Invoice Financing vs Factoring Explained: Side-by-Side Comparison With Real Examples

11

mins read

In this article

TL;DR

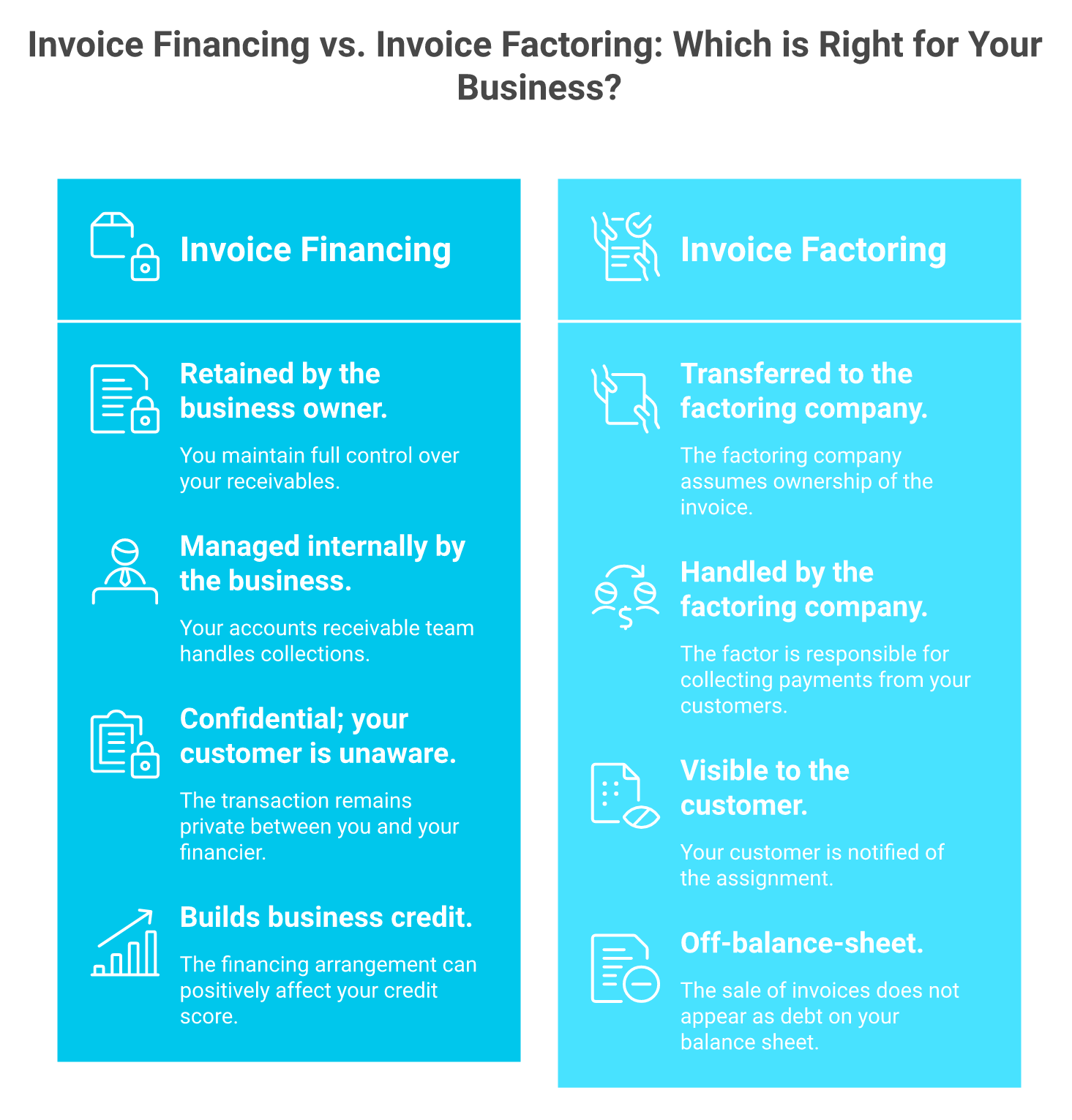

Invoice financing borrows against invoices (collateral); factoring sells them outright to a third party, creating fundamentally different ownership and collections structures. Financing charges interest on the drawn advance (10–35% APR); factoring fees apply to full invoice value (20–45% APR), making cost divergence accelerate with longer payment cycles. Factoring outsources collections and approves based on customer credit, making it accessible to startups; financing preserves confidentiality but requires 600+ credit scores and internal AR capacity. Recourse factoring (83.8% of U.S. volume) lets factors return unpaid invoices; non-recourse only covers insolvency, not disputes or slow payment. AI-native platforms like Luca AI introduce dynamic pricing that adjusts with real-time performance, deploying capital in minutes with no lock-in or personal guarantees.

Q1. What Is Invoice Financing and How Does It Work Step by Step? [toc=Invoice Financing Explained]

Invoice financing is a short-term borrowing arrangement where a business uses its unpaid B2B invoices as collateral to secure a loan or revolving credit line from a lender. The business retains full ownership of every invoice, and full responsibility for collecting payment from its customers. You may see this product referred to by several interchangeable names: invoice discounting, accounts receivable financing, or simply invoice finance. Regardless of the label, the core mechanism is identical: you borrow against money your customers already owe you, unlocking working capital without waiting 30, 60, or 90 days for them to pay.

The process follows a streamlined five-step sequence:

Apply and submit your accounts receivable ledger to a lender

Dual evaluation: the lender assesses your business creditworthiness and your customers' payment history

Receive an advance, typically 80 to 95% of the invoice face value, deposited within 24 to 72 hours

Collect payments normally: your customers pay you directly, completely unaware of the arrangement

Repay the advance: once the customer pays, you return the lender's advance plus interest and fees

💰 A Worked Dollar Example

Consider a $100,000 invoice with an 85% advance rate. You receive $85,000 upfront. Your customer pays the full $100,000 thirty days later. You repay the lender $85,000 plus approximately $1,275 in interest (at 1.5% monthly on the advance), keeping $13,725 in retained margin. The interest applies only to the drawn advance amount, not the full invoice face value, which is a critical cost distinction from factoring that directly impacts your effective borrowing rate.

Beyond the headline interest rate (typically 1 to 3% per month or 0.5 to 1.5% per week), several additional fees can layer into total cost:

Origination fees: 1 to 3% one-time at facility setup

Draw fees: a small per-advance processing charge each time you access the facility

Unused-line fees: 0.25 to 0.5% annually on undrawn facility capacity

Annualised APR typically falls between 10 and 35%, and total cost scales directly with how long your customer takes to pay, making payment velocity the single biggest lever on your effective borrowing cost.

⏰ Who Qualifies and How Quickly?

