders across fees, speed, eligibility, platform integration, and capital intelligence to help ecommerce founders choose.

Ecommerce-specific lenders like Wayflyer, Clearco, and SellersFi use sales data for underwriting, while OnDeck, Bluevine, and Fundbox treat you like any offline SMB.

Platform-embedded capital from Shopify, Amazon, and PayPal offers zero-friction funding but locks you into a single channel with no cross-platform visibility.

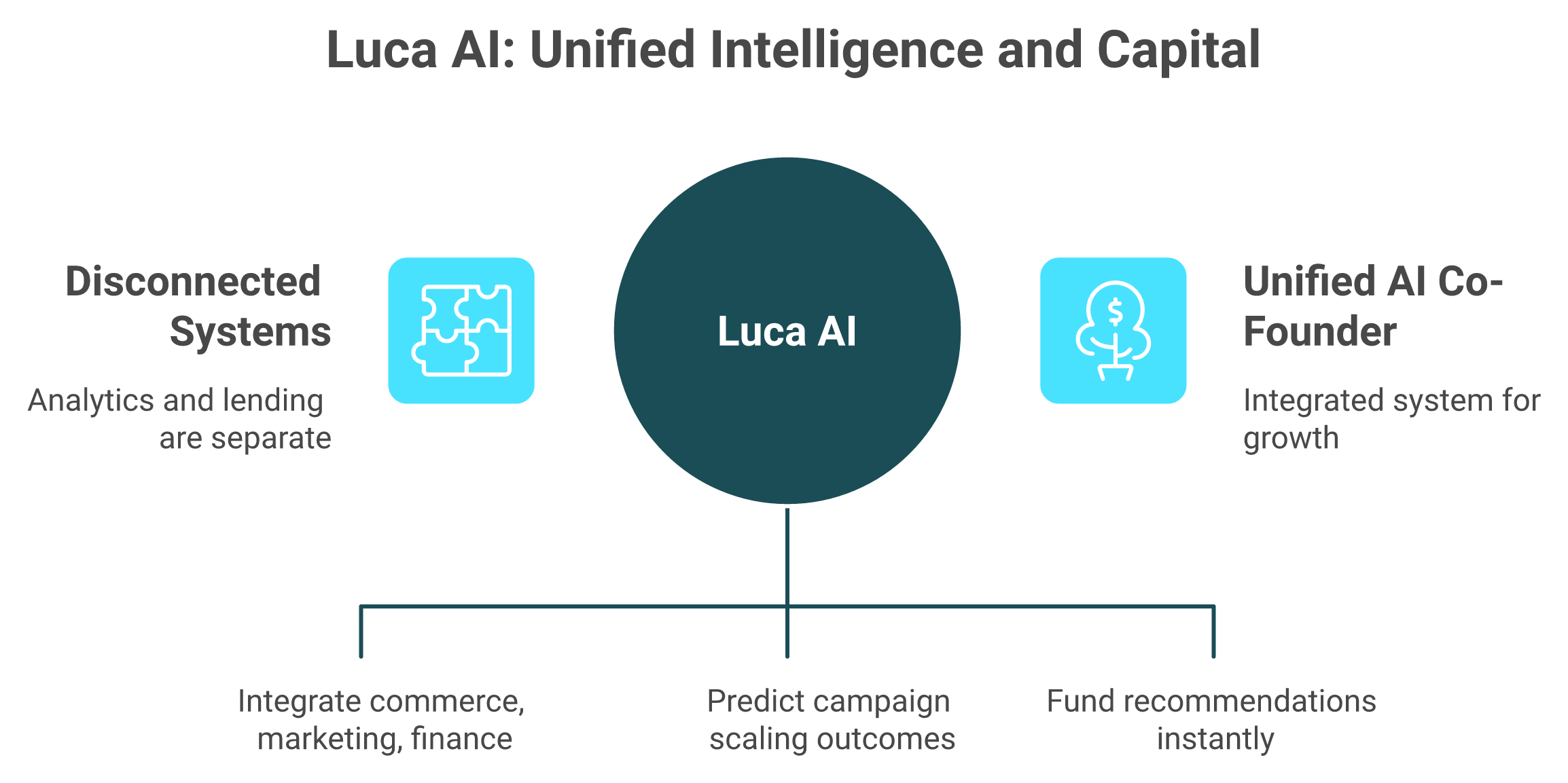

Luca AI is the only platform that combines business intelligence with embedded capital, modeling downstream cash impact before deploying funding in one system.

True cost matters more than advertised rates: a 7% flat fee can outperform a 6.2% interest rate depending on repayment structure and early payoff terms.

Q1. What Are the 10 Best Alternative Lenders for E-commerce in 2026? [toc=10 Best Ecommerce Lenders]

Alternative lenders exist because traditional banks were not built for e-commerce. With 80%+ of online seller loan applications rejected due to lack of physical collateral, short operating histories, and seasonal revenue swings, alternative lenders stepped in, using real-time sales data, marketplace performance, and revenue velocity for underwriting instead. The global alternative lending market hit $489 billion in 2025 and is projected to reach $556 billion in 2026, growing at 13.8% CAGR, with e-commerce-driven credit demand cited as a primary growth driver. Here are the 10 best alternative lenders for e-commerce in 2026.

Term loans up to $250K, LOC up to $200K, fast 1-day funding

General SMBs needing speed over ecommerce-specific features

APR from 29.9% + possible origination fee

Bluevine ⭐⭐⭐

Business LOC up to $250K, weekly/monthly repayment, simple draw process

Established businesses ($120K+ revenue) needing revolving capital

Interest starting at 6.2%

Fundbox ⭐⭐⭐

Business LOC up to $250K, lowest credit barrier (600), 12–52 week terms

Newer businesses or owners with limited credit history

Weekly fee from 4.66% (12-week) to 8.99% (52-week)

