Direct to Consumer Financing: The Complete Guide to Models, Platforms, Costs, and Implementation

12

mins read

In this article

TL;DR

D2C financing spans two ecosystems: consumer-facing BNPL at checkout and non-dilutive brand capital like RBF and inventory financing. BNPL lifts AOV 30-50% and conversion 20-30%, but MDR of 3-6% can destroy margins on low-margin products below 16.7% gross margin. An 8% flat-fee RBF advance repaid in 30 days yields roughly 96% effective APR; always model repayment timeline before accepting capital. EU CCD II, UK FCA, and US state-level laws bring BNPL and commercial financing under formal oversight by mid-2026. AI-driven underwriting and dynamic capital pricing are replacing static applications, with embedded lending projected to reach $34.73B by 2033.

Q1. What Is Direct to Consumer Financing and Why Does It Matter for DTC Brands? [toc=What Is D2C Financing]

Direct to consumer financing has become one of the most important strategic levers for ecommerce brands in 2026, yet most founders misunderstand what it actually means. The term carries two distinct definitions, and confusing them leads to fragmented decision-making at the exact moment when clarity matters most.

The Dual Meaning Every DTC Founder Must Understand

D2C financing operates as two distinct ecosystems — confusing them leads to fragmented capital decisions.

The first meaning refers to capital sourced by DTC brands: non-dilutive funding models like revenue-based financing, inventory financing, and merchant cash advances that provide growth capital without surrendering equity. The second meaning refers to consumer-facing financing offered at checkout: BNPL programs, POS installments, and embedded credit options that let shoppers split payments while merchants receive full payment upfront.

The Numbers Behind the Growth

Both categories are experiencing explosive growth. The embedded lending market was valued at $6.2 billion in 2024 and is projected to reach $16.1 billion by 2030, growing at a 17.4% CAGR. On the consumer side, merchants offering BNPL at checkout report conversion improvements of 20 to 30% and AOV increases of 30 to 50%. DTC founders now face a two-sided financing decision that most guides treat as one, and getting either side wrong has direct P&L consequences.

Why Traditional Financing Creates Fragmented Decisions

The problem is not a lack of options; it is how those options force founders into disconnected workflows. Applying to Wayflyer for growth capital in one tab. Configuring Klarna's BNPL checkout in another. Reconciling cash flow impact in Xero. Checking campaign performance in Meta Ads Manager. Each decision happens in its own silo, with no system connecting the capital you take to the performance data that should inform it.

Static Applications and Siloed Data

Traditional RBF providers offer capital based on static applications, a snapshot of your business from 60 days ago, without understanding whether the campaign you are funding will actually generate positive returns. BNPL platforms increase checkout conversion but add 3 to 8% merchant discount rates that nobody connects to your product-level contribution margins. The result: financing decisions made without the context they require.

"Wayflyer talks a big game about helping fast-growing brands bridge gaps and move with confidence. Cool story, but when we actually needed them for a basic, real-world funding scenario, the whole machine fell apart." Gemma Wayflyer - Trustpilot Verified Review

The Architectural Shift: Intelligence-Led Capital

In 2026, the competitive edge is not just accessing capital faster; it is accessing it smarter. The winning DTC brands are moving beyond "apply and hope" financing toward systems that reason across marketing performance, inventory velocity, and cash runway before recommending any financing action. The question has shifted from "Can I get funded?" to "Should I get funded for this specific opportunity, and what is the downstream cash impact?"

The Convergence Point

This is the convergence point: intelligence without capital is advice; capital without intelligence is risk. The brands pulling ahead have unified both sides into a single decision layer.

How Luca AI Unifies Intelligence and Capital

Luca AI was built for exactly this convergence. On the capital side, Luca competes directly on the metrics that matter: same-day disbursal speed, dynamic pricing that adjusts to real-time business health (not static 60-day-old snapshots), no personal guarantees, and revenue-linked repayment that flexes with your cash cycle. On the intelligence side, Luca operates as an AI layer over your data warehouse, connecting Shopify, Meta, Xero, and 20+ sources into a single reasoning layer that extracts root causes, predicts cash flow gaps, simulates scenarios, and pushes agentic reports to Slack and email automatically.

The system that identifies the growth opportunity can model its cash impact and fund it, without a separate application, a separate dashboard, or a 48-hour wait.

"While dashboards tell you your ROAS dropped, Luca tells you why, simulates the fix, and wires the capital you need to launch the next campaign."

Q2. What Are the Core Direct to Consumer Financing Models Every DTC Founder Should Know? [toc=Core D2C Financing Models]

Seven distinct financing models power the DTC ecosystem, each with fundamentally different cost structures, risk profiles, and suitability windows. Understanding the mechanics of each model is the prerequisite for making capital decisions that accelerate growth rather than constrain it.

The DTC Financing Landscape at a Glance

DTC Financing Models Overview

Model

Typical Cost

Funding Speed

Borrowing Range

Collateral Required

Best For

💰 Revenue-Based Financing

6 to 12% flat fee

24 to 48 hrs

$10K to $20M

None (revenue data)

Scaling ad spend, inventory

📦 Inventory Financing

3 to 10% advance rate

1 to 2 weeks

Inventory-value based

Inventory as collateral

Seasonal stock purchases

💸 Merchant Cash Advance

Factor rate 1.1 to 1.5x

Same day

$5K to $500K

Future receivables

Emergency cash gaps

🛒 BNPL/POS Financing

2 to 8% MDR

Instant integration

Per-transaction

None

Increasing checkout AOV

📄 AR/Invoice Factoring

1 to 5% discount

24 to 48 hrs

Invoice value

Outstanding invoices

B2B DTC with net terms

🏦 Revolving Credit Lines

8 to 25% APR

Pre-approved draws

$10K to $5M

Varies (often PG required)

Ongoing working capital

⚡ Embedded Lending

Variable

Real-time

Platform-dependent

Revenue data

Integrated platform users

How Each Model Works

Revenue-Based Financing (RBF) provides a lump-sum advance repaid as a fixed percentage of monthly revenue. Repayment scales automatically: strong months pay down faster, and slow months reduce the burden. Providers include Wayflyer, Clearco, and Uncapped. Best suited for DTC brands between $1M and $20M revenue with consistent monthly sales and a clear deployment plan for the capital.