Lenders assess two dimensions simultaneously: your business's financial profile (revenue history, credit score, time in operation) and the credit quality of the customers listed on your invoices. Businesses with credit scores above 600, at least 12 to 24 months of operating history, and a base of commercially reliable customers qualify most easily. Most fintech lenders approve and fund within 24 to 72 hours, a dramatic improvement over the 6 to 8 week timelines typical of traditional bank credit facilities. Minimum invoice thresholds usually start at $10,000.

✅ The Confidentiality Advantage

The defining benefit of invoice financing is complete confidentiality. No notification letters, no payment redirection, no disruption to customer relationships. Your buyers never know the financing arrangement exists. For brands selling into relationship-sensitive channels, such as enterprise SaaS clients, premium retailers, and strategic wholesale partners, this invisibility is often the deciding factor.

But what if your own credit history is limited, or your team doesn't have the bandwidth to chase payments internally? That's exactly where invoice factoring enters, with a fundamentally different ownership model where invoices aren't pledged as collateral but sold outright to a third party.

Q2. What Is Invoice Factoring and Why Do Businesses Sell Their Invoices? [toc=Invoice Factoring Explained]

Invoice factoring is the outright sale of unpaid invoices to a third-party company, known as a "factor," at a discount. Unlike invoice financing, where the business borrows against receivables, factoring transfers legal ownership of the receivable to the factor. The factor advances 70 to 90% of the invoice face value, assumes responsibility for collecting payment directly from your end customer, and remits the remaining balance (minus their fee) once payment clears. This product also goes by accounts receivable factoring, debt factoring, or AR factoring. The fundamental distinction is structural: this is a sale of assets, not a loan.

The mechanic follows five steps, though the customer experience differs significantly from financing:

Submit invoices to the factoring company

Factor verifies the invoice and runs credit checks on your customer, not on your business

Receive an advance, 70 to 90% of the invoice value within 24 to 48 hours

Notice of Assignment (NOA): the factor notifies your customer to redirect payment directly to them

Reserve release: once the customer pays in full, the factor remits the remaining balance minus the factoring fee

💸 Whole-Ledger vs Spot Factoring

Not all factoring arrangements are identical. Whole-ledger factoring requires you to factor your entire accounts receivable portfolio, meaning every eligible invoice routes through the factor. This is the most common structure and typically offers lower per-invoice fees in the range of 1 to 3% per 30-day period.

Spot factoring (selective factoring) lets you choose individual invoices to factor on demand. Factor one large invoice this month, none the next, giving you maximum flexibility, but per-invoice fees run higher at 3 to 5%. Spot factoring is gaining rapid traction among DTC brands with seasonal revenue patterns and businesses that need only occasional cash flow acceleration.

⚠️ Customer Notification: The Key Trade-Off

The most debated element of factoring is customer visibility. Three notification models exist along a spectrum:

Disclosed (standard): Customer receives an NOA and pays the factor directly, operationally clean but introduces perception risk

Non-notification: The factor remains invisible; payments route through a lockbox. Rarer, more expensive, and typically reserved for larger facilities

Hybrid notification-only: Customer is informed of the assignment but continues paying the business, which forwards funds

As one experienced controller shared:

"The procedure was quite straightforward: I would send over a copy of all the invoices we were factoring along with a summary of the total amount. They would then deposit the funds into our account overnight. The associated fees were around 1.5% monthly." r/Accounting Reddit Thread

✅ Why Businesses Choose Factoring Despite the Cost

The appeal comes down to four drivers: outsourced collections eliminate internal AR overhead, immediate cash unlocks time-sensitive growth opportunities, the factor's credit analysis provides built-in bad-debt protection, and, most critically, approval depends on your customers' creditworthiness, not your own. This makes factoring uniquely accessible to startups, businesses with imperfect credit histories, and rapid-growth companies that traditional lenders routinely reject.

Q3. Invoice Financing vs Factoring: What Are the Key Differences? [toc=Key Differences Compared]

The core conceptual divide is simple: invoice financing means borrowing against your receivables; invoice factoring means selling your receivables. That single structural difference, collateral versus sale, cascades into every operational, financial, and relational dimension of the arrangement. The following comparison table captures all nine critical dimensions side by side.

The single structural fork between collateral and sale cascades into every operational, financial, and relational dimension of the arrangement.

Invoice Financing vs Invoice Factoring: 9-Dimension Comparison

Dimension

Invoice Financing

Invoice Factoring

Invoice Ownership

Retained by business (collateral)

Transferred to the factor (sold)

Collections Responsibility

Business collects payment internally

Factor manages all collections

Customer Notification

None, fully confidential

Notice of Assignment sent to customer

Advance Rate

80 to 95% of invoice value

70 to 90% of invoice value

Cost Structure

Interest on drawn advance (1 to 3%/month)

Flat fee on full invoice value (1 to 5%/30 days)

Typical Effective APR

10 to 35%

20 to 45%

Funding Speed

24 to 72 hours (revolving facility)

24 to 48 hours (per-invoice or per-batch)

Credit Evaluation Focus

Your business credit + customer quality

Primarily your customer's creditworthiness

Balance Sheet Treatment

Receivable stays as asset; advance as liability

Receivable removed; no new liability added

🔍 Ownership and Collections: The Cascading Divide

With financing, invoices remain on your balance sheet as collateral. You retain the receivable, you collect payment, and you bear the full risk if the customer pays late or defaults. With factoring, legal ownership transfers via an assignment agreement, and the factor's collections team takes over. This single structural difference dictates everything else: financing preserves confidentiality but requires internal AR capacity; factoring outsources collections but introduces customer visibility.

⭐ Credit Evaluation: Your Credit vs Your Customers' Credit

Financing lenders assess your business: credit score, revenue trajectory, and time in operation. Stronger businesses secure better rates. Factoring companies primarily evaluate your customers' payment reliability, because the factor is purchasing the right to collect from them. This is why factoring remains more accessible for startups and businesses with limited credit history: if your customers are creditworthy, you qualify regardless of your own balance sheet strength.

⏰ Funding Speed and Flexibility

Both options fund within 24 to 48 hours once approved. However, financing typically provides a revolving facility, allowing you to draw and repay repeatedly against your AR ledger as invoices cycle. Factoring funds on a per-invoice or per-batch basis, making it more episodic. Financing gives predictable, ongoing access to capital; factoring scales dynamically with invoice volume.

For global context: the worldwide factoring market reached 3.38 trillion euros in volume in 2023 according to FCI's Annual Review 2024, yet the Federal Reserve Small Business Credit Survey found that only 4% of small employer firms had applied for factoring, suggesting massive underutilisation driven largely by confusion about how factoring differs from other financing products. Closing that knowledge gap is precisely the purpose of this comparison.