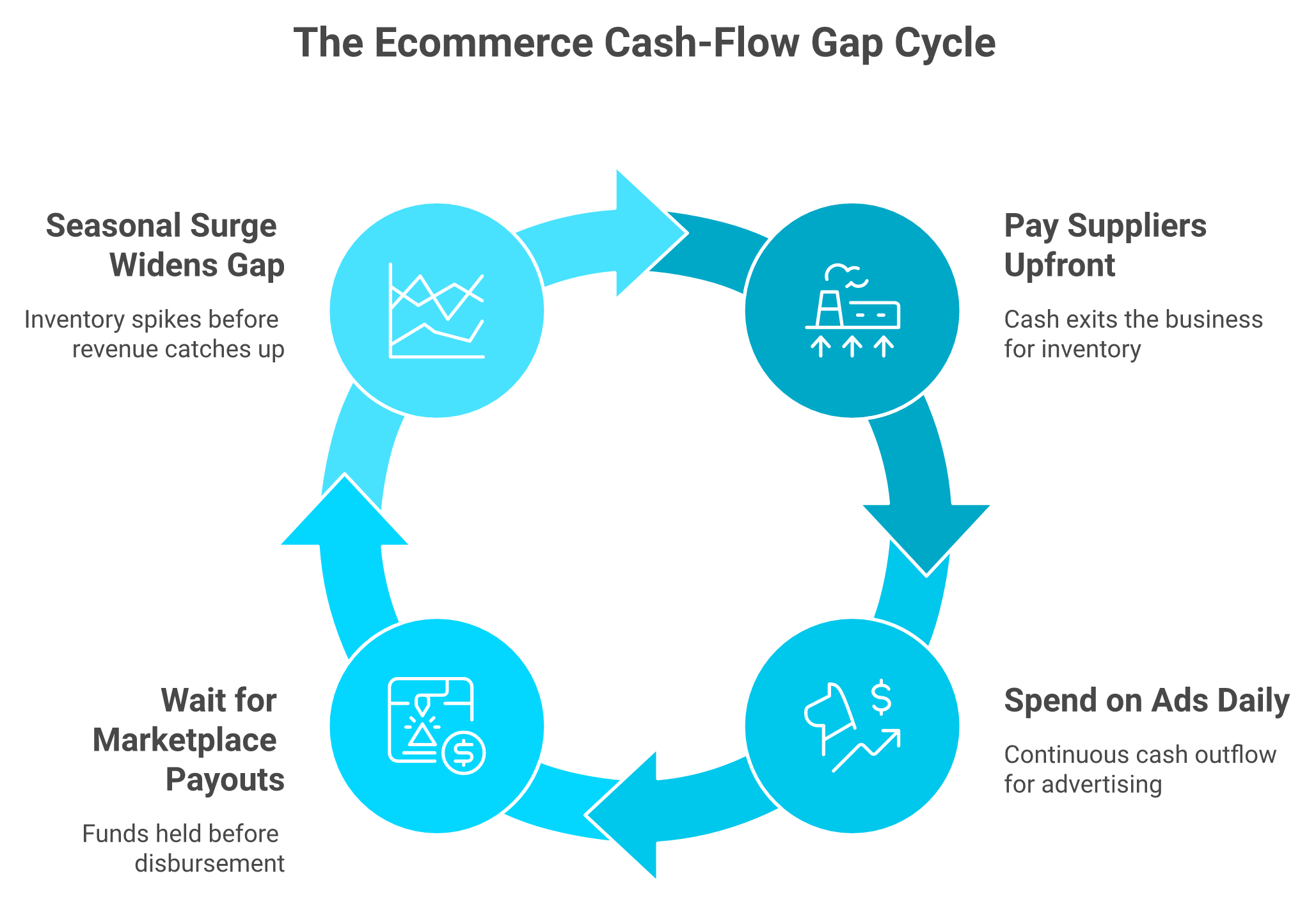

⏰ Understanding the Ecommerce Cash-Flow Gap

Before diving into each lender, it helps to understand why ecommerce businesses need alternative capital in the first place. The core problem is a timing mismatch: you pay suppliers upfront (often 30–90 days before selling), spend on ads daily, but receive marketplace payouts on a 14–21 day delay from Amazon or a 2–3 day cycle from Shopify. This gap widens during seasonal surges when inventory needs spike but revenue has not yet caught up.

Alternative lenders differ from traditional bank loans across four critical dimensions:

Speed: Hours or days vs. 6–8 weeks for bank approvals

Collateral: Sales data and marketplace performance vs. physical assets or real estate

Eligibility: Revenue-based underwriting vs. credit-score-gated applications

Repayment: Percentage of daily/weekly sales (flexes with revenue) vs. fixed monthly installments regardless of performance

The ecommerce cash-flow trap is a timing mismatch: suppliers demand payment months before marketplace payouts arrive, creating a perpetual working capital gap that alternative lenders exist to fill.

💰 Financing Types Represented on This List

Financing Models Explained

Financing Model

How It Works

Lenders on This List

Revenue-Based Financing (RBF)

Advance repaid as a % of future sales until a fixed fee is paid

Wayflyer, Clearco

Merchant Cash Advance (MCA)

Lump sum × factor rate, repaid via daily/weekly sales deductions

Shopify Capital, Clearco

Line of Credit (LOC)

Revolving draw up to a limit, interest only on drawn amounts

OnDeck, Bluevine, Fundbox, SellersFi

Platform-Embedded Capital

Native financing within a marketplace ecosystem, invite-based

Shopify Capital, Amazon Lending, PayPal Working Capital

AI-Integrated Capital

Intelligence layer identifies the opportunity, embedded capital funds it instantly

Adjacent options not profiled here but worth noting: SBA loans (low rates but 60–90 day approval timelines), equity financing (dilutive), inventory financing (collateral-based, suited for large PO cycles), invoice factoring (B2B-specific), crowdfunding, and government grants.

🏆 1. Luca AI

✅ Why Did We Choose This Tool?

Full disclosure: I'm Eric Bidinger, founder of Luca AI, and yes, we're listed first. But not because I wrote this article. Luca AI is first because it's the only platform on this list that doesn't just give you capital; it tells you whether you should take it, models the downstream impact, and funds the move in one system. Every other lender on this list solves half the problem. We built Luca to solve both halves: the intelligence gap and the capital gap. The AI Co-Founder model, unified Second Brain architecture, proactive intelligence, and Capital-as-a-Feature are not marketing buzzwords; they're architectural decisions that make Luca structurally different from every other entry here.

Luca AI's Lending intelligence dashboard serves as an AI Co-Founder for ecommerce, unifying sales analytics, ad spend modeling, inventory visibility, and embedded capital access in one conversational interface.

📊 Core Metrics

Funding Range: €10K–€500K+

Approval Speed: Same-day capital deployment

Fee Structure: Dynamic pricing based on real-time business health

Eligibility: Connected ecommerce store (Shopify, Amazon, or equivalent)

Platform Integrations: Shopify, Amazon, Meta, Google Ads, Xero, Stripe, 20+ data sources

✅ Solutions Offered

Unified Business Intelligence: Connects commerce, marketing, finance, and operations data into one reasoning layer via natural language conversation

Capital-as-a-Feature: Instant, dynamically-priced embedded capital that adjusts to current performance, not a 60-day-old snapshot

Proactive Intelligence: 24/7 automated scanning for risks (CAC spikes, inventory shortfalls) and opportunities (high-ROAS campaigns ready to scale)

Cross-Functional Scenario Modeling: Ask "If I take €50K and deploy to Meta, what's my cash position in 90 days?" and get an answer in seconds

Action-Oriented Execution: Pauses underperforming ads, generates forecasts, surfaces capital recommendations, all within one chat interface

😊 Best For

Scaling ecommerce brands (€1M–€100M revenue) that want a partner, not just a lender. Founders who need the system that identifies growth opportunities to also fund them instantly.

📋 Case Study

🔍 The Problem: A UK-based DTC skincare brand running €3.2M annual revenue across Shopify and Amazon was bleeding margin without visibility. Their Head of Growth saw strong ROAS on Meta campaigns but had no way to connect that data to cash runway, meaning winning campaigns were paused prematurely because the CFO couldn't confirm cash availability for inventory restocks.

💡 How Luca Helped: After a 10-minute onboarding connecting Shopify, Meta Ads, Stripe, and Xero, Luca's proactive intelligence surfaced a critical insight within 48 hours: their top-performing product-channel combination had a 4.1x ROAS with sufficient inventory runway to scale. Luca modeled the cash impact of a €40K capital injection and deployed funding same-day.

🏆 The Outcome: The brand scaled Meta spend by 65% on the identified campaign, generating €127K in incremental revenue over 6 weeks. Cash runway remained positive throughout because Luca had pre-modeled inventory needs and payout timing. Total time spent managing this across dashboards and lender applications before Luca: ~12 hours/week. After Luca: 25 minutes.