Inventory, MCA, and BNPL Models

Inventory Financing advances 40 to 70% of your inventory's wholesale value, allowing brands to purchase stock without depleting cash reserves. The inventory itself serves as collateral. Ideal for seasonal DTC brands preparing for Q4 or launching new product lines.

Merchant Cash Advances (MCA) provide same-day capital in exchange for a percentage of future credit card sales. Factor rates of 1.1 to 1.5x make MCAs the most expensive option: a $100K advance at a 1.3 factor costs $130K total, regardless of repayment timeline.

BNPL/POS Consumer Financing is not capital for your brand; it is financing you offer shoppers at checkout. The merchant pays a 2 to 8% discount rate per transaction while receiving the full purchase amount upfront from the BNPL provider.

Invoice Factoring, Credit Lines, and Embedded Lending

Invoice Factoring converts outstanding B2B invoices into immediate cash at a 1 to 5% discount. Useful for DTC brands with wholesale channels operating on net-30 or net-60 terms.

Revolving Credit Lines function like business credit cards: draw what you need, repay, and draw again. APRs range from 8 to 25%, but most require personal guarantees and minimum credit scores above 680.

Embedded Lending integrates financing directly into the commerce platform (e.g., Shopify Capital). Capital offers appear automatically based on platform sales data, with no separate application required.

⚠️ The APR Trap Most Founders Miss

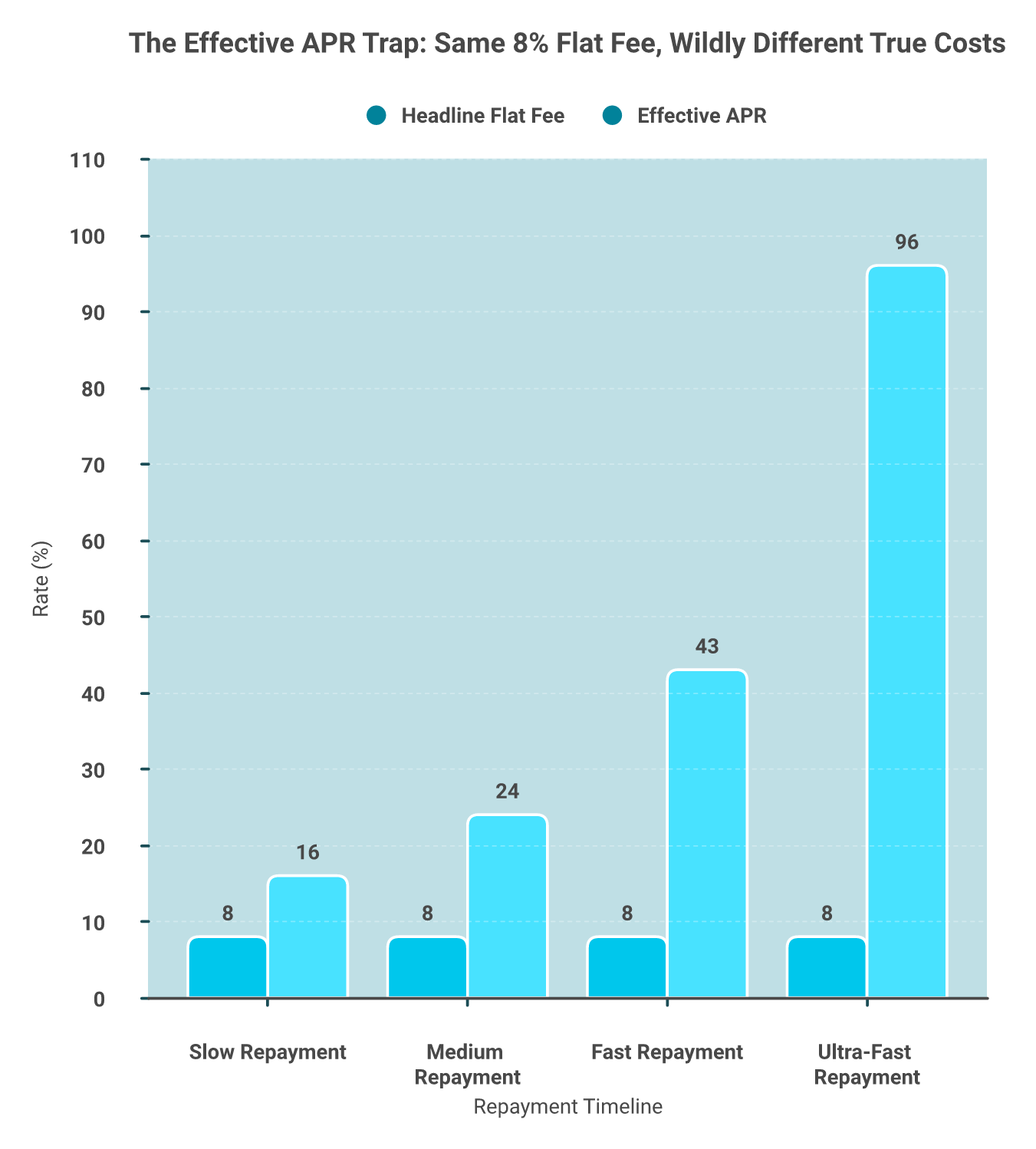

Flat fees are misleading without repayment timeline context. A $100K advance at 8% flat fee ($8K cost) repaid over 4 months yields an effective APR of approximately 24%. That same $100K at 8% repaid in just 1 month, because your revenue share is high, yields an effective APR of roughly 96%.

The formula: Effective APR = (Fee / Principal) x (365 / Days to Repay)

"6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% / 4 months x 12 months = 36% APR. In the best case." Julian Fernau Clearco - Trustpilot Verified Review

Always calculate effective APR before accepting any offer. The headline fee rarely tells the full story.

How Luca AI Simplifies Model Selection

Luca AI eliminates manual APR calculations and model comparisons by analyzing your real-time revenue data, cash runway, and deployment plans, then recommending the optimal financing structure. Luca's own capital offers feature dynamic pricing that adjusts as your business health changes, same-day disbursal, and no personal guarantees. No separate applications, no spreadsheet modeling, no 48-hour waits.

Q3. How Do BNPL and POS Financing Work for Merchants, and What Does It Actually Cost? [toc=BNPL Merchant Costs]

BNPL and POS financing have moved from optional checkout features to essential conversion tools for DTC merchants. But the merchant-side economics are more nuanced than most providers advertise, and the difference between profitable and margin-destroying BNPL comes down to understanding the fee structures, break-even thresholds, and hidden costs.