Q4. How Much Does Each Option Really Cost? (Worked Examples With APR Calculator) [toc=Cost Comparison and APR]

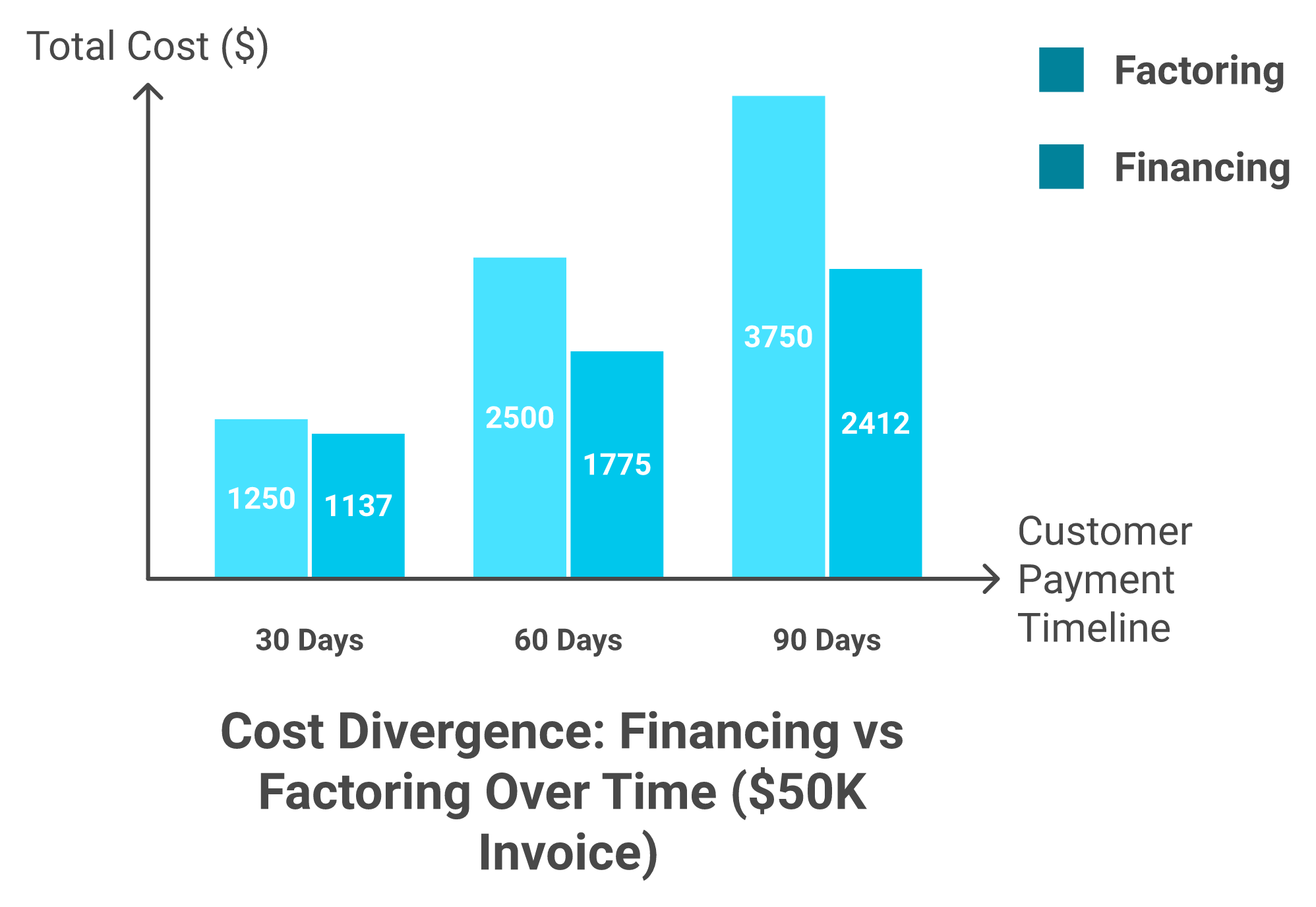

Cost is where the financing-versus-factoring decision gets concrete. Below is a transparent, apples-to-apples comparison using the same $50,000 invoice modelled across three customer payment timelines: 30, 60, and 90 days.

Base assumptions:

Financing terms: 1.5% monthly interest on the advance, 85% advance rate ($42,500 upfront), 1% origination fee ($500 one-time)

Factoring terms: 2.5% fee per 30-day period on the full invoice face value, 90% advance rate ($45,000 upfront)

Invoice Financing vs Factoring: Cost by Payment Timeline ($50K Invoice)

Customer Pays In

Financing Total Cost

Factoring Total Cost

Financing Effective APR

Factoring Effective APR

30 days

$637 interest + $500 origination = $1,137

$1,250

~18%

~30%

60 days

$1,275 + $500 = $1,775

$2,500

~18%

~30%

90 days

$1,912 + $500 = $2,412

$3,750

~18%

~30%

The cost divergence accelerates with time because factoring fees apply to the full invoice face value ($50,000), while financing interest accrues only on the drawn advance ($42,500). At 90 days, the factoring cost is 55% higher than financing for the same underlying invoice.

The cost gap between financing and factoring accelerates over time because factoring fees apply to the full invoice value while financing interest accrues only on the drawn advance.

💸 Hidden Fees That Inflate the Headline Rate

The table above captures core costs only. In practice, ancillary fees can add 15 to 30% to the total:

Factoring hidden costs:

Wire transfer fees: $25 to $50 per transfer

Due diligence fees: $300 to $500 upfront

Monthly minimum volume requirements: $10K to $50K (penalties if unmet)

Aging penalties: incremental fees for invoices past 60/90 days

Early termination penalties: 2 to 5% of facility value

Financing hidden costs:

Draw fees per advance request

Unused-line fees: 0.25 to 0.5% on undrawn capacity

Annual renewal fees

Personal guarantee requirements on some facilities

As one Reddit user evaluating factoring noted:

"A tiered pricing model is often employed, meaning that as the time an invoice remains unpaid increases, so does the fee. For instance, if an invoice is settled within 1 to 10 days, the charge might be 1%. However, if it takes 11 to 20 days for payment, the fee could rise to 2%." r/lowvoltage Reddit Thread

⚠️ Neither Option Is Categorically Cheaper

The "right" cost depends on three variables unique to your business:

Credit profile: Strong credit (600+) unlocks cheaper financing rates; weak credit makes factoring the only viable option

Payment velocity: If customers pay within 30 to 45 days, financing almost always wins on cost. At 60 to 90+ day cycles, factoring's outsourced collections can offset the higher fee

Collections capacity: The salary cost of an internal AR specialist ($45K to $65K/year) must be weighed against factoring's built-in collections service

The downloadable cost comparison calculator linked at the end of this article lets you input your own invoice amounts, advance rates, fee structures, and payment timelines to model your specific total cost under both options. For businesses looking for AI-powered cash flow forecasting to complement their financing strategy, platforms like Luca AI can model these scenarios dynamically based on your real-time unit economics and customer payment patterns.