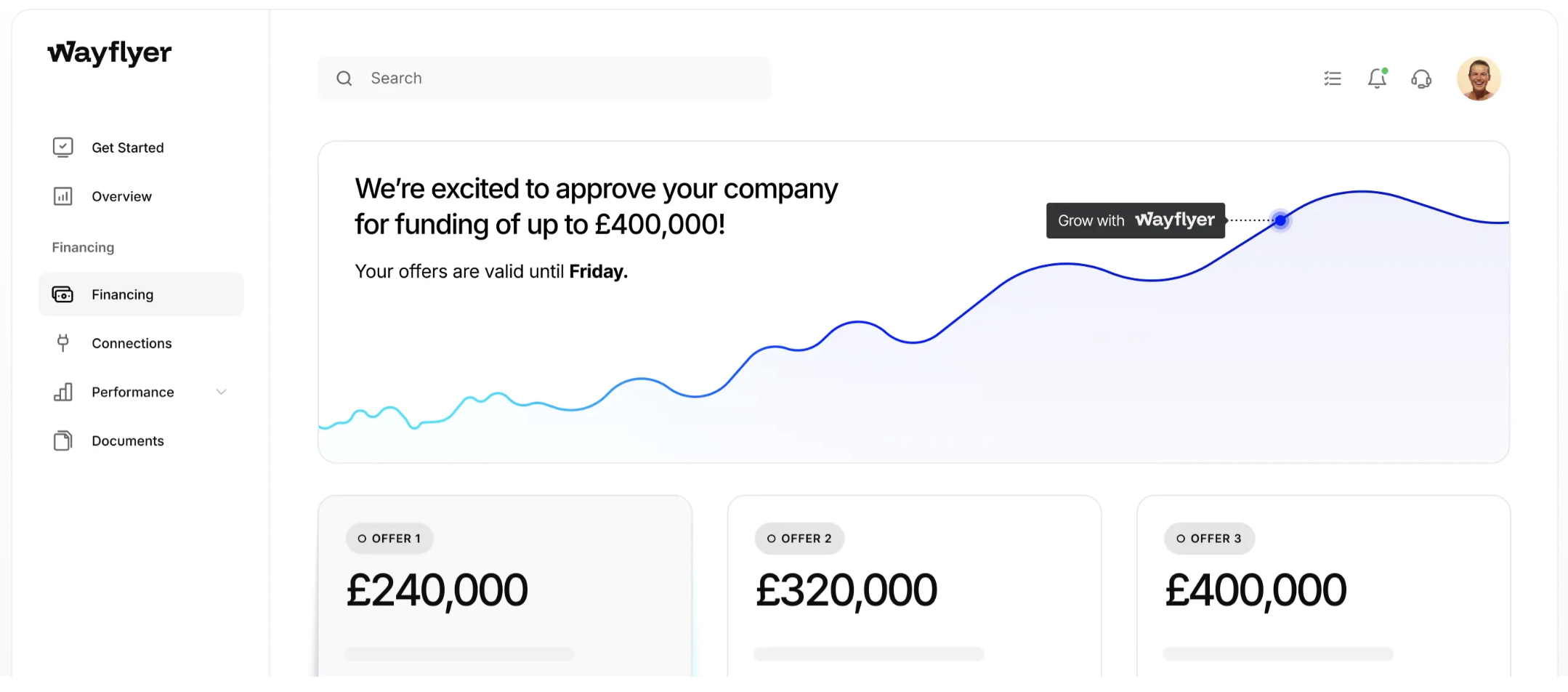

Wayflyer has deployed over $3.5 billion to ecommerce brands since launching in Dublin in 2019, making it one of the most established revenue-based financing providers in the space. Its flat-fee model (2–9%) consistently undercuts traditional MCA providers, and multi-currency support across USD, GBP, EUR, and AUD makes it a strong option for international sellers.

Wayflyer's capital dashboard presents tiered funding offers alongside a revenue performance chart — approval in 24 hours with 2–9% flat fees — but underwriting is based on trailing sales snapshots with no intelligence layer to model whether scaling that campaign will tank your cash runway.

📊 Core Metrics

Funding Range: $5K–$20M

Approval Speed: 24 hours (application to decision)

Fee Structure: 2–9% flat fee on funded amount (avg. ~7%)

Revenue-based financing with daily/weekly repayment as a percentage of sales

Multi-currency funding (USD, GBP, EUR, AUD) for international sellers

Data-driven underwriting via connected marketplace and payment accounts

Virtual card for immediate ad spend deployment

Growth analytics dashboard with basic performance insights

😊 Best For

International multi-marketplace sellers (Amazon + Shopify) doing $20K+/month who want the lowest flat-fee RBF available with fast approval.

⭐ Reviews

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues, this was incredibly disappointing and I am frustrated that no-one reached out to us sooner to advise." Joshua Hannan Wayflyer - Trustpilot Verified Review

"Worst bank agreement I have seen in 25 years of business. Dishonest sales team. Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC. They can deem you in default for any reason at their discretion." Zachary Piech Wayflyer - Trustpilot Verified Review

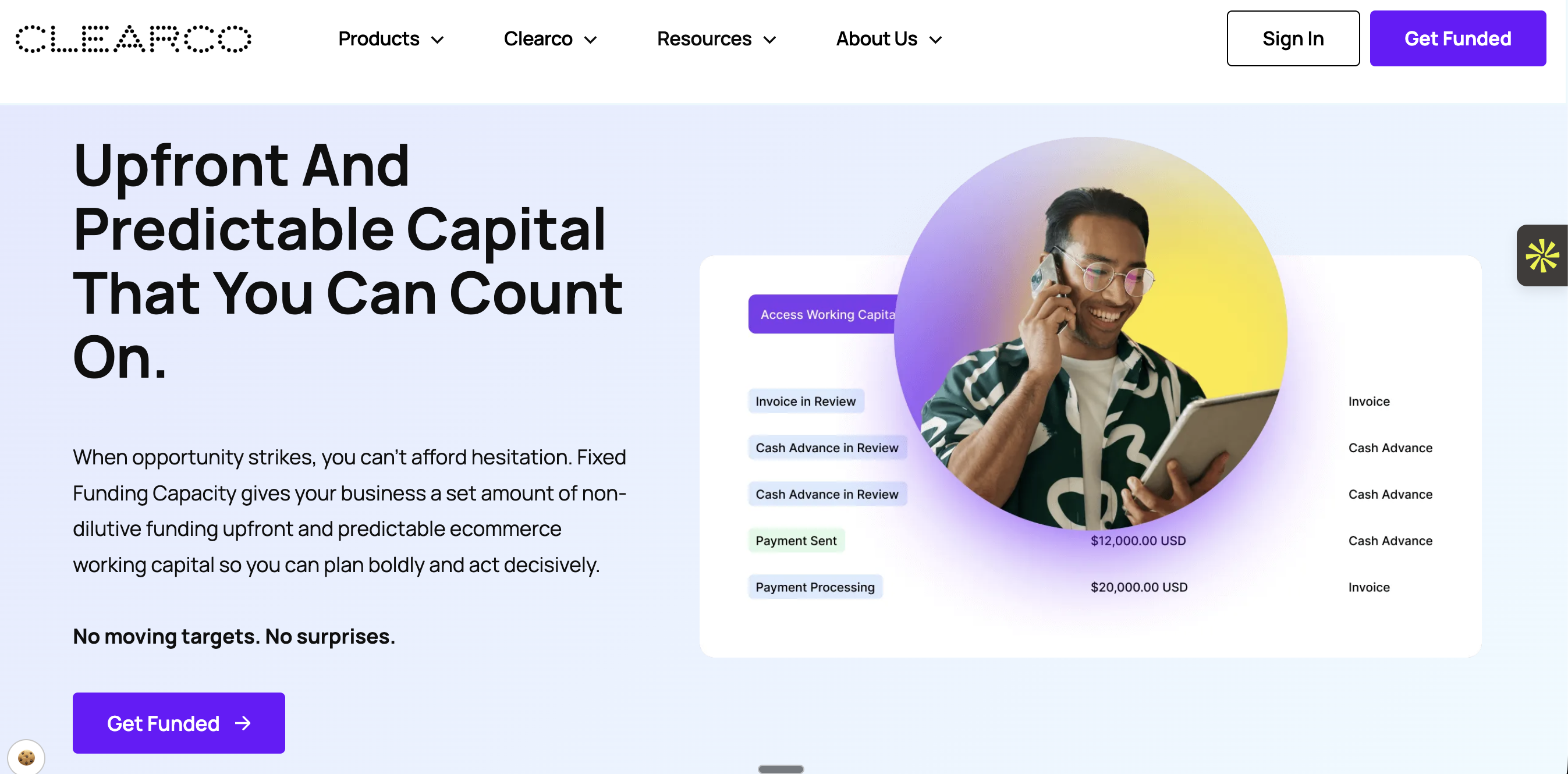

🏆 3. Clearco

✅ Why Did We Choose This Tool?

Clearco has invested over $3 billion into 10,000+ businesses since inception, establishing itself as one of the most recognized non-dilutive capital providers for DTC brands. Their dual product offering, cash advances and invoice funding, gives sellers flexibility, and capped weekly repayments prevent the accelerated payoff problem common with traditional MCAs.

Clearco's capital dashboard tracks cash advances, invoice funding, and payment status in one view — offering 6–12% flat-fee non-dilutive funding — but multiple borrowers report that repayment deductions exceeded contracted terms, inflating the effective cost well beyond the advertised rate.

📊 Core Metrics

Funding Range: Up to $2M+ (varies by qualification)

Eligibility: US-based ecommerce/SaaS, active online revenue

Platform Integrations: Shopify, Amazon, Stripe, Meta Ads, Google Ads

✅ Solutions Offered

Non-dilutive MCA cash advances with capped weekly repayments (max 30% of weekly revenue)

Invoice funding with prorated fee rebates for early payoff

Automated repayment via revenue-share integration

2-minute funding estimate before full application

No personal guarantee required

😊 Best For

US-based DTC brands that want fast, non-dilutive capital with capped weekly repayments and early repayment flexibility via invoice funding.

⭐ Reviews

"Clearco Lost Touch With Its Own Business Model. We worked with Clearco for a couple of years and had a great experience early on, especially with our original account manager, Derek. Unfortunately, things changed when our account was reassigned. Despite no change in our cash position or risk profile, and with strong recurring revenue, we started facing stricter cash-on-hand demands that made little sense." Melissa Clearco - Trustpilot Verified Review

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues. Just terrible, we wasted so much time on our side and their service was horrible after contract was signed and ACH was set up." Thomas Bishop Clearco - Trustpilot Verified Review

🏆 4. SellersFi

✅ Why Did We Choose This Tool?