Merchant Fee Comparison: Major BNPL Providers

BNPL Provider Merchant Fee Comparison

Provider

MDR Range

Per-Txn Fee

Payout Speed

Max Transaction

Best For

Klarna

3.29% to 5.99%

+ $0.30

1 to 3 days

Varies by plan

EU reach, fashion/lifestyle

Afterpay

4% to 6%

+ $0.30

1 to 2 days

$2,000 (default)

Fashion, beauty, impulse buys

Affirm

3% to 6%

+ $0.30

1 to 3 days

$17,500+

High-ticket items ($500+)

PayPal Pay Later

Variable

Included

1 to 2 days

Varies

Existing PayPal merchants

Shop Pay Installments

0% to 5.9%

Variable

Next business day

$17,500

Shopify-native stores

How the Merchant-Lender-Consumer Flow Works

The mechanics follow a consistent pattern across all major BNPL providers:

⭐ Customer selects BNPL at checkout and completes a soft credit pre-qualification (no impact on credit score)

✅ BNPL provider approves the transaction and pays the merchant the full purchase amount minus the MDR fee

✅ Merchant receives payout within 1 to 5 business days, bearing zero consumer credit risk

💰 BNPL provider collects installments directly from the consumer (typically 4 payments over 6 to 8 weeks for standard BNPL, or 6 to 60 months for POS financing plans)

The Key Trade-Off

The merchant gets paid upfront and transfers all credit risk to the BNPL provider. The trade-off is the merchant discount rate, which ranges from 2% to 8% depending on the provider, your negotiated volume rate, and the financing plan selected.

The Impact on Business Metrics, With Real Numbers

The data consistently shows meaningful commercial impact:

⭐ AOV increase: Merchants report 30 to 50% higher average order values when BNPL is offered. Shop Pay Installments reports up to 50% AOV increase

✅ Conversion rate lift: Klarna reports 30% improvement in checkout conversion; industry averages show 20 to 30% improvement across providers

If your BNPL provider charges 5% MDR and delivers a 35% AOV increase, your minimum gross margin to break even is 14.3%. Any product with gross margins above that threshold generates net positive revenue from BNPL. Any product below it loses money on every financed transaction.

Not every product benefits from BNPL — this matrix reveals where checkout financing creates or destroys value.

Worked example: A DTC brand processing $500K/month through Afterpay at 5% MDR pays $25K/month in fees ($300K/year). If BNPL drives a 30% AOV lift, the incremental monthly revenue is $150K, but only $142.5K after BNPL fees. Net positive only if the blended gross margin on incremental sales exceeds 16.7%.

Hidden Costs to Factor In

❌ BNPL-specific return rates run 15 to 20% higher than standard purchases

❌ Chargebacks on financed transactions are more complex and costly to dispute

❌ Integration maintenance and provider-specific checkout friction

How Luca AI Optimizes Your BNPL Economics

Luca AI's intelligence layer connects your BNPL transaction data to your full P&L, analyzing MDR impact on contribution margin by product category and channel in real-time. Luca predicts which product lines generate positive ROI after merchant discount rates, flags margin erosion before it compounds, and pushes automated BNPL performance reports to Slack and email. You stop guessing whether BNPL is profitable and start knowing, at the product level.

Q4. How Do Leading DTC Financing Platforms Compare: Luca AI vs. Wayflyer vs. Clearco vs. Shopify Capital vs. 8fig? [toc=Platform Comparison 2026]

You have validated product-market fit, identified a winning campaign, and need $50K to $500K to scale it before the window closes. Five platforms dominate DTC brand financing in 2026, but they operate through fundamentally different architectures, and the platform you choose determines far more than the capital you receive.

Luca AI: Intelligence-Led Capital

✅ Luca AI competes on the three capital metrics that DTC founders care about most: cost (dynamic pricing that adjusts to real-time business health, not static rates locked at application), speed (same-day disbursal vs. the 24 to 72 hour industry standard), and flexibility (revenue-linked repayment that automatically adjusts during slow months, no cash crunches from rigid schedules). No personal guarantees. No 60-day-old application snapshots. Capital offers surface continuously as your business health qualifies.

Wayflyer: Fast Capital, Limited Context

✅ Wayflyer has deployed $1.6B+ to ecommerce brands, offering RBF with 5 to 10% fees and 24-hour approval with no personal guarantees.

❌ However, Wayflyer operates as a "capital black box": you receive an offer without visibility into how it is calculated or whether the deployment you are planning will generate positive returns. Multiple merchants report broken commitments and opaque underwriting:

"After being offered funding in writing with specific amounts, repayment terms, and confirmation that the deal was approved, Wayflyer abruptly reversed their decision at the last minute. This caused significant disruption to our operations and cash flow." Geoff Brand Wayflyer - Trustpilot Verified Review

"Read their terms and contract carefully! They said their offer is not secured, which is false. They can deem you in default for any reason at their discretion. The worst bank agreement I have read in 25 years." Zachary Piech Wayflyer - Trustpilot Verified Review

Clearco: DTC-Focused, Operationally Challenged

✅ Clearco was purpose-built for DTC with weekly repayment structures and ecommerce-native underwriting.

❌ Since 2022, Clearco has faced repeated layoffs and operational deterioration. Merchants report inconsistent support, opaque fee calculations, and payment processing failures:

"Ops team was terrible. They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly, and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

Shopify Capital: Seamless but Exclusive

✅ Shopify Capital offers the smoothest integration for Shopify merchants: instant approval, automatic revenue-share repayment, and zero additional platform setup.

❌ It is invite-only, meaning you cannot apply proactively. Funding amounts are capped and typically conservative relative to revenue. Merchants who need capital urgently cannot trigger the process themselves.

8fig: Supply-Chain Focus, Execution Risk

✅ 8fig offers a unique continuous funding model designed around supply-chain timelines, with capital deployed in stages matching your procurement cycle.