Q5. What Are the Pros, Cons, and Customer Relationship Implications of Each? [toc=Pros, Cons and Relationships]

Choosing between invoice financing and factoring isn't just a cost calculation. It's a strategic decision about customer relationships, credit positioning, and operational capacity. Here's a balanced breakdown of the advantages and trade-offs for each product.

✅ Invoice Financing: Pros and Cons

Pros:

Full control over customer relationships and the collections process

Complete confidentiality: customers never learn about the financing arrangement

Flexible revolving access to capital that grows with your receivables ledger

Typically lower all-in cost for businesses with strong credit and fast-paying customers

Cons:

Collections burden stays internal, requiring dedicated AR staff or infrastructure

Stricter business credit requirements (600+ score, 12 to 24 months operating history)

Slower initial qualification for first-time applicants compared to factoring

Doesn't solve the problem if your customers are chronically slow payers

✅ Invoice Factoring: Pros and Cons

Pros:

Immediate cash flow acceleration within 24 to 48 hours of invoice submission

Outsourced collections reduce AR overhead and headcount needs

Funding capacity scales automatically as your revenue grows

Credit risk can transfer to the factor in non-recourse arrangements

Accessible to startups and businesses with limited credit history

Cons:

Customer notification via Notice of Assignment can feel intrusive

Potentially higher total cost, especially on long payment cycles

Vendor relationship disruption in confidentiality-sensitive industries

Contract lock-in risk with whole-ledger factoring requirements

Loss of direct customer payment intelligence and cash application data

⚠️ Customer Relationships: The Under-Discussed Factor

The reputational impact of factoring depends entirely on industry norms. In staffing, freight, and construction, factoring is so normalised that Notices of Assignment cause zero friction. As one recruiter shared:

"During my four years managing a staffing agency in California, we consistently factored our invoices without encountering any problems. Our competitors, who didn't use factoring, often struggled with cash shortages." u/Regal-30-, r/Recruitment Reddit Thread

In professional services, SaaS, and luxury DTC, however, customers receiving an NOA may interpret it as a signal of financial distress. If your top three customers represent 80%+ of revenue, protecting those relationships argues strongly for confidential invoice financing or non-notification factoring arrangements.

💰 Business Credit Score: A Hidden Divergence

Invoice financing appears as a credit facility on your business credit report. Timely repayment actively builds credit history. Factoring, structured as a sale rather than a loan, generally does not appear on credit reports and neither builds nor damages your score.

However, there's a critical caveat: most factoring companies file a UCC-1 lien on your receivables. As one business owner noted:

"UCC filings are visible to future lenders. It can impact your chances for loans and credit cards. Factoring companies are notorious for doing the UCC filings to keep you with them for long term." u/JDinSF, r/smallbusiness Reddit Thread

⭐ Quick Decision Framework

Choose financing when: you have a credit score above 600, relationship-sensitive customers, efficient internal collections, and a need for complete confidentiality.

Choose factoring when: you have poor or limited business credit, no internal AR team, are in rapid growth straining internal resources, or operate in an industry where factoring is normalised and expected. For e-commerce founders exploring additional working capital options beyond traditional invoice products, AI-native platforms offer a third path worth evaluating.

Q6. Recourse vs Non-Recourse Factoring: Who Bears the Risk if a Customer Doesn't Pay? [toc=Recourse vs Non-Recourse Risk]

Invoice financing is inherently full recourse. You borrowed against the invoice and must repay the lender regardless of whether your customer pays. The risk spectrum within factoring, however, is where the nuance lies. Recourse factoring, which accounted for 83.8% of all U.S. factoring transactions in 2020 according to the International Factoring Association's Annual Industry Survey, means the factor can "put back" unpaid invoices to your business after a defined period, typically 60 to 90 days of non-payment. You must buy the invoice back or replace it with a performing receivable. Non-recourse factoring means the factor absorbs the credit risk, but with a critical limitation that catches many businesses off guard: non-recourse coverage typically applies only to customer insolvency (bankruptcy), not to payment disputes, delivery disagreements, quality claims, or simple slow payment.

💸 The Cost Trade-Off, Quantified

Non-recourse factoring typically adds 1 to 2 percentage points to the factoring fee, for example, 4 to 5% per 30-day period versus 2 to 3% for recourse. For a business factoring $500K in monthly invoices, that premium translates to $5,000 to $10,000 per month, a significant margin impact for growth-stage brands managing tight margins. An alternative strategy is purchasing trade credit insurance (0.1 to 0.5% of receivables annually) alongside recourse factoring, which can deliver non-recourse-like bad-debt protection at a fraction of the cost while keeping factoring fees low.

⭐ Decision Guidance by Customer Profile

If your customers are large, creditworthy enterprises, such as government agencies, Fortune 500 retailers, and publicly traded companies, recourse factoring is usually sufficient. Default risk against these payers is negligible, and you avoid paying the non-recourse premium entirely. If you sell to SMBs, international buyers, or customers in volatile industries with unpredictable credit profiles, non-recourse factoring or a recourse-plus-insurance combination may justify the premium. In every case, verify the exact non-recourse coverage definition in your contract before signing. "Non-recourse" does not mean zero risk, and the gap between perception and contractual reality is where businesses get burned.

Q7. How Do Financing and Factoring Appear on Your Balance Sheet, and What Are the Tax Implications? [toc=Balance Sheet and Tax Impact]

How you record invoice financing versus factoring on your books fundamentally changes your financial statements, and can directly affect loan covenants, investor due diligence, debt capacity, and tax treatment. Under FASB ASC 860 (or IFRS 9 internationally), factoring arrangements structured as a "true sale" remove the receivable from the balance sheet entirely. Invoice financing keeps the receivable as an asset and adds a corresponding liability. The distinction matters far more than most founders realise.

Cash $90,000 + Factoring Fee Expense $3,000 + Due from Factor (reserve) $7,000

Accounts Receivable $100,000

Reserve release

Cash $7,000

Due from Factor $7,000

Net effect: The receivable disappears from the balance sheet entirely. No new liability is created. Receivables decrease; debt does not increase.

⚠️ Impact on Financial Ratios and Investor Readiness

Financial Ratio Impact: Financing vs Factoring

Ratio

Invoice Financing Impact

Invoice Factoring Impact

Current Ratio

❌ Decreases (new liability added)

✅ Can improve (no liability added)

Debt-to-Equity

❌ Increases

✅ Unchanged

Days Sales Outstanding

Unchanged

✅ Decreases (receivables removed)

Loan Covenant Risk

⚠️ May trigger restrictive covenants

✅ Typically covenant-neutral

For businesses preparing for fundraising or acquisition, factoring's off-balance-sheet treatment presents a cleaner capital structure. However, auditors increasingly scrutinise factoring for "true sale" vs "secured borrowing" classification under ASC 860. If recourse terms are too aggressive, the arrangement may be reclassified as a loan, negating the off-balance-sheet benefit entirely. Founders preparing for investor due diligence should consult resources on cash flow forecasting to model the downstream effects of their financing structure.