SellersFi stands out for its deep Amazon integration, including a formal partnership with Amazon Lending offering eligible sellers credit lines up to $10 million, backed by a $300 million credit facility through Citi and Fasanara Capital. Their multi-product approach (working capital, inventory financing, invoice factoring) gives Amazon and Shopify sellers more flexibility than single-product RBF providers.

📊 Core Metrics

Funding Range: Up to $10M (Amazon Lending partnership)

Approval Speed: 48–72 hours

Fee Structure: Custom pricing based on risk assessment

Working capital funding with flexible repayment terms

Inventory financing for large purchase orders and seasonal stock-up

Invoice factoring for B2B ecommerce sellers

Amazon Lending partnership with credit lines up to $10M

Soft credit pull that does not impact personal credit score

😊 Best For

Amazon-heavy sellers doing $20K+/month who need multi-product financing flexibility and access to high-ceiling credit lines through the Amazon Lending partnership.

⭐ Reviews

"Working capital process was straightforward and funding came through in about 3 days. The Amazon integration made it seamless. However, the cost was not fully transparent upfront; I had to ask multiple times to get a clear picture of total fees." Ecommerce Seller SellersFi - Verified Review

"I was not asked when Uncapped took over the business I had with SellersFi. I never had a problem with SellersFi. But with Uncapped, a major one. My business banking is in a local credit union's hands, and Uncapped is incapable to connect to my bank account due to their flawed integration of Plaid's service." Volker Foerster SellersFi/Uncapped - Trustpilot Verified Review

🏆 5. Shopify Capital

✅ Why Did We Choose This Tool?

Shopify Capital eliminates the application process entirely; if you qualify, an offer appears in your Shopify admin dashboard. With Shopify having deployed over $5 billion in cumulative capital to merchants on its platform, the program has proven its model at massive scale. The zero-friction experience (no credit check, no paperwork, automatic repayment) makes it the lowest-effort financing option on this list.

Shopify Capital's funding dashboard surfaces pre-qualified offers directly inside your Shopify admin — zero application, zero credit check — but funds only Shopify-channel revenue while ignoring Amazon, wholesale, and every other sales channel.

📊 Core Metrics

Funding Range: $200–$2M (varies by merchant profile)

Eligibility: Invitation-only, must use Shopify Payments, active Shopify store

Platform Integrations: Shopify only

✅ Solutions Offered

Merchant cash advance with flat borrowing cost disclosed upfront

Automatic repayment as a fixed percentage of daily Shopify sales (10–17%)

No credit check or personal guarantee required

$0 payment on zero-sales days (true revenue-flex)

Pre-qualified offers appear directly in Shopify admin; no application needed

😊 Best For

Shopify-only merchants who want the simplest possible financing experience with zero application friction and fully automated repayment.

⭐ Reviews

"Good value for money? No. Quick money in a pinch? Yes." u/nkl7e6h, r/shopify Reddit Thread

"Our recent Shopify Capital $180,000 loan has been declined after we applied. This is strange to me, as since 2025 we've successfully been accepted for and repaid over $500k in capital loans." u/anonymous, r/shopify Reddit Thread

🏆 6. Amazon Lending

✅ Why Did We Choose This Tool?

Amazon Lending provides financing directly within the Amazon Seller Central ecosystem, leveraging first-party sales data that no external lender can access. Through partnerships with SellersFi, Parafin, Lendistry, and Marcus by Goldman Sachs, eligible sellers can access term loans, lines of credit, and merchant cash advances with minimal paperwork and automatic repayment through Amazon payouts.

Amazon Lending's capital dashboard lets invited sellers view loan summaries and funding allocation directly within the Amazon ecosystem — but access is invitation-only, limited to Amazon sales data, and offers zero intelligence on whether deploying that capital is the right strategic move.

📊 Core Metrics

Funding Range: $1K–$750K (up to $10M via SellersFi partnership)

Approval Speed: 1–5 business days (if invited)

Fee Structure: Varies by partner and product type

Eligibility: Invitation-only, 12+ months selling on Amazon, good account health

Platform Integrations: Amazon only

✅ Solutions Offered

Term loans, lines of credit, and MCA via four third-party lending partners

Underwriting based on Amazon's proprietary first-party sales data

Automatic repayment deducted from Amazon disbursements

No application required; pre-qualified offers appear in Seller Central

SellersFi partnership extends credit lines up to $10M for larger sellers

😊 Best For

Established Amazon sellers with 12+ months of sales history and strong account health who want the convenience of lending integrated directly into Seller Central.

⭐ Reviews

"Shopify and PayPal could look at my store and offer capital, however Onramp seemingly can just accuse me of not owning the commercial rights, and then refuse to acknowledge proper documentation when provided." Kenneth Onramp Funds (Amazon Lending Partner) - Trustpilot Verified Review

"I had the same thing happen to me in July. I believe it was an AI error." u/nwkrkhe, r/shopify Reddit Thread

🏆 7. PayPal Working Capital

✅ Why Did We Choose This Tool?

PayPal Working Capital offers one of the simplest financing models available: a single fixed fee, no credit check, and automatic repayment as a percentage of PayPal sales. For sellers with significant PayPal transaction volume, it's a frictionless option that requires no external applications or data connections.

📊 Core Metrics

Funding Range: Up to 35% of annual PayPal sales (typically $1K–$300K)

Approval Speed: Minutes (automated decision)

Fee Structure: Single fixed fee (varies by loan size, repayment %, and history)

Eligibility: PayPal Business account, 90+ days history, $15K–$20K annual PayPal sales

Platform Integrations: PayPal only

✅ Solutions Offered

Single fixed-fee loan with no interest accrual or compounding

Automatic repayment as a percentage of each PayPal sale

No credit check or personal guarantee

Flexible repayment percentage selection (10%, 15%, 20%, 25%, or 30%)

Instant eligibility check within PayPal dashboard

😊 Best For

Sellers with high PayPal transaction volume who want the simplest possible loan structure with no credit check and fully automated repayment.

⭐ Reviews

"PayPal Working Capital is legitimate and many businesses use it successfully. The automatic repayment from sales can work well for businesses with consistent revenue, but becomes problematic when sales fluctuate or slow down." u/npmef8a, r/loansforsmallbusiness Reddit Thread

"This product is expensive compared to traditional business loans and the automatic deduction can destroy cash flow during slow periods." u/nph277v, r/loansforsmallbusiness Reddit Thread

🏆 8. OnDeck Capital

✅ Why Did We Choose This Tool?

OnDeck has originated over $15 billion in small business financing, making it one of the largest and most established alternative lenders in the US. While not ecommerce-specific, its fast approval process (same-day decisions), high funding ceilings, and both term loan and line of credit products make it relevant for ecommerce operators with diversified revenue who need general-purpose working capital.

📊 Core Metrics

💰 Funding Range: Up to $250K (term loan), up to $200K (LOC)

📊 Fee Structure: APR from 29.9% (term loans), monthly interest on LOC

✅ Eligibility: 625+ credit score, $100K+ annual revenue, 1+ year in business

🔗 Platform Integrations: None (no ecommerce platform connections)

✅ Solutions Offered

Short-term business loans up to $250K with fixed daily or weekly payments

Revolving line of credit up to $200K with interest-only on drawn amounts

Same-day approval decisions via automated underwriting

Repeat borrower benefits with improved terms for returning customers

Dedicated customer support with phone access

😊 Best For

General SMBs (including ecommerce operators with offline/mixed revenue) needing fast capital without ecommerce-specific underwriting or marketplace integration.

⭐ Reviews

"Have mercy on me...went with OnDeck in a moment of need." u/anonymous, r/Businessloans Reddit Thread

🏆 9. Bluevine

✅ Why Did We Choose This Tool?

Bluevine offers one of the most competitive interest rates among alternative line-of-credit providers, starting at just 6.2%, significantly lower than OnDeck or Fundbox for qualified borrowers. Their revolving credit line structure is well-suited for ecommerce operators who need ongoing access to capital for recurring expenses like ad spend and inventory replenishment rather than one-time lump sums.