❌ Multiple merchants report bait-and-switch tactics, with agreed-upon funding reduced or pulled at the last minute:

"We had a signed agreement with 8fig for three preset rounds of funding at pre-agreed rates. They only funded the first round, which was at the highest cost, and then backed out of the rest at the last minute." Melissa 8fig - Trustpilot Verified Review

⭐ Head-to-Head Comparison

DTC Financing Platform Comparison 2026

Criteria

Luca AI

Wayflyer

Clearco

Shopify Capital

8fig

💰 Fee Structure

Dynamic (real-time)

5 to 10% flat

6 to 12% flat

Revenue share (varies)

Variable by cycle

⏰ Disbursal Speed

Same day

24 to 72 hrs

24 to 48 hrs

Instant (if invited)

48 to 72 hrs

Capital Range

$10K to $500K

$10K to $20M

$10K to $10M

Up to $2M

$10K to $1M

Personal Guarantee

❌ None

❌ None

❌ None

❌ None

❌ None

Repayment Flexibility

✅ Revenue-linked, auto-adjusts

Revenue share, fixed %

Weekly, fixed %

Revenue share

Fixed schedule by cycle

Real-Time Health Pricing

✅ Continuous

❌ Static at application

❌ Periodic

❌ Shopify data only

❌ Static

Setup Complexity

10-min integration

Application + data connect

Application + data connect

Automatic (invite)

Application + supply-chain mapping

Who Should Choose What

Choose Wayflyer if you need capital above $500K and have an internal team to independently assess deployment ROI. Choose Shopify Capital if you are Shopify-native and lucky enough to qualify for an invite. Choose Luca AI if you want the fastest disbursal, fairest dynamic pricing, and revenue-linked repayment that adjusts automatically: capital that gets smarter as your business gets stronger.

Q5. What Are the Real Benefits of D2C Financing, and What Risks Should You Watch For? [toc=Benefits and Risks]

D2C financing drives measurable commercial impact across three stakeholder groups: merchants, consumers, and DTC brand founders. But the gains come with costs and risks that most guides conveniently omit. Here is what both sides of the ledger actually look like.

⭐ Benefits for Merchants Offering Consumer Financing

✅ AOV increase of 30 to 50%: Shop Pay Installments reports up to 50% higher average order values when financing is displayed at checkout

✅ Conversion rate lift of 20 to 30%: BNPL options reduce checkout friction, particularly for purchases above $100

✅ Cart abandonment reduction of up to 28%: Displaying installment amounts on product pages, not just at checkout, captures intent earlier in the funnel

✅ Zero consumer credit risk: The BNPL provider assumes all default risk; merchants receive full payment upfront minus MDR

⭐ Benefits for DTC Brand Founders Taking Capital

Non-dilutive capital preserves equity, a critical advantage over VC rounds that typically cost 15 to 30% ownership. Revenue-based financing and modern fintech models offer repayment tied to cash flow cycles, meaning slow months do not create crippling fixed payments. Speed of access is the second major unlock: when a winning Meta campaign is live and needs scaling today, not in 6 to 8 weeks, RBF provides capital in 24 to 48 hours without personal guarantees.

💰 Case Study

A mid-market DTC skincare brand processing $4M annually used RBF to fund a Q4 inventory purchase of $200K at 8% flat fee ($16K cost). The funded inventory generated $680K in Q4 revenue, a 3.4x return on capital deployed. Without financing, the brand would have missed the seasonal window entirely, representing an estimated opportunity cost of $480K in lost revenue.

❌ The Risks Most Guides Do Not Disclose

Consumer-Side Risks

BNPL users carry an average of 3 to 4 active installment plans simultaneously, increasing default risk across the ecosystem

BNPL-specific return rates run 15 to 20% higher than standard purchases; consumers buy more freely when payments feel abstract

Chargebacks on financed transactions are more complex and costly to dispute

Brand-Capital Risks

⚠️ Flat-fee RBF appears cheap, but effective APR spikes dramatically with fast repayment (8% fee repaid in 1 month = approximately 96% APR)

MCA factor rates of 1.1 to 1.5x represent the most expensive capital available

Some providers include revenue share clauses that persist beyond the initial advance or change terms mid-contract

"They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly, and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

"They trick you into signing a low APR contract, and then one month into the term, they hike up the rates by offering more funds. They divide the lending into cycles." Khalid 8fig - Trustpilot Verified Review

How Luca AI Helps You Navigate Both Sides

Luca AI's intelligence layer monitors both sides of this equation: predicting which product-channel combinations generate positive ROI after MDR costs, simulating the cash impact of taking capital before you commit, and flagging margin erosion in real-time. Agentic reports delivered via Slack and email surface risk signals weekly so you catch issues before they hit the P&L.

Q6. What Does D2C Financing Actually Cost? A Worked Cost Analysis with Real Numbers [toc=True Cost Analysis]

The true cost of D2C financing depends almost entirely on variables most providers do not highlight: repayment speed, fee compounding mechanics, and hidden margin erosion. Three worked scenarios reveal how the same headline fee can translate into vastly different effective costs.

💰 Scenario 1: Revenue-Based Financing True Cost

A DTC brand takes a $200K advance at 8% flat fee ($16K total cost). Here is where the math diverges:

RBF Effective APR by Repayment Timeline

Repayment Timeline

Monthly Revenue Share

Months to Repay

Effective APR

Fast repayment

$100K revenue x 10% share

~2.2 months

⚠️ ~43%

Medium repayment

$60K revenue x 10% share

~3.6 months

~24%

Slow repayment

$40K revenue x 10% share

~5.4 months

~16%

The formula: Effective APR = (Fee / Principal) x (365 / Days to Repay)

The counterintuitive reality: faster-growing brands with higher revenue pay more in effective APR terms because the flat fee is retired in fewer days. A $200K advance at 8% repaid in just 30 days yields an effective APR of approximately 96%.

The same 8% flat fee translates to anywhere from 16% to 96% effective APR depending on how fast you repay.

💸 Scenario 2: BNPL Merchant Cost at Scale

A DTC brand processes $500K/month through Afterpay at 5% MDR:

Any product with gross margins below 16.7% is destroying value with every BNPL transaction. For a DTC brand with blended 45% gross margins, BNPL is highly profitable. For a low-margin electronics brand at 12%, every financed sale loses money.

⚠️ Scenario 3: $150K Capital Need, Three Models Compared

$150K Capital Cost Comparison Across Three Models

Model

Total Cost

Effective APR

Personal Guarantee

Speed

Best When

Inventory Financing (7% advance fee)

$10,500

~28% (30 days)

❌ Inventory as collateral

1 to 2 weeks

Seasonal stock purchase

Revolving Credit Line (18% APR)

$2,219 (30 days)

18%

⚠️ Usually required

Pre-approved

Ongoing working capital

MCA (1.3x factor rate)

💸 $45,000

365%+ (30 days)

❌ Future receivables

Same day

Emergency only

The spread is staggering: the same $150K need over 30 days costs $2,219 on a credit line or $45,000 via MCA. That is a 20x cost difference for identical capital.