💰 Tax Treatment Differences

Factoring fees are typically deductible as a business expense (cost of sales or operating expense), reducing gross or operating margin. Financing interest is deductible as an interest expense, subject to Section 163(j) limitations for businesses exceeding $30M in gross receipts. The practical difference is where the deduction sits on your P&L: factoring fees appear above the operating income line; financing interest appears below it. This can affect EBITDA calculations and operating margin optics during investor presentations. Consult your CPA for entity-specific guidance.

Q8. Which Industries Benefit Most, and What Do Real Scenarios Look Like? [toc=Industry Scenarios and Use Cases]

The "right" choice between invoice financing and factoring depends heavily on industry dynamics: payment cycle length, customer concentration, collections complexity, and confidentiality norms. The global factoring market reached 3.38 trillion euros in volume in 2023 according to FCI's Annual Review, yet the Federal Reserve Small Business Credit Survey found that only 4% of small U.S. employer firms applied for factoring, suggesting massive underutilisation driven by industry-specific uncertainty.

🚛 Trucking, Freight, and Staffing: Factoring

Long payment cycles (60 to 90+ days), high invoice volumes, and low confidentiality sensitivity make factoring the dominant choice in these verticals. Scenario: A trucking company with $200K/month in freight invoices factors at 85% advance rate, 2% per 30-day fee. Result: $170K cash within 24 hours instead of waiting 75 days. Specialised transport factors also handle broker verifications, fuel advances, and compliance documentation, adding operational value beyond pure cash acceleration.

As one factoring user shared about the fee dynamics:

"The fee depends on revenue; when we earned less than $1 million, it was about 3%. I kept negotiating until it fell to 1%." u/TheLordMyDog, r/loansforsmallbusiness Reddit Thread

🏗️ Manufacturing and Construction: Factoring (With Caveats)

Payment cycles of 60 to 120 days, milestone-based billing, and retainage clauses create complex AR. Factoring is common, but businesses must verify the factor handles progress billing and retainage separately. Scenario: A subcontractor with $80K in monthly progress billings uses whole-ledger factoring at 80% advance to fund materials and labour while waiting for general contractor payment. The factor manages lien waiver documentation as part of the collections process.

💻 Professional Services, SaaS, and Consulting: Financing

Shorter payment cycles (30 to 45 days), high customer LTV, and strong confidentiality requirements make invoice financing the better fit. Scenario: A B2B SaaS startup with $80K in quarterly invoices from 5 enterprise clients uses a revolving financing facility at 90% advance to bridge between billing cycles. Customers never know. The facility expands automatically as the client base grows. For SaaS and consulting founders looking to layer intelligence-led capital on top of their financing strategy, newer platforms combine data unification with funding access.

🛍️ DTC E-Commerce and Wholesale: Depends on Customer Mix

DTC brands selling B2B to large retailers (Nordstrom, Sephora) benefit from confidential invoice financing, as preserving the premium brand relationship is paramount. Factoring works better for brands with dozens of smaller wholesale accounts where collections overhead is a genuine burden. Scenario: A DTC beauty brand with $150K/month in wholesale invoices across 30 boutique retailers uses factoring to eliminate the need for a dedicated AR hire, saving $60K/year in salary while accelerating cash flow by 40+ days. Brands managing complex e-commerce tech stacks should evaluate how their financing choice integrates with existing operational tools.

Q9. What Should You Ask Before Signing With Any Provider? (Due-Diligence Checklist and Red Flags) [toc=Provider Due-Diligence Checklist]

Before signing with any invoice financing or factoring provider, ask these 12 questions. Every answer should be in writing before you commit.

✅ The 12-Question Provider Checklist

What is the all-in cost including origination, processing, wire, and draw fees, not just the headline rate?

Is there a monthly minimum volume requirement, and what penalty applies if I fall short?

What is the contract length, and what's the early termination penalty?

Will you file a UCC-1 lien, and is it limited to receivables or a blanket lien on all business assets?

Is customer notification required, and can I see a sample NOA letter before signing?

What is the recourse period, and what specific events trigger a buyback obligation?

What advance rate is guaranteed vs conditional on customer credit or invoice size?

How quickly are funds deposited after invoice submission: same day, next day, or 2 to 3 days?

Do you offer spot/selective factoring, or is whole-ledger required?

What happens if my customer disputes an invoice: who mediates, and who absorbs the cost during resolution?

Are there incremental aging penalties for invoices past 60 or 90 days?

Do you require a personal guarantee, and under what conditions can it be called?

⚠️ Red Flags: Walk Away If You See These

Provider won't disclose the full fee schedule in writing before contract execution

Requires a blanket UCC lien on all business assets, not just purchased receivables

Locks you into 12+ month contracts with punitive early-termination clauses (3 to 5% of facility value)

Includes auto-renewal provisions requiring 90-day advance cancellation notice

Demands a personal guarantee on a facility marketed as "non-recourse"

The severity of these traps is well-documented across provider reviews. One business owner's experience with a major RBF provider illustrates the UCC concern vividly:

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC. They can deem you in default for any reason at their discretion... they can enter your building and take your property in excess of the value of what is owed." Zachary Piech, ValuePetSupplies.com Wayflyer - TrustPilot Verified Review

Another provider's contract terms raised similar alarms:

"There is no personal guarantees or debentures they claim, though as a director signing this contract there is an indemnity. Which means it would fall back on the directors personally if not paid back. Uncapped at any point can ask for the full funds to be returned and you will still be left with the interest to be paid." Lewin Uncapped - TrustPilot Verified Review

⭐ What Good Provider Terms Look Like

The best factoring and financing providers offer month-to-month or quarterly terms, transparent tiered pricing published upfront, UCC filings limited to purchased receivables only, no personal guarantees, and same-day or next-day funding. If your provider can't meet these baselines, there are better options in the market. For a deeper look at how intelligence-led capital is reshaping provider standards, explore how AI-native platforms are eliminating many of these contract pitfalls entirely.

Q10. Common Myths, Overlooked Alternatives, and Cross-Border Considerations [toc=Myths, Alternatives and Cross-Border]

Four persistent myths continue to distort how business owners evaluate invoice-based capital. Clearing them up is essential before making a decision.