📊 Core Metrics

💰 Funding Range: Up to $250K (line of credit)

⏰ Approval Speed: Same-day decision, funding within 24 hours

📊 Fee Structure: Simple interest starting at 6.2%

✅ Eligibility: 625+ credit score, $120K+ annual revenue, 6+ months in business

🔗 Platform Integrations: None (no ecommerce platform connections)

Established businesses ($120K+ revenue) with decent credit (625+) who want the lowest-cost revolving capital among general alternative lenders for ongoing working capital needs.

⭐ Reviews

"I secured a $20k line of credit from Bluevine last year, and it proved essential for paying invoices. The funding arrived within two days, the interest rate was 7.5%, but the $15 wire fee was a nuisance." u/anonymous, r/loansforsmallbusiness Reddit Thread

🏆 10. Fundbox

✅ Why Did We Choose This Tool?

Fundbox has the lowest credit barrier on this list: a 600 minimum credit score and just $30K annual revenue, making it accessible to newer ecommerce businesses that would not qualify anywhere else. The no-origination-fee model and quick approval process make it a solid entry point for sellers who are still building their credit profile and revenue history.

📊 Fee Structure: Weekly fees starting at 4.66% (12-week) or 8.99% (52-week), est. APR 10.1%–79.8%

✅ Eligibility: 600+ credit score, $30K+ annual revenue, 6+ months in business

🔗 Platform Integrations: None (no ecommerce platform connections)

✅ Solutions Offered

Revolving line of credit up to $250K with weekly repayment

12-week and 52-week term options for different cash flow needs

No origination fees or prepayment penalties

Automated underwriting with minimal documentation

Integration with accounting software (QuickBooks, Xero) for faster approval

😊 Best For

Newer ecommerce businesses or founders with limited credit history (600+ score) who need accessible working capital with the lowest entry barriers among alternative lenders.

⭐ Reviews

"Traditional business lines of credit from banks often cost significantly less if you qualify." u/npn7lov, r/loansforsmallbusiness Reddit Thread

Luca AI is the only platform on this list that closes the loop between knowing and doing. Every other lender gives you capital. Luca gives you the intelligence to know whether you should take it, models what happens if you do, and deploys the funds, all in one conversation. Intelligence without capital is advice. Capital without intelligence is risk.

Q2. How Were These Ecommerce Lenders Evaluated and Scored? [toc=Evaluation Methodology]

Comparing alternative lenders for ecommerce is inherently complex because these providers operate on fundamentally different financing models. Revenue-based financing, merchant cash advances, lines of credit, term loans, and platform-embedded capital each carry different fee structures, eligibility criteria, and repayment mechanics. A standardized methodology ensures founders, CFOs, and Heads of Growth can make apples-to-apples comparisons despite these structural differences.

📊 The Five Evaluation Criteria

We scored all 10 lenders across five weighted criteria totaling 100%:

Evaluation Criteria and Weights

Criterion

Weight

What It Measures

Pricing Transparency and True Cost

25%

Published fee ranges, APR equivalents, hidden fee absence, and clarity of total cost before signing

Approval Speed and Funding Efficiency

20%

Application-to-funding time, documentation burden, and decision automation

Eligibility Accessibility

15%

Minimum barriers to entry: credit score floors, revenue thresholds, and time-in-business requirements

Platform Integration and Ecommerce Fit

20%

Marketplace connections (Shopify, Amazon, and PayPal), data-driven underwriting, and ecommerce-specific features

Capital Intelligence and Borrower Support

20%

Whether the lender provides business context, scenario modeling, proactive recommendations, or strategic guidance alongside funding

🔍 Criteria Definitions

💰 Pricing Transparency (25%): The single most impactful criterion for borrowers. Lenders with clearly published fee ranges, honest APR-equivalent disclosures, and no hidden charges score highest. Opaque pricing or fees that mask true cost (e.g., a "6% flat fee" that translates to 36%+ APR when factoring weekly repayment schedules) are penalized.

⏰ Approval Speed (20%): Ecommerce opportunities are time-sensitive. Q4 inventory windows, viral product moments, and ROAS spikes don't wait for 6-week bank approvals. Lenders offering same-day or automated decisions score higher than those requiring extensive documentation and manual underwriting.

✅ Eligibility Accessibility (15%): Lower credit score minimums, lower revenue thresholds, and shorter time-in-business requirements expand access for earlier-stage sellers. Invitation-only models (Shopify Capital, Amazon Lending) receive lower scores here because founders cannot proactively apply.

📊 Platform Integration (20%): Lenders that connect directly to Shopify, Amazon, Meta Ads, and payment processors for data-driven underwriting better serve ecommerce operators than those relying on bank statements and tax returns alone.

🧠 Capital Intelligence (20%): This criterion separates commodity capital from strategic capital. Most lenders score zero here; they provide money without business context, scenario modeling, or guidance on deployment. Only platforms that help founders understand whether and how to use capital score above baseline.

⭐ Star Rating Summary

Lender Star Ratings

Lender

Rating

Luca AI

⭐⭐⭐⭐⭐

Wayflyer

⭐⭐⭐⭐

Clearco

⭐⭐⭐⭐

SellersFi

⭐⭐⭐⭐

Shopify Capital

⭐⭐⭐⭐

Amazon Lending

⭐⭐⭐

PayPal Working Capital

⭐⭐⭐

OnDeck Capital

⭐⭐⭐

Bluevine

⭐⭐⭐

Fundbox

⭐⭐⭐

⚠️ A Note on Situational Fit

These ratings provide a general framework, not absolute rankings. The "best" lender depends entirely on your seller profile: stage, primary platform, geography, and capital need. An Amazon-only seller doing $500K/month may find SellersFi or Amazon Lending perfectly suited to their needs, while a multi-channel DTC founder operating across Shopify and wholesale channels might find platform-embedded options too limiting. The individual profiles throughout this article give the context needed to match each lender to the right seller archetype.

Q3. Luca AI: The AI Co-Founder That Funds What It Finds [toc=Luca AI Profile]

Every ecommerce founder knows the workflow: you spot an opportunity in one tool, then open a separate application to fund it. By the time capital arrives, days or sometimes weeks later, the scaling window has closed, the inventory is gone, or the ROAS has shifted. The ecommerce cash-flow gap isn't just a funding problem. It's an intelligence problem disguised as a capital one.

❌ The Broken Status Quo

Traditional alternative lenders like Wayflyer and Clearco offer capital without intelligence. They underwrite based on trailing 90-day revenue snapshots, meaning the capital offer you receive today reflects your business health two months ago, not your current trajectory. They can't tell you whether scaling that Meta campaign will tank your Q4 cash runway. They can't model inventory implications. They fund, they collect, and they move on.

On the other side, analytics tools like Triple Whale and GA4 show you the opportunity but can't fund it. They display ROAS, flag creative fatigue, and surface high-performing cohorts, but the moment you want to act, you're back to manual processes: exporting data, building a case, submitting a separate lending application, and waiting.

"0 customer service whatsoever, I've done 2 loans with these people and can't get ahold of a real person." Anonymous Wayflyer - Trustpilot Verified Review

✅ The Synthesis Thesis

Intelligence without capital is advice. Capital without intelligence is risk. The AI Co-Founder model closes this gap: a unified system that reasons across commerce, marketing, finance, and operations, then acts on what it finds, including deploying capital instantly when the math supports it.

We built Luca AI to be the system that identifies the opportunity, models the downstream impact, and funds the move, all inside a single conversational interface. No CSV exports, no separate applications, and no waiting.

The ecommerce industry's core problem isn't funding or analytics alone — it's that these two capabilities have never existed in one system. Luca AI's synthesis thesis unifies both.

📊 Luca AI at a Glance

Luca AI Overview

Dimension

Detail

Eligibility

Connected ecommerce store (Shopify, Amazon, or equivalent)

Fees

Dynamic, performance-based pricing reflecting real-time business health

Approval Speed

Same-day capital deployment

Platforms

Shopify, Amazon, Meta, Google Ads, Xero, Stripe, 20+ integrations

Repayment

Flexible, revenue-aligned

Intelligence Layer

✅ Cross-functional reasoning, proactive alerts, and scenario modeling

🧠 What Makes the AI Co-Founder Architecturally Different

✅ Unified Second Brain: Connects Shopify, Amazon, Meta, Xero, and Stripe into a single reasoning layer, not a dashboard aggregator, but a system that understands relationships between data points

✅ Cross-Functional Reasoning: Ask "If I scale this campaign 50%, will I have cash for inventory in August?" and receive an answer that spans marketing, finance, and operations in seconds

✅ Proactive Intelligence: Luca scans your business 24/7, surfacing risks (CAC inflation, creative fatigue, and inventory shortfalls) and opportunities (underpriced channels and high-LTV cohorts) without being asked

✅ Capital-as-a-Feature: When Luca recommends scaling a campaign, it can fund the move instantly, expressing confidence in its own analysis by putting capital behind its recommendation

✅ 10-Minute No-Code Setup: Natural language replaces SQL, dashboards, and analyst dependency

🏆 The Defining Use Case

While Wayflyer sends you a funding offer based on what your business looked like 60 days ago, Luca tells you whether you should take it, models the downstream cash impact across your entire operation, and funds the move, all in one conversation. The difference isn't incremental. It's architectural.