"6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% / 4 months x 12 months = 36% APR." Julian Fernau Clearco - Trustpilot Verified Review

How Luca AI Eliminates the Guesswork

Luca AI models true cost-of-capital scenarios against your real-time revenue data, simulating not just what financing costs in isolation, but what it costs relative to the opportunity it funds. Ask Luca: "What is my effective APR if I take $100K and repay at my current revenue run rate?" and get the answer in seconds, not spreadsheet hours. Dynamic pricing means Luca's own capital offers adjust automatically as your business health changes, ensuring you never overpay for capital your metrics do not justify.

Q7. How Do the Top D2C Financing Platforms Compare in 2026? [toc=Platform Comparison 2026]

Two distinct ecosystems serve D2C financing: brand capital providers that fund your growth and consumer-facing BNPL platforms that finance your shoppers. Evaluating them requires separate frameworks because they solve fundamentally different problems.

⭐ DTC Brand Capital Providers

DTC Brand Capital Providers Comparison

Provider

Fee/Rate

Disbursal Speed

Funding Range

Personal Guarantee

Repayment Model

Real-Time Health Pricing

Luca AI

Dynamic (adjusts to live health)

⏰ Same day

$10K to $500K

❌ None

Revenue-linked, auto-adjusts

✅ Continuous

Wayflyer

2 to 10% flat

24 to 72 hrs

$10K to $20M

❌ None

Revenue share, fixed %

❌ Static at application

Clearco

6 to 12%

24 to 48 hrs

$10K to $10M

❌ None

Revenue share, weekly

❌ Periodic

Uncapped

2 to 14%

24 hrs

$10K to $5M

❌ None

Revenue share

❌ Monthly review

Shopify Capital

Varies

Instant (invite-only)

Up to $2M

❌ None

Revenue share

❌ Shopify data only

8fig

Variable by cycle

48 to 72 hrs

$10K to $1M

❌ None

Fixed schedule by cycle

❌ Supply-chain data

❌ What Real Users Report About These Platforms

Wayflyer users report approval reversals and opaque underwriting:

"We had gotten a batch of offers from them, which we accepted the least amount. Business turned out better than usual, and when we came back we were rejected. The underwriters are behind the scenes. If they come back with something nonsensical, which they did, you cannot prove them otherwise." Mike M Wayflyer - Trustpilot Verified Review

"We signed a $3M loan deal, only for them to come back two weeks later saying, 'Oops, our C-suite decided to focus on Amazon deals,' and slashing our funding to $1M. Then months later, right as we hit our 5% EBITDA margin, they cut it again to $350K." Xin Shui Uncapped - Trustpilot Verified Review

8fig users report predatory cycle structures:

"They sucker you in by saying how they will scale you big and then since you are hooked legally now, they create a disbursement and payment plan that gets extremely confusing to follow in a dashboard and you end up using the prior disbursement to cover the next, like one of those high-interest payday advances." Suckered In 8fig - Trustpilot Verified Review

Consumer-Facing BNPL/POS Platforms

Consumer-Facing BNPL/POS Platform Comparison

Provider

MDR Range

Payout Speed

Max Transaction

Consumer Credit Check

Best For

Affirm

3 to 6% + $0.30

1 to 3 days

$17,500+

Soft check

High-ticket ($500+)

Klarna

3.29 to 5.99% + $0.30

1 to 3 days

Varies

Soft check

EU reach, fashion/lifestyle

Afterpay

4 to 6% + $0.30

1 to 2 days

$2,000

Soft check

Fashion, beauty, impulse

SweetPay

Custom

1 to 3 days

Varies

Full check

Home services, contractors

Jifiti

White-label

1 to 3 days

Varies

Bank-branded

White-label POS

Skeps

Custom

1 to 3 days

Varies

Multi-lender waterfall

Highest approval rates

Note: Luca AI does not appear in this table. Luca competes as a brand capital provider, not a consumer-facing BNPL platform.

Why Luca AI Leads on Capital Metrics

Luca AI wins on the three metrics that determine real capital value: (1) Speed, same-day disbursal vs. the 24 to 72 hour industry standard, (2) Cost fairness, dynamic pricing that drops as your business health improves rather than static rates locked at application, (3) Repayment flexibility, revenue-linked terms that automatically adjust during slow months, preventing the cash crunches that plague fixed-schedule providers.

Q8. How Do You Implement D2C Financing? A Step-by-Step Integration Guide [toc=Implementation Guide]

Implementing D2C financing involves two distinct workflows: adding consumer-facing BNPL to your storefront and onboarding with a brand-capital provider. Most merchants need both, and the sequence matters.

Part A: Implementing Consumer Financing at Checkout

⭐ Audit your checkout flow: Identify high-AOV products and cart abandonment hotspots where BNPL adds the greatest conversion lift. Products above $100 see the strongest BNPL impact.

Evaluate providers by your market: Klarna for EU reach, Affirm for US high-ticket ($500+), Afterpay for fashion/beauty, Skeps for maximum approval rates via multi-lender waterfall.

Technical integration: Shopify app install takes 5 minutes for Klarna or Afterpay. Headless storefronts require API integration. Custom platforms use hosted checkout redirects.

Configure checkout UX: Display installment amounts on product listing pages ("4 payments of $24.99"), place BNPL above the fold, and enable soft-credit pre-qualification before checkout.

A/B test for 2 to 4 weeks: Measure conversion lift, AOV change, and return rate differential before full rollout.

💰 Monitor MDR impact monthly: Track BNPL margin erosion at the product-category level, not just blended averages.

Part B: Onboarding with a Brand-Capital Provider

⭐ Connect your data sources via API or OAuth: Shopify, Stripe, and your accounting platform. Luca AI completes this in under 10 minutes with no-code setup.

Complete prequalification: Modern providers use automated revenue verification. Avoid providers still requesting manual document uploads; it signals outdated underwriting.

Review capital offers on effective APR: Compare true cost using the formula from Q6, not headline flat fees.

Define your deployment strategy before accepting: Allocate capital to specific use cases, such as inventory, ad spend scaling, and seasonal preparation, before taking money.