❌ Four Myths Debunked

Myth 1: "Factoring is only for struggling businesses." In reality, growth-stage companies with strong demand but long payment cycles, such as trucking firms, staffing agencies, and DTC brands selling to retailers, are the primary users. The global factoring market reached 3,781 billion euros in 2023, growing 3.3% year-over-year according to FCI's preliminary world factoring statistics. Struggling businesses don't generate 3.78 trillion euros in annual volume.

Myth 2: "Financing is always cheaper than factoring." When you account for internal collections overhead ($45K to $65K/year for an AR specialist), credit insurance premiums, and bad debt write-offs, factoring can be net-cheaper for businesses with long payment cycles and diverse customer bases.

Myth 3: "Non-recourse factoring means zero risk." Non-recourse typically covers only customer insolvency, not payment disputes, delivery disagreements, or slow payment. The gap between perception and contractual reality is where businesses get burned.

Myth 4: "Invoice financing and factoring are the same thing." They share a surface similarity (both use invoices to unlock cash) but differ fundamentally in ownership, accounting treatment, collections responsibility, and risk allocation.

💰 Alternatives Ranked by Speed and Founder-Friendliness

If neither financing nor factoring fits your situation, consider these alternatives:

Luca AI: AI-native capital: dynamically-priced working capital deployed in minutes with no personal guarantees, pricing that adjusts in real time as business performance changes, and capital sized precisely to the deployment opportunity rather than pushed as lump sums

Revenue-based financing (Wayflyer, Clearco, Uncapped): lump-sum advances repaid as a percentage of revenue, but priced on a static snapshot with limited deployment guidance

Business lines of credit: flexible but require strong credit and 4 to 8 week bank approval cycles

SBA loans: lowest rates available (6 to 10%) but 60 to 90 day approval timelines and heavy documentation requirements

Supply chain finance / dynamic discounting: buyer-initiated programs where your customer's bank pays you early at a discount, only available if your buyer offers it

🌍 Cross-Border and Export Invoice Considerations

International receivables introduce currency risk, jurisdictional collections complexity, and longer payment cycles of 90 to 120 days. Export factoring is typically handled through two-factor arrangements: a domestic factor partners with a correspondent factor in the buyer's country via the FCI network. The domestic factor advances funds; the overseas factor manages local collections and assumes the buyer's credit risk. Export financing may additionally require export credit insurance through entities like EXIM Bank or Euler Hermes. If more than 30% of your invoices are international, verify that your provider has documented cross-border capabilities and FCI membership before signing.

Q11. How Do AI-Native Capital Platforms Compete on Speed, Cost, and Flexibility? [toc=AI-Native Capital Platforms]

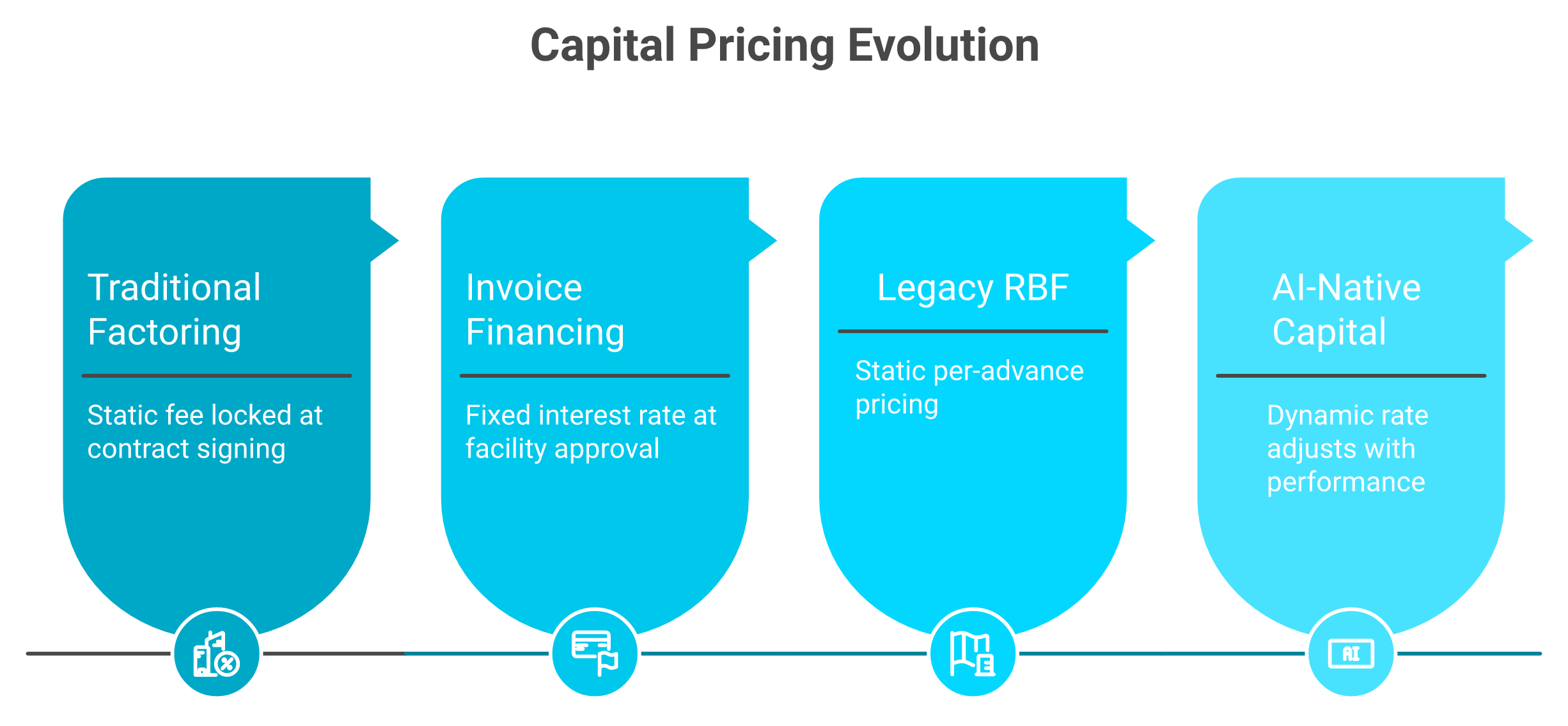

The financing-versus-factoring debate assumes capital pricing is static and one-size-fits-all. Traditional factoring locks in a fee percentage at contract signing. Invoice financing fixes an interest rate at facility approval. But your business isn't static: revenue fluctuates seasonally, margins shift with product mix, and customer payment behaviour changes quarter to quarter. AI-native capital platforms like Luca AI introduce a fundamentally different approach: dynamically-priced working capital where the rate adjusts continuously based on current business performance.

Capital pricing has evolved from static contract fees to dynamic, performance-based rates that decrease as your business metrics improve.