❌ Traditional lenders give you capital and hope you deploy it wisely.

❌ Traditional dashboards show you opportunities and hope you find capital.

✅ Luca AI identifies the opportunity, models the outcome, and funds it, in one system.

Stop renting disconnected tools. Start hiring an AI Co-Founder.

Q4. Ecommerce-Specific Lenders Compared: Wayflyer, Clearco, SellersFi, Shopify Capital, Amazon Lending and PayPal Working Capital [toc=Ecommerce Lender Profiles]

These six lenders are purpose-built for ecommerce sellers, using sales data and marketplace performance for underwriting rather than traditional credit metrics like bank statements and tax returns. They split into two distinct categories: Independent RBF providers (Wayflyer, Clearco, and SellersFi) that work across platforms, and Platform-Embedded capital (Shopify Capital, Amazon Lending, and PayPal Working Capital) tied to a single ecosystem.

💸 Independent Ecommerce Lenders

Wayflyer

Wayflyer has deployed over $3.5 billion to ecommerce brands since 2019, offering revenue-based financing at 2–9% flat fees with multi-currency support across USD, GBP, EUR, and AUD. Approval takes 24 hours, with repayment structured as 10–15% of daily sales. Minimum eligibility requires $20K/month revenue and 6+ months trading history.

✅ Pros: Competitive fee range, multi-marketplace support, virtual card for immediate ad spend, and international reach (US/UK/EU/AU)

❌ Cons: $20K/month minimum excludes smaller sellers, no intelligence layer, and multiple sellers report inconsistent underwriting and poor post-funding communication

"Our experience with Wayflyer has been extremely disappointing and professionally damaging. After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute." Geoff Brand Wayflyer - Trustpilot Verified Review

"Company loves to lie unfortunately. They gave our firm a 90,000 loan in June. At the time, they mentioned that once we paid off 50% of the loan, we would be eligible for additional financing so we can continue scaling. That was one big lie." Adam Zackman Wayflyer - Trustpilot Verified Review

Clearco

Clearco provides MCA cash advances and invoice funding at 6–12% flat fees, with capped weekly repayments (max 30% of weekly revenue) and prorated fee rebates for early payoff. Approval takes 24 hours with a 2-minute initial funding estimate. Primarily US-focused, with no minimum credit score requirement.

✅ Pros: No minimum credit score, 2-minute initial estimate, early repayment rebate structure, and capped weekly repayments

❌ Cons: Higher fee ceiling than Wayflyer, limited to US-based businesses, and extensive negative feedback on customer service and operational reliability

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

"Unresponsive. We used to get funding through them in 2020. Then they just disappeared. Pretty expensive product at 35-40% APR. Even worse support. 6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months." Julian Fernau Clearco - Trustpilot Verified Review

SellersFi

SellersFi offers working capital, inventory financing, and invoice factoring with a formal Amazon Lending partnership providing credit lines up to $10 million, backed by a $300M credit facility through Citi and Fasanara Capital. Approval takes 48–72 hours with a soft credit pull. Minimum eligibility requires $20K/month revenue and 6+ months operating history.

✅ Pros: Multi-product financing flexibility, Amazon Lending partnership for high-ceiling credit, soft credit pull protects personal score, and Shopify and Walmart support

❌ Cons: Limited fee transparency, mixed communication feedback, and acquisition by Uncapped has caused service disruption for some users

"I wasn't asked when Uncapped took over the business I had with SellersFi. I never had a problem with SellersFi. But with Uncapped, a major one. My business banking is in a local credit union's hands, and Uncapped is incapable to connect to my bank account due to their flawed integration of Plaid's service." Volker Foerster SellersFi - Trustpilot Verified Review

🏦 Platform-Embedded Lenders

Shopify Capital

Ecommerce lenders split into two camps: independent RBF providers with cross-platform reach but no intelligence, and platform-embedded capital with zero-friction access but single-ecosystem lock-in.

Shopify Capital operates on an invitation-only basis; if you qualify, an offer appears in your Shopify admin with zero application required. Factor rates range from 1.10–1.17, with automatic repayment as a fixed percentage (10–17%) of daily Shopify sales. Funding arrives in 2–5 business days. No credit check, no personal guarantee, and $0 payment on zero-sales days.

✅ Pros: Zero application friction, flat fee upfront, $0 on slow days, and no credit check

❌ Cons: Invitation-only with no transparency on selection criteria, Shopify-only (can't fund Amazon or wholesale operations), non-negotiable terms, and multiple merchants report unexplained rejections after years of successful borrowing

"Our recent Shopify Capital $180,000 loan has been declined after we applied. This is strange to me, as since 2025 we've successfully been accepted for and repaid over $500k in capital loans." u/anonymous, r/shopify Reddit Thread

"Good value for money? No. Quick money in a pinch? Yes." u/nkl7e6h, r/shopify Reddit Thread

Amazon Lending

Amazon Lending provides financing through third-party partners (SellersFi, Parafin, Lendistry, and Marcus by Goldman Sachs), offering term loans, lines of credit, and MCAs to eligible sellers within Seller Central. Funding ranges from $1K–$750K (up to $10M via SellersFi), with 1–5 day disbursement for invited sellers. Requires 12+ months selling history and good account health.

✅ Pros: No paperwork, fast if invited, underwriting based on Amazon's proprietary first-party data, and automatic repayment from payouts

❌ Cons: Zero control over invite timing, non-negotiable terms, Amazon-only ecosystem, no transparency on selection algorithm, and sellers cannot proactively apply

"Shopify and PayPal could look at my store and offer capital, however Onramp [Amazon Lending partner] seemingly can just accuse me of not owning the commercial rights, and then refuse to acknowledge proper documentation when provided." Kenneth Amazon Lending/Onramp - Trustpilot Verified Review

PayPal Working Capital

PayPal Working Capital offers a single fixed-fee loan based on annual PayPal sales volume, with automatic repayment as a percentage of each PayPal transaction. No credit check required. Eligibility starts at 90+ days account history and $15K–$20K annual PayPal sales. Approval is instant and automated.

✅ Pros: Simplest fee structure (single fixed fee, no compounding), no credit check, instant automated decision, and flexible repayment percentage selection

❌ Cons: Capped at 35% of annual PayPal sales (limiting for fast-growth sellers), PayPal-only ecosystem, and loan size meaningless if most revenue runs through Shopify or Amazon

"PayPal Working Capital is legitimate and many businesses use it successfully. The automatic repayment from sales can work well for businesses with consistent revenue, but becomes problematic when sales fluctuate or slow down." u/npmef8a, r/loansforsmallbusiness Reddit Thread

"This product is expensive compared to traditional business loans and the automatic deduction can destroy cash flow during slow periods." u/nph277v, r/loansforsmallbusiness Reddit Thread

📊 Head-to-Head Comparison

Ecommerce-Specific Lenders Comparison

Dimension

Wayflyer

Clearco

SellersFi

Shopify Capital

Amazon Lending

PayPal Working Capital

Fee Range

2–9% flat

6–12% flat

Custom

Factor 1.10–1.17

Varies by partner

Single fixed fee

Approval Speed

24 hours

24 hours

48–72 hours

2–5 days (if invited)

1–5 days (if invited)

Minutes

Min Revenue

$20K/month

Active online revenue

$20K/month

Invitation-based

Invitation-based

$15K–$20K/year PayPal

Credit Check

No hard pull

No

Soft pull

None

None

None

Shopify

✅

✅

✅

✅

❌

❌

Amazon

✅

❌

✅

❌

✅

❌

Geographic Reach

US, UK, EU, AU

US

US, Global (via Amazon)

US, CA, UK, AU

US

US (primary)

Repayment Model

% of daily sales

Capped weekly deductions

Flexible terms

% of daily Shopify sales

Auto-deducted from payouts

% of PayPal sales

Early Repayment Benefit

No rebate

Prorated fee rebate

Varies

No rebate

No rebate

No (fixed fee)

Intelligence Layer

❌

❌

❌

❌

❌

❌

⚠️ The Lock-In Risk

Platform-embedded capital (Shopify Capital, Amazon Lending, and PayPal Working Capital) is ideal for single-channel sellers who live entirely within one ecosystem. But for multi-marketplace brands selling across Shopify, Amazon, and wholesale, these options create a dangerous blind spot: they fund one channel while ignoring the rest of your operation.