Establish monitoring cadence: Track ROI on deployed capital monthly against your original deployment thesis.

Choosing a Lending Partner: 7-Point Evaluation Checklist

Lending Partner Evaluation Checklist

Criteria

What to Look For

❌ Red Flag

Fee transparency

Clear APR calculation, no hidden costs

"Flat fee" with no repayment timeline context

⏰ Disbursal speed

Same-day to 48 hours

1 to 2 week processing

Repayment flexibility

Revenue-linked, auto-adjusts

Fixed weekly debits regardless of revenue

Personal guarantee

None required

PG required for any amount

Prequalification

Automated, API-based

Manual document upload

Data integration

API/OAuth with live data

CSV uploads, manual bank statements

Track record

Verified reviews, transparent complaints

No public reviews, suppressed feedback

⚠️ Common Implementation Mistakes

❌ Hiding BNPL in checkout only instead of surfacing on product pages, which reduces conversion lift by 40 to 60%

❌ Offering BNPL on low-margin products where 5% MDR erodes profit entirely

❌ Not tracking BNPL-specific refund rates (typically 15 to 20% higher than standard)

❌ Accepting capital without modeling repayment timeline against revenue forecasts

❌ Failing to negotiate volume-based MDR reductions after reaching $100K+/month in financed transactions

"I was not sure about the exact payment terms or how everything works. It is my first time lending for my business. NOT BEGINNERS FRIENDLY AT ALL." shakib mustafa Clearco - Trustpilot Verified Review

How Luca AI Simplifies Both Workflows

Capital side: Luca AI's onboarding takes under 10 minutes. Connect Shopify and your accounting platform, and capital offers surface automatically based on your live business health. No documents, no waiting, no 48-hour gaps.

Analytics side: Luca's intelligence layer then monitors your financed transactions continuously, simulating ROI on deployed capital, tracking BNPL margin impact by product category, and pushing weekly performance reports to Slack and email so you always know if your financing is working.

Q9. What Regulatory and Compliance Requirements Apply to D2C Financing in 2026? [toc=Regulatory Compliance 2026]

The regulatory landscape for D2C financing is shifting rapidly across every major market. Whether you are offering consumer financing at checkout or taking brand capital as a DTC founder, understanding your disclosure obligations, lending partner requirements, and cross-border compliance risks is no longer optional; it is a prerequisite for operating legally.

🇺🇸 United States: CFPB, TILA, and State-Level Disclosures

The CFPB's 2024 interpretive rule attempted to classify BNPL products as credit cards under the Truth in Lending Act (TILA), requiring full APR disclosure, billing dispute rights, and refund protections. However, after legal challenge by the Financial Technology Association, the CFPB revoked the rule and shifted its enforcement priorities away from BNPL in 2025. This does not mean BNPL is unregulated; individual states are filling the gap:

✅ California (SB 1235): Requires commercial financing providers to disclose total cost of financing expressed as an annualized rate, payment terms, and prepayment policies for offers of $500,000 or less

✅ New York (Commercial Finance Disclosure Law): Similar APR-equivalent disclosure requirements for MCA, RBF, and factoring products offered to small businesses

⚠️ Virginia: Enacted comparable transparency mandates for commercial lending products

What this means for DTC founders: If you are taking capital from an RBF or MCA provider, you now have disclosure rights; your provider must show you the effective APR, not just a flat fee percentage. If you are offering consumer financing, your BNPL partner handles regulatory compliance, but you inherit obligations around refund policies and dispute resolution.

🇪🇺 EU and 🇬🇧 UK: BNPL Under Formal Regulation

The EU's Second Consumer Credit Directive (CCD II, Directive 2023/2225) explicitly brings BNPL within the scope of consumer credit regulation. Key requirements:

Full creditworthiness assessment before approving consumer BNPL transactions

Pre-contractual information disclosure including total cost of credit

14-day right of withdrawal for consumers on all BNPL agreements

Member states must transpose CCD II into national law by November 2026

In the UK, the FCA confirmed that BNPL will become a regulated activity from 15 July 2026. BNPL providers must obtain FCA authorization, conduct affordability checks, and comply with the Consumer Duty. Firms can register for the Temporary Permissions Regime between 15 May and 1 July 2026.

🇮🇳 India and APAC: RBI Digital Lending Framework

India's RBI Digital Lending Guidelines (2022, updated with FLDG norms in 2023) require all digital lending to flow through regulated entities. Key provisions:

Four major markets are simultaneously tightening D2C financing regulation — cross-border merchants must comply with all of them.

💰 First Loss Default Guarantee (FLDG) capped at 5% of the loan portfolio, limiting how much risk fintechs can absorb on behalf of regulated lenders

Mandatory APR and fee disclosure at the point of loan origination

Direct disbursal to borrower's bank account only (no third-party pass-through)

Complete data privacy requirements; LSPs cannot store customer data beyond what is essential

✅ Merchant Compliance Checklist

Merchant Compliance Checklist for D2C Financing

#

Requirement

Applies To

1

Display BNPL provider's APR and total credit cost at checkout

Merchants offering consumer financing (EU/UK)

2

Verify lending partner holds required licenses in every jurisdiction you sell

All merchants

3

Implement clear refund policies for financed purchases

Review commercial financing disclosures from your capital provider

US merchants taking RBF/MCA (SB 1235)

6

Ensure data sharing with lending partners complies with GDPR/CCPA

Cross-border merchants

7

Maintain financed transaction records for dispute resolution

All merchants

8

⏰ Audit annually; regulations are evolving rapidly

All merchants

How Luca AI Ensures Compliance Transparency

Luca AI partners with regulated lending entities and ensures all capital offers include full cost-of-capital transparency: effective APR, total repayment amount, and itemized fee breakdowns, compliant with US commercial financing disclosure laws and EU consumer credit requirements. No opaque flat fees, no hidden costs.

Q10. What Emerging Trends Will Reshape D2C Financing by 2027? [toc=Emerging Trends 2027]

Five converging forces are about to fundamentally change how DTC brands access, price, and deploy financing. The brands that adapt to these shifts early will secure structural advantages in cost of capital, speed of deployment, and capital efficiency.