💰 Capital Metrics: How Luca AI Competes

Capital Metrics Comparison: Factoring vs Financing vs Legacy RBF vs Luca AI

Metric

Traditional Factoring

Invoice Financing

Legacy RBF (Wayflyer/Clearco)

Luca AI

Effective APR Range

20 to 45%

10 to 35%

15 to 45%

Dynamic: decreases as performance improves

Disbursal Speed

24 to 48 hours

24 to 72 hours

3 to 10 business days

Minutes

Personal Guarantee

Sometimes

Often required

Varies

❌ None

Contract Lock-In

6 to 12 months typical

12+ months typical

Per-advance

❌ No lock-in

UCC Lien Scope

Receivables (sometimes blanket)

Receivables

Blanket on all assets (common)

Receivables only

Pricing Model

Static fee at signing

Static rate at approval

Static per-advance

✅ Dynamic, real-time

Capital Sizing

Per-invoice

Revolving facility

Lump-sum push

✅ Sized to deployment need

Repayment

Customer pays factor

Business repays advance

Revenue-share percentage

✅ Automated revenue-share

⚠️ The Hidden Cost of Over-Capitalisation

Traditional RBF providers earn more on larger advances, creating an inherent incentive to push bigger lump sums. Capital sitting idle in a bank account still costs the business the full fee. Luca AI's model favours frequent, smaller advances sized precisely to the immediate deployment opportunity: inventory purchase orders, proven ad campaigns, or seasonal stock builds.

The operational reality of legacy providers is well-documented. One Wayflyer user shared:

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues this was incredibly disappointing." Joshua Hannan Wayflyer - TrustPilot Verified Review

Another user highlighted the contrast between sales promises and underwriting reality:

"Clearco Lost Touch With Its Own Business Model... Despite no change in our cash position or risk profile, and with strong recurring revenue, we started facing stricter cash-on-hand demands that made little sense for a company offering high-cost MCA." Melissa Clearco - TrustPilot Verified Review

⭐ Concrete Scenario: Q4 Inventory Funding

A Shopify DTC brand needs 40,000 euros to fund a Q4 inventory purchase order. Traditional factoring: 3% fee per 30-day period on the invoice = approximately 3,600 euros total cost if the retailer pays in 60 days. Invoice financing: 1.5%/month on the advance = approximately 1,800 euros but requires 600+ credit score and 12+ months operating history. Luca AI:dynamically-priced advance reflecting the brand's current ROAS, margin health, and cash position, deployed in minutes with no personal guarantee, and the effective rate decreases as Q4 performance materialises.

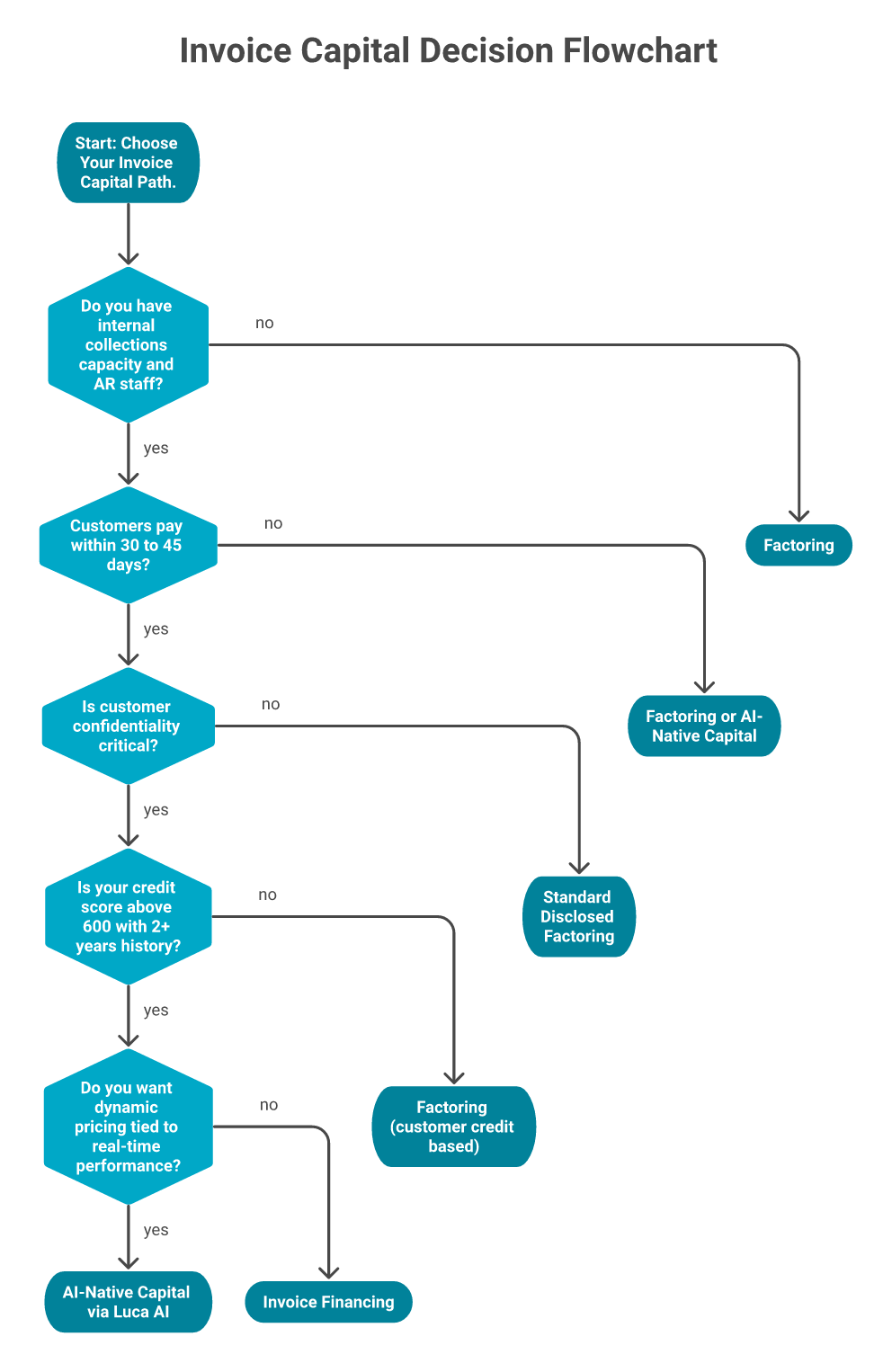

Q12. Decision Flowchart, Quick-Reference Summary, and FAQ [toc=Decision Flowchart and FAQ]

Use this five-question self-assessment to find your starting point. Answer each question honestly: the path leads directly to a recommendation.

Answer five questions honestly and follow the branching paths to identify whether invoice financing, factoring, or AI-native capital is your best fit.

✅ 5-Question Decision Flowchart

Do you have internal collections capacity and AR staff? Yes: invoice financing is viable. No: factoring handles collections for you.