Independent RBF providers (Wayflyer, Clearco, and SellersFi) offer broader reach but still lack intelligence; they fund based on revenue history without understanding whether deploying that capital is the right strategic move. For sellers operating across 2+ platforms who need both context and capital, Luca AI is architecturally designed to see the full picture: connecting every channel, modeling the cross-functional impact, and funding the opportunity in the same system.

Q5. Can General Business Lenders Like OnDeck, Bluevine, and Fundbox Work for Ecommerce? [toc=General Business Lenders]

Yes, but with significant limitations. OnDeck, Bluevine, and Fundbox are reliable alternative lenders for general small business working capital, but none were built for ecommerce. They don't connect to Shopify, Amazon, or any marketplace. They don't underwrite based on sales velocity, ROAS, or inventory turnover. They evaluate your business the same way they'd evaluate a plumber or a dentist: bank statements, credit score, and time in business. For ecommerce founders who also have offline revenue or need general-purpose capital that isn't tied to marketplace performance, these lenders can work. For pure-play online sellers, the fit is structurally incomplete.

📊 Head-to-Head: OnDeck vs. Bluevine vs. Fundbox

OnDeck vs. Bluevine vs. Fundbox Comparison

Dimension

OnDeck

Bluevine

Fundbox

Products

Term loans + LOC

LOC (revolving)

LOC (revolving)

Max Amount

$400K (term) / $200K (LOC)

$250K

$250K

APR Range

35%–99%

14%–95%

10.1%–79.8% (effective)

Min Credit Score

625

625

600

Min Revenue

$100K/year

$120K/year

$30K/year

Min Time in Business

12 months

12 months

6 months

Repayment

Daily/weekly (term), weekly/monthly (LOC)

Weekly or monthly

Weekly (12 or 52 weeks)

Ecommerce Integrations

❌ None

❌ None

❌ None

Funding Speed

Same-day

Same-day

Next business day

✅ Where Each Lender Fits

OnDeck: Best for established SMBs ($100K+ revenue) needing fast term loans up to $400K. Highest APRs on this list (avg. 56% per NerdWallet), but same-day funding and flexible qualification make it useful for emergencies.

Bluevine: Competitive starting rates (7.80% simple interest) and the option for monthly repayment make it the cheapest general lender for qualified borrowers (625+ credit, $120K+ revenue). Over $16 billion in working capital deployed to 900,000+ businesses.

Fundbox: Lowest barrier to entry: 600 credit score, $30K annual revenue, and 6 months in business. Ideal for newer businesses that can't qualify anywhere else, but weekly fee structures can compound quickly.

❌ The Ecommerce Gap

The critical limitation shared by all three: they evaluate ecommerce businesses using the same criteria as any offline SMB. They can't see your Shopify sales velocity, Amazon BSR trajectory, Meta campaign performance, or inventory turnover rates. This means:

❌ Underwriting ignores your strongest asset (marketplace sales data)

❌ No revenue-flex repayment: fixed schedules regardless of sales seasonality

❌ Capital deployment guidance is nonexistent

❌ Personal guarantees required across all three lenders

"I secured a $20k line of credit from Bluevine last year, and it proved essential for paying invoices. The funding arrived within two days, the interest rate was 7.5%, but the $15 wire fee was a nuisance." u/anonymous, r/loansforsmallbusiness Reddit Thread

"Have mercy on me...went with OnDeck in a moment of need." u/anonymous, r/Businessloans Reddit Thread

✅ Where Luca AI Bridges the Gap

For ecommerce founders, the difference is architectural. General lenders provide capital but cannot contextualize it within marketplace performance, ad spend ROI, or inventory cycles. Luca AI bridges this by connecting sales data, ad performance, and financial health into one intelligence layer that both qualifies you for capital and helps you deploy it where the math says it will generate the highest return, something no general-purpose lender can offer.

Q6. How Do You Choose the Right Lender? True Cost, Decision Framework and Red Flags [toc=Decision Framework]

With 10 alternative lenders available, choosing wrong means overpaying by thousands, waiting too long for capital, or getting locked into a single-platform ecosystem that can't scale with your business. Most founders pick based on whoever offers the highest amount or the lowest advertised rate, ignoring platform fit, true total cost, repayment impact on daily cash flow, and whether the lender actually understands their business model.

Instead of comparing all 10 lenders at once, this decision tree narrows your options in five questions based on your selling platform, revenue level, and whether you need intelligence alongside capital.

💰 True Cost Comparison: $50K Over 6 Months

Advertised rates are misleading. A "7% flat fee" and a "29.9% APR" sound dramatically different, but the dollars repaid on a $50K advance over 6 months tell the real story:

True Cost Comparison: $50K Over 6 Months

Lender

Fee Structure

Est. Total Repaid on $50K

True Cost

Bluevine

7.80% simple interest

~$51,950

💰 Lowest

Wayflyer

7% flat fee

~$53,500

💰 Low

Clearco

8% midpoint flat

~$54,000

💸 Moderate

SellersFi

Custom factor rate

~$54,500 (est.)

💸 Moderate

Fundbox

4.66% weekly fee (12-wk)

~$54,660

💸 Moderate

Shopify Capital

Factor 1.10–1.17

$55,000–$58,500

💸 Moderate to High

OnDeck

35%–99% APR + origination

~$57,500+

💸 High

PayPal WC

Single fixed fee

Varies by volume

💸 Varies

Amazon Lending

Varies by partner

Varies

💸 Varies

Luca AI

Dynamic, performance-based

Adjusts to real-time health

✅ Context-aware

⚠️ Key insight: Cheapest-looking isn't always cheapest. Flat fees don't reward early repayment (Wayflyer, Shopify Capital). APR models layer origination fees on top (OnDeck charges 0–4%). Weekly fee structures compound faster than they appear. Fundbox's "4.66%" weekly draw fee translates to 10.1–79.8% effective APR depending on term length.

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC. They can deem you in default for any reason at their discretion." Zachary Piech Wayflyer - Trustpilot Verified Review

"6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% to 4 months to 12 months to 36% APR. In the best case." Julian Fernau Clearco - Trustpilot Verified Review

✅ Where Luca AI Stands

For sellers who need someone to tell them IF they should take the capital, not just offer it, Luca AI is the only option that closes the loop. It models the downstream cash impact before you accept, recommends optimal deployment across channels, and dynamically prices based on real-time business health rather than a static application from 60 days ago. The system that identifies the opportunity funds it.

Q7. People Also Ask: Ecommerce Lending Trends, Tax Implications and Cross-Border Guidance for 2026 [toc=Trends and FAQs 2026]

⏰ Five Trends Reshaping Ecommerce Lending in 2026

The alternative lending landscape is evolving rapidly, driven by technology convergence and shifting borrower expectations:

AI-native underwriting replaces static credit models: Lenders increasingly use real-time sales velocity, campaign performance, and inventory turnover for risk assessment rather than 60-day-old bank statements and credit scores.

Embedded finance expands beyond Shopify: Capital is being natively integrated into TikTok Shop, Amazon, Walmart, and B2B commerce platforms. In 2026, financing stops being a downstream step and becomes a channel embedded at the point of need.

Dynamic pricing replaces flat fees: Cost adjusts to real-time business health rather than locking in a rate based on historical snapshots. Decision latency, how fast a lender can assess and fund, is becoming the new competitive metric.

Cross-border funding goes mainstream: Multi-geography sellers demand multi-currency capital solutions. Providers like Wayflyer (USD/GBP/EUR/AUD) are setting the baseline, but full cross-border intelligence remains nascent.

Intelligence converges with capital: The system that recommends the investment funds it. Analytics and financing are merging into unified platforms rather than operating as separate, non-communicating tools.