The Current Inflection Point

The embedded lending market was valued at $9.25 billion in 2026 and is expected to reach $34.73 billion by 2033, growing at a 20.8% CAGR. The broader embedded finance market is projected to surpass $723 billion by 2033. Three structural shifts are converging simultaneously: AI is replacing static credit applications with continuous underwriting, open banking regulations are enabling instant data sharing between commerce and finance platforms, and low-code infrastructure is democratizing access to lending capabilities for non-fintech brands.

By 2027, the "apply with 60-day-old financials and wait 48 hours" model will be functionally obsolete. AI-native lenders already assess business health continuously, adjusting capital offers daily based on live revenue, marketing performance, and cash runway. This means capital pricing becomes dynamic: your rate improves when your business improves, not when you reapply.

The implications are significant for DTC founders currently trapped in static pricing models:

"Company loves to lie unfortunately. They gave our firm a $90,000 loan. At the time, they mentioned that once we paid off 50% of the loan, we would be eligible for additional financing so we can continue scaling. That was one big lie." Adam Zackman Wayflyer - Trustpilot Verified Review

Static underwriting creates exactly these broken promises, because the lender's snapshot of your business at application does not reflect your reality at the halfway point.

🔓 Trend 2: Open Banking Enables Instant Verification

PSD3 in the EU and CFPB Section 1033 in the US are enabling DTC brands to share financial data directly with lenders via API, eliminating manual document uploads, reducing approval times from days to minutes, and enabling real-time creditworthiness assessment. For DTC founders, this means capital access becomes frictionless: connect your bank account once and capital offers surface automatically based on live data.

DTC brands will offer branded financing at checkout without building fintech infrastructure. White-label BNPL, embedded credit lines, and loyalty-linked financing are becoming standard Shopify and WooCommerce plugins. The embedded finance market's projected growth to over $700 billion by 2033 reflects this infrastructure shift; financing disappears into the checkout experience.

🔗 Trends 4 and 5: Blockchain Lending and Global Expansion

Decentralized lending protocols are beginning to offer working capital using on-chain revenue data as collateral, still early-stage but maturing rapidly. Meanwhile, D2C financing models are expanding aggressively across India (UPI + embedded lending under RBI frameworks), Southeast Asia (GrabPay, ShopeePay), and Latin America (Mercado Credito), creating cross-border financing opportunities for DTC brands selling internationally.

Where Luca AI Stands in This Future

Capital lens:Luca AI already operates in the AI-driven underwriting future: continuous health assessment, dynamic pricing that adjusts as your business grows, and same-day disbursal without static applications. While legacy providers are building toward real-time assessment, Luca has shipped it.

Analytics lens: Luca's intelligence layer makes these trends actionable today, predicting cash flow gaps before they materialize, simulating financing decisions across your entire business, and automatically surfacing opportunities via agentic report delivery to Slack and email. By 2027, the best DTC brands will not apply for financing; their AI layer will tell them when to take it, how much, and where to deploy it.

Q11. How Should You Choose the Right D2C Financing Strategy for Your Business? [toc=Choosing Your Strategy]

D2C financing is not one decision; it is two. First: should you offer consumer-facing financing at checkout (BNPL/POS) to boost conversion? Second: should you take brand capital (RBF/inventory financing/credit line) to fund growth? These decisions interact; the capital you take should fund the opportunities your data reveals. But most founders treat them in isolation because their tools force it.

❌ The Wrong Way to Decide

Most founders choose their BNPL provider based on brand recognition (Klarna because it is famous) and their capital provider based on approval speed (whoever says yes first). This ignores the questions that actually determine ROI:

Does the BNPL provider's MDR work with my margin structure at the product level?

Does the capital provider's repayment model match my revenue seasonality?

Am I evaluating effective APR or just flat fee percentages?

Can I model the downstream cash impact before committing?

"Wasted 10 days with daily promises that were never kept and had to follow up daily. Was asked for countless documents to tell me in the end that I don't have enough cash runway to borrow money, absolute nonsense from some underwriter that does not understand e-commerce." A Ovidiu Uncapped - Trustpilot Verified Review

✅ The Right Framework: Consumer Financing Decision

Score each BNPL/POS provider on these 6 criteria (0 to 2 points each):

BNPL Provider Scoring Framework

Criteria

Affirm

Klarna

Afterpay

Skeps

MDR rate vs. your gross margin

⭐⭐ (negotiable)

⭐ (higher range)

⭐ (4 to 6%)

⭐⭐ (custom)

AOV lift for your ticket size

⭐⭐ (best above $500)

⭐⭐ (strong $100 to $500)

⭐⭐ (strong $50 to $200)

⭐ (variable)

Consumer approval rate

⭐ (stricter checks)

⭐⭐ (wide approvals)

⭐⭐ (wide approvals)

⭐⭐ (multi-lender waterfall)

Integration complexity

⭐ (API-heavy)

⭐⭐ (Shopify plugin)

⭐⭐ (Shopify plugin)

⭐ (custom integration)

Geographic coverage

⭐ (US/CA primary)

⭐⭐ (strongest EU)

⭐⭐ (US/AU/UK)

⭐ (US-focused)

Refund/chargeback handling

⭐⭐

⭐

⭐

⭐⭐

Rule of thumb: Affirm for high-ticket ($500+), Klarna for EU-heavy customer bases, Afterpay for fashion/beauty/impulse, and Skeps for maximum approval rates via multi-lender waterfall.

✅ The Right Framework: Brand Capital Decision

Match your financing model to your growth stage:

Brand Capital Decision by Revenue Stage

Revenue Stage

Recommended Model

Key Criteria

⚠️ Avoid

Pre-$1M

Bootstrap + BNPL for customers only

Do not take capital until unit economics are proven

MCA, high-fee RBF

💰 $1M to $5M

RBF or inventory financing

No personal guarantee, flexible repayment, fast disbursal

Bank loans (too slow), MCA (too expensive)

$5M to $20M

Revolving credit + RBF

Dynamic pricing vs. static rates, seasonal adaptability

Fixed-schedule providers

$20M+

Multi-source capital stack

Diversified lenders, lowest blended cost of capital

Single-provider dependency

⭐ Where Luca AI Scores on Capital Metrics

Luca AI Capital Metrics Scorecard

Capital Criterion

Luca AI Score

Why

⏰ Disbursal Speed

2/2

Same-day deployment

💰 Cost Fairness (Dynamic Pricing)

2/2

Rate drops as business health improves

Repayment Flexibility

2/2

Revenue-linked, auto-adjusts during slow months

Personal Guarantee

2/2

None required

Seasonal Adaptability

2/2

Automatic adjustment to revenue cycles

Scalability

2/2

Funding limits grow with revenue

Total

12/12

-

Luca AI scores highest on capital metrics because it was designed as a capital provider that underwrites continuously, not one that snapshots your business once and locks a rate.