Do your customers typically pay within 30 to 45 days? Yes: financing is almost always cheaper. No: factoring or AI-native capital may be necessary.

Is customer confidentiality critical to your brand relationships? Yes: confidential invoice financing or non-notification factoring. No: standard disclosed factoring works.

Is your business credit score above 600 with 2+ years of operating history? Yes: you'll qualify for financing at competitive rates. No: factoring approves based on customer credit, not yours.

Do you want capital pricing that reflects real-time business performance rather than a static application? Yes: explore AI-native platforms like Luca AI. No: traditional factoring or financing will serve you well.

Each profile should use the Q9 due-diligence checklist as the immediate next step before signing with any provider.

💬 Frequently Asked Questions

Is invoice financing the same as factoring? No. Financing is a loan where invoices serve as collateral: you retain ownership and collect payment. Factoring is a sale where the factor takes ownership and collects directly from your customer.

Which is cheaper, invoice financing or factoring? Financing is typically cheaper when you have strong credit and fast-paying customers. Factoring can be net-cheaper when you factor in collections overhead, bad debt risk, and the value of outsourced AR management.

Does invoice factoring affect my credit score? Factoring itself doesn't appear on credit reports since it's structured as a sale, not a loan. However, the UCC-1 lien filed by most factors will be visible to other lenders and may signal that traditional credit wasn't available.

Can I use both invoice financing and factoring at the same time? Generally no. Most financing and factoring agreements require exclusivity over your receivables via a UCC filing. Running both simultaneously would create competing claims on the same assets.

What is a Notice of Assignment in factoring? A formal letter sent to your customer informing them that the invoice has been assigned to a factoring company and that future payments should be directed to the factor. This is standard in disclosed factoring arrangements and is the primary reason some businesses prefer confidential invoice financing instead. For founders exploring how AI-driven cash flow forecasting can complement or replace traditional invoice products, newer platforms offer a third path that eliminates many of these structural trade-offs.

FAQ's

What is the structural difference between invoice financing and invoice factoring?

We find that the single most important distinction is ownership. Invoice financing is a loan: we borrow against unpaid invoices used as collateral, retain full ownership of those receivables, and remain responsible for collecting payment from our customers. Invoice factoring is a sale: we sell the invoices outright to a third-party factor who takes legal ownership and collects payment directly from our customers.

This structural fork cascades into every operational dimension:

Collections: Financing keeps collections internal; factoring outsources them entirely.

Confidentiality: Financing is invisible to customers; factoring typically requires a Notice of Assignment.

Balance sheet: Financing adds a liability; factoring removes the receivable with no new debt.

For e-commerce founders managing complex B2B relationships, this ownership distinction determines whether customer relationships stay protected or become visible to a third party. We recommend modelling both structures against your specific working capital requirements before committing.

Which is cheaper for my business: invoice financing or invoice factoring?

We cannot give a universal answer because cost depends on three variables unique to each business: credit profile, customer payment velocity, and internal collections capacity.

Here is how the math breaks down on a $50,000 invoice:

Financing at 1.5% monthly on an 85% advance ($42,500) costs $1,137 at 30 days, rising to $2,412 at 90 days.

Factoring at 2.5% per 30-day period on the full $50,000 face value costs $1,250 at 30 days, escalating to $3,750 at 90 days.

The gap widens because factoring fees apply to the full invoice value while financing interest accrues only on the drawn advance. At 90 days, factoring costs 55% more for the same invoice.

However, factoring can be net-cheaper when we factor in the $45K–$65K annual salary of an internal AR specialist, bad debt write-offs, and credit insurance premiums that financing requires us to absorb ourselves. We recommend using an AI-powered cash flow forecasting tool to model total cost under both structures with your real payment timelines.

Does invoice factoring affect my business credit score or future borrowing ability?

We see two layers to this question that most guides overlook. First, factoring itself typically does not appear on business credit reports because it is structured as an asset sale, not a loan. It neither builds nor damages our credit score directly. Invoice financing, by contrast, appears as a credit facility, and timely repayment actively strengthens our credit history.

However, there is a critical second layer: UCC-1 lien filings. Most factoring companies file a UCC-1 lien against our receivables, and some file blanket liens against all business assets. These filings are visible to every future lender conducting due diligence. They can signal to banks and investors that traditional credit was unavailable, potentially complicating future loan applications or fundraising rounds.

We recommend verifying three things before signing:

Whether the UCC filing is limited to purchased receivables or covers all assets.

Whether the factor will release the lien promptly upon contract termination.

Whether early termination penalties apply if we want to transition to conventional financing later.

For founders preparing for investor due diligence, understanding how each structure impacts unit economics and financial ratios is essential.

What is the difference between recourse and non-recourse factoring?

We find that this distinction is one of the most misunderstood areas in receivables finance. Recourse factoring, which accounts for approximately 83.8% of all U.S. factoring transactions, means the factor can return unpaid invoices to us after a defined period, typically 60 to 90 days. We must then buy the invoice back or replace it with a performing receivable.

Non-recourse factoring means the factor absorbs the credit risk, but with a critical limitation: coverage typically applies only to customer insolvency (bankruptcy), not to payment disputes, delivery disagreements, quality claims, or simple slow payment.

The cost premium is significant. Non-recourse adds 1 to 2 percentage points to the factoring fee. For a business factoring $500K monthly, that premium translates to $5,000–$10,000 per month in additional cost.

An alternative we recommend evaluating: purchasing trade credit insurance (0.1–0.5% of receivables annually) alongside recourse factoring. This combination can deliver non-recourse-like bad-debt protection at a fraction of the cost. For growth-stage brands managing tight margins, modelling these scenarios through cash flow forecasting reveals which approach preserves the most margin.

Are there alternatives to invoice financing and factoring for e-commerce businesses?

We see five alternatives worth evaluating when neither traditional financing nor factoring fits our situation:

AI-native capital (Luca AI): Dynamically-priced working capital deployed in minutes, where the rate adjusts in real time as business performance improves. No personal guarantees, no contract lock-in, and capital sized precisely to the deployment opportunity rather than pushed as lump sums.

Revenue-based financing (Wayflyer, Clearco): Lump-sum advances repaid as a percentage of revenue, but priced on a static snapshot with limited deployment guidance and often blanket UCC liens.

Business lines of credit: Flexible revolving access, but require strong credit scores and 4 to 8 week bank approval cycles.

SBA loans: Lowest rates available at 6–10%, but 60 to 90 day approval timelines and heavy documentation.

Supply chain finance: Buyer-initiated programs where our customer's bank pays us early at a discount, only available if our buyer offers the program.

For DTC and e-commerce founders specifically, the shift toward intelligence-led capital means pricing that rewards improving metrics rather than penalising static snapshots.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.svg)

.svg)

.svg)

.webp)

.avif)