💰 Tax Implications by Financing Type

Tax treatment varies significantly across financing models. Consult a CPA for your specific situation, but here's the general framework:

Tax Treatment by Financing Type

Financing Type

Tax Treatment

Notes

Term loan interest

✅ Deductible as business expense

Must be used for legitimate business purposes

Line of credit interest

✅ Deductible as business expense

Only on drawn amounts

RBF fees

✅ Generally deductible

Record as interest/fee expense against liability

MCA payments

⚠️ Partially deductible

Technically a purchase of future receivables, not a loan; fee component may be deductible, consult CPA

Origination fees

✅ Amortizable over loan term

Cannot deduct full amount in year one

Flat fees (Shopify Capital, Wayflyer)

✅ Generally deductible

Record the fee portion separately from principal repayment

🌍 Cross-Border Availability

Lender Geographic Availability

Lender

US

UK

EU

APAC

Global

Luca AI

✅

✅

✅

✅

Expanding

Wayflyer

✅

✅

✅

✅ (AU)

-

Clearco

✅

-

-

-

-

SellersFi

✅

-

-

-

Via Amazon

Shopify Capital

✅

✅

-

✅ (AU)

-

Amazon Lending

✅

-

-

-

-

PayPal WC

✅

✅

-

✅ (AU)

-

OnDeck

✅

-

-

-

-

Bluevine

✅

-

-

-

-

Fundbox

✅

-

-

-

-

❓ Frequently Asked Questions

What is the best alternative lender for ecommerce?

It depends on your profile. For intelligence + capital in one system, Luca AI leads. For lowest flat-fee RBF, Wayflyer. For Shopify-only merchants, Shopify Capital offers zero-friction access.

How does revenue-based financing work for online sellers?

You receive a lump sum and repay it as a fixed percentage of daily or weekly sales. When sales are high, you repay faster. When sales dip, payments decrease automatically. Total repayment is the advance plus a flat fee (typically 2–12%).

Can I get ecommerce financing with bad credit?

Yes. Fundbox accepts credit scores as low as 600. Shopify Capital and PayPal Working Capital require no credit check at all. Platform-embedded lenders underwrite based on sales data, not personal credit.

Do alternative lenders require personal guarantees?

Most general lenders (OnDeck, Bluevine, and Fundbox) do require personal guarantees. Ecommerce-specific providers (Shopify Capital and Clearco) typically do not. Wayflyer's contract terms have been flagged by some borrowers for containing UCC filing provisions.

How fast can I get ecommerce business funding?

PayPal Working Capital offers instant automated decisions. Shopify Capital and Amazon Lending fund within 1–5 days if you're invited. Wayflyer and Clearco typically fund within 24 hours of application.

What's the difference between a merchant cash advance and a business loan?

An MCA is technically a purchase of your future sales, not a loan. It uses a factor rate (e.g., 1.15) instead of an interest rate, and repayment is deducted as a percentage of daily sales. A business loan carries an APR, fixed repayment schedule, and is regulated as a lending product.

✅ Where Luca AI Fits in the 2026 Landscape

Luca AI is built for this converged future: intelligence and capital architecturally unified, not retrofitted. As embedded finance expands and AI underwriting becomes standard, Luca represents the prototype of where the entire ecommerce lending industry is heading: a system that understands your business deeply enough to fund it intelligently. Every trend on this list, AI-native underwriting, dynamic pricing, embedded capital, and cross-functional intelligence, is already core to how Luca operates today.

FAQ's

What is revenue-based financing and how does it work for ecommerce sellers?

Revenue-based financing (RBF) is a funding model where you receive a lump sum and repay it as a fixed percentage of your daily or weekly sales until a predetermined total amount (advance plus flat fee) is paid back. Unlike traditional loans with fixed monthly installments, RBF flexes with your revenue: when sales spike during Q4 or a viral product moment, you repay faster; when sales dip in a slow period, your payments decrease automatically.

For ecommerce sellers, this model aligns repayment with actual business performance rather than arbitrary schedules. Providers like Wayflyer (2%–9% flat fee) and Clearco (6%–12% flat fee) are the most established RBF options on our list. However, RBF providers typically underwrite based on trailing 90-day revenue snapshots, meaning the offer you receive today reflects where your business was two months ago, not where it is now.

We built Luca AI's financial management layer to address this gap. Instead of funding based on stale data, Luca connects to your live sales channels, models the real-time cash impact of taking capital, and deploys funding only when the math supports it. The result is capital that is both flexible in repayment and intelligent in deployment.

Can I get ecommerce business funding with a low credit score or no credit check?

Yes. Several alternative lenders on our list require no credit check at all, and others accept scores as low as 600. Here is a quick breakdown of the most accessible options:

Shopify Capital: No credit check required. Invitation-only, but if you receive an offer, approval is automatic based entirely on your Shopify sales performance.

PayPal Working Capital: No credit check. Eligibility is based on your PayPal transaction history ($15K–$20K annual PayPal sales minimum).

Fundbox: Accepts credit scores as low as 600 with just $30K annual revenue and 6 months in business, making it the lowest barrier-to-entry lender on this list.

Clearco: No minimum credit score requirement. Underwriting is based on active online revenue rather than personal credit history.

The trade-off with low-barrier lenders is that fees can be higher, and platform-embedded options like Shopify Capital only fund one sales channel. For sellers who want a smarter approach to funding, we recommend connecting all your revenue channels so capital decisions are based on total business health, not just one platform's snapshot.

How do I calculate the true cost of an ecommerce loan or merchant cash advance?

Advertised rates are misleading. A "7% flat fee" and a "29.9% APR" sound dramatically different, but the total dollars repaid on a $50K advance over 6 months tell the real story. Here is why true cost calculation matters:

Flat-fee models (Wayflyer, Shopify Capital) charge a fixed percentage regardless of how quickly you repay. A 7% flat fee on $50K means you owe $53,500 whether you pay it back in 3 months or 6 months. There is no early repayment benefit.

APR models (OnDeck, Bluevine) charge interest over time, so faster repayment actually saves money. However, origination fees (OnDeck charges 0%–4%) add hidden cost on top.

Weekly fee structures (Fundbox) compound faster than they appear. A "4.66%" weekly draw fee translates to 10.1%–79.8% effective APR depending on term length.

The key metric is total dollars repaid, not the advertised rate. We built cash flow forecasting directly into Luca AI so you can model the exact repayment impact on your runway before accepting any capital offer, from any lender, inside one conversation.

What is the fastest way to get funded as an ecommerce seller in 2026?

Speed varies dramatically across lenders. Here is the current funding timeline landscape for ecommerce sellers:

Minutes: PayPal Working Capital offers instant automated decisions with same-day funding for eligible PayPal Business accounts.

Same-day: Luca AI deploys capital same-day after connecting your ecommerce data sources. OnDeck and Bluevine also offer same-day decisions with next-day funding.

24 hours: Wayflyer and Clearco typically move from application to funding decision within one business day.

48–72 hours: SellersFi processes applications within 2–3 business days, including a soft credit pull.

2–5 days: Shopify Capital and Amazon Lending fund within this window, but only if you have already received an invitation.

The critical difference is not just speed of funding but speed of intelligent funding. Getting capital fast without knowing whether or how to deploy it creates risk, not opportunity. Our intelligence-capital thesis explains why the system that identifies the growth opportunity should also be the one that funds it, eliminating the lag between insight and action entirely.

Should I use Shopify Capital, Amazon Lending, or an independent lender for my ecommerce store?

It depends on how many sales channels you operate across and whether you need capital for your entire business or just one platform. Here is how we break it down:

Choose platform-embedded capital (Shopify Capital, Amazon Lending, PayPal Working Capital) if: You sell exclusively on one platform, you want zero-friction approval with no application, and you are comfortable with non-negotiable terms tied to that single ecosystem.

Choose independent RBF providers (Wayflyer, Clearco, SellersFi) if: You sell across multiple marketplaces, you want to compare fee structures, and you need capital that is not locked to one channel. Independent lenders offer broader reach but still fund based on historical revenue without strategic deployment guidance.

Choose Luca AI if: You operate across 2+ platforms and need both intelligence and capital in one system. Platform-embedded options create a blind spot by funding one channel while ignoring the rest. Independent lenders fund without context. Luca AI connects every channel, models the cross-functional cash impact, and funds the opportunity, all inside one conversation. For multi-marketplace sellers, that architectural difference determines whether capital accelerates growth or just adds debt.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.png)