The Intelligence Layer That Connects Both Decisions

For the intelligence layer that tells you when to take capital and where to deploy it, Luca's AI sits over your data warehouse, extracting root causes, predicting cash flow gaps, simulating scenarios, and pushing agentic reports to Slack and email. The capital decision and the intelligence decision are separate, but they are better when they live in the same ecosystem.

FAQ's

What is direct to consumer financing and what models are available for DTC brands?

Direct to consumer financing refers to the financial products and capital structures that enable DTC brands to either offer payment flexibility to shoppers at checkout or access growth capital without traditional bank loans or equity dilution. We see two distinct ecosystems operating simultaneously.

Consumer-facing financing includes BNPL (Buy Now, Pay Later) platforms like Klarna, Afterpay, and Affirm that split customer payments into installments. The merchant pays a Merchant Discount Rate (MDR) of 3-6% per transaction, but gains a 30-50% AOV lift and 20-30% conversion rate increase.

Brand capital financing includes revenue-based financing (RBF), merchant cash advances (MCA), inventory financing, and revolving credit lines. These models provide non-dilutive capital tied to your cash flow cycles rather than fixed monthly payments.

RBF: 6-12% flat fee, repaid as a percentage of daily or weekly revenue

MCA: 1.1-1.5x factor rate, the most expensive option available

Inventory financing: 2-8% advance fee with inventory as collateral

Most scaling DTC brands need both ecosystems working together. We help founders navigate this complexity through our financial management intelligence, which models the downstream cash impact of every financing decision before you commit.

How do you calculate the true effective APR of revenue-based financing?

The headline flat fee that most RBF providers advertise is deeply misleading without repayment timeline context. We use this formula to reveal the true cost: Effective APR = (Fee / Principal) x (365 / Days to Repay).

Here is where the math gets counterintuitive. A $200K advance at 8% flat fee ($16K total cost) produces wildly different effective APRs depending on how fast your revenue retires the balance:

Repaid in ~2.2 months (fast-growing brand): approximately 43% effective APR

Repaid in ~3.6 months (moderate growth): approximately 24% effective APR

Repaid in ~5.4 months (slower growth): approximately 16% effective APR

Repaid in just 30 days: approximately 96% effective APR

The counterintuitive reality is that faster-growing brands with higher revenue pay more in effective APR terms because the flat fee is retired in fewer days. This is why we built AI-powered cash flow forecasting directly into our capital modeling. Before you accept any advance, we simulate your actual repayment timeline against your live revenue run rate so you see the true cost in seconds, not spreadsheet hours.

What are the BNPL compliance requirements for DTC merchants in 2026?

The regulatory landscape for BNPL and commercial financing shifted significantly across every major market in 2025-2026. We track three jurisdictions that most DTC brands must navigate.

European Union: The Second Consumer Credit Directive (CCD II, Directive 2023/2225) explicitly brings BNPL within consumer credit regulation. This requires full creditworthiness assessments before approving BNPL transactions, pre-contractual cost disclosure, and a 14-day right of withdrawal. Member states must transpose CCD II into national law by November 2026.

United Kingdom: The FCA confirmed that BNPL becomes a regulated activity from 15 July 2026. Providers must obtain FCA authorization and conduct affordability checks under the Consumer Duty.

United States: While the CFPB revoked its 2024 interpretive rule classifying BNPL as credit cards, states like California (SB 1235) and New York now require APR-equivalent disclosure for commercial financing offers of $500,000 or less.

For DTC founders taking brand capital, these state laws mean your provider must disclose effective APR, not just flat fee percentages. We ensure full cost-of-capital transparency across every offer, compliant with both US commercial disclosure laws and EU consumer credit requirements.

How should DTC brands choose between BNPL providers like Klarna, Afterpay, and Affirm?

We recommend scoring each BNPL provider across six criteria that directly impact your unit economics, rather than choosing based on brand recognition alone.

MDR rate vs. gross margin: Affirm offers negotiable rates (3-6%); Afterpay runs 4-6%. Your break-even threshold is MDR% divided by AOV Lift%. At 5% MDR and 30% AOV lift, any product below 16.7% gross margin destroys value on every financed sale.

AOV lift by ticket size: Affirm performs best above $500. Afterpay excels at $50-$200 impulse purchases. Klarna is strongest in the $100-$500 range.

Consumer approval rates: Skeps uses a multi-lender waterfall for highest approval rates. Affirm runs stricter checks.

Geographic coverage: Klarna dominates EU markets. Afterpay covers US, AU, and UK. Affirm focuses on US and Canada.

Integration complexity: Klarna and Afterpay offer one-click Shopify plugins. Affirm and Skeps require heavier API integration.

The critical step most founders skip is tracking BNPL margin erosion at the product-category level, not just blended averages. We surface this granularity automatically through our unit economics tracking, so you know exactly which products profit from BNPL and which ones lose money with every financed transaction.

What emerging D2C financing trends should ecommerce founders prepare for by 2027?

We see five converging forces reshaping how DTC brands access and price capital over the next 12-18 months. The embedded lending market was valued at $9.25 billion in 2026 and is projected to reach $34.73 billion by 2033, growing at a 20.8% CAGR.

AI-driven underwriting is replacing the "apply with 60-day-old financials and wait 48 hours" model. AI-native lenders already assess business health continuously, adjusting capital offers daily based on live revenue and marketing performance.

Open banking regulations (PSD3 in EU, CFPB Section 1033 in US) enable DTC brands to share financial data directly with lenders via API, reducing approval times from days to minutes.

Embedded finance infrastructure is making checkout financing invisible. White-label BNPL, embedded credit lines, and loyalty-linked financing are becoming standard Shopify plugins.

Blockchain lending and global expansion across India (UPI + RBI frameworks), Southeast Asia (GrabPay, ShopeePay), and Latin America (Mercado Credito) are creating cross-border financing opportunities.

We already operate in this future through continuous health assessment and dynamic pricing that adjusts as your business grows. By 2027, the best DTC brands will not apply for financing; their AI layer will tell them when to take it and where to deploy it.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.svg)

.svg)

.svg)

.webp)

.png)