10 Best Revenue-Based Financing Companies: 2026 Rankings With Real Cost Breakdowns

13

mins read

TL;DR

We ranked 10 RBF providers using a weighted methodology across cost, speed, eligibility, intelligence, and user trust.

Effective APR on RBF ranges from 8% to 40% depending on repayment speed, not just the stated flat fee.

Renewal stacking can inflate blended APR by 30 to 50% versus a single properly-sized advance.

Seven red flags in RBF contracts include blanket UCC liens, confession of judgment clauses, and opaque fee disclosure.

Luca AI is the only provider combining real-time business intelligence with dynamically-priced capital tranches.

Q1. What Are the 10 Best Revenue-Based Financing Companies for E-commerce in 2026? [toc=Best RBF Companies 2026]

Revenue-based financing (RBF) gives e-commerce businesses upfront capital repaid through a fixed percentage of future revenue, typically 2% to 20%, until a predetermined repayment cap (usually 1.1x to 1.5x the funded amount) is reached. With the global RBF market projected to hit $42 billion by 2027 and AI-driven underwriting reshaping how providers assess risk, the landscape has matured well beyond the first wave of flat-fee lenders. Below are the 10 best revenue-based financing companies for 2026, ranked by a weighted methodology detailed in Q2.

Revenue-based loans up to $4M per round ($10M total), no equity or personal guarantees, monthly revenue-share repayment

SaaS startups with $15K+ MRR seeking non-dilutive growth capital

1.3x to 1.5x repayment cap; 2% to 8% revenue share

Wayflyer ⭐⭐⭐⭐

Cash advance, term loan, rolling finance; flat-fee pricing; multi-currency (USD, GBP, EUR, AUD); $5K to $20M range

E-commerce and Amazon sellers needing fast inventory/ad funding

2% to 10% flat fee on funded amount

Pipe ⭐⭐⭐⭐

Recurring revenue trading platform, embedded capital via vertical SaaS partners, no debt on balance sheet

SaaS companies converting MRR/ARR into upfront cash

Up to 1% trading fee per transaction

Clearco ⭐⭐⭐

Revenue advances, invoice funding, rolling funding capacity; performance-based pricing; no equity dilution

DTC brands needing marketing spend and inventory capital

5% to 12.5% flat fee (varies by term and use case)

Founderpath ⭐⭐⭐⭐

Revenue purchase agreements, term loans, MCAs for SaaS; AI agents for growth; 200+ five-star reviews

Bootstrapped SaaS founders wanting capital + growth tools

Discount rates from 7%; term loans from 15% APR

Outfund ⭐⭐⭐

£10K to £10M funding, revenue-share or fixed instalments, flat transparent fee, 24-hour processing

UK/EU/AU online businesses and subscription brands

2% to 6%+ flat fee depending on term and performance

Kapitus ⭐⭐⭐

Revenue-based financing, lines of credit, equipment financing; up to $5M; dedicated funding specialists

Established SMBs (2+ years, $250K+ revenue) needing working capital

Rates from 6.25%; origination fee ~2.5%

Biz2Credit ⭐⭐⭐

Revenue-based financing up to $2M+, term loans up to $1M, 24-hour approval, daily/weekly/biweekly repayment options

Small businesses with $250K+ annual revenue and 575+ credit score

3% to 8% revenue share; varies by terms

Shopify Capital ⭐⭐⭐

Merchant cash advances up to $2M for pre-qualified Shopify merchants, no application required, repay via daily sales

Shopify merchants wanting frictionless, invitation-only capital

Factor rate 1.10 to 1.17; no origination or hidden fees

🏆 1. Luca AI

✅ Why Did We Choose This Tool?

Full disclosure: I'm Eric Bidinger, founder of Luca AI, and yes, we listed ourselves first. But the ranking reflects our weighted methodology, not just founder bias. Luca AI is the only platform on this list that combines real-time business intelligence with dynamically-priced capital. Every other provider on this list offers money. We offer understanding first, then money, only when the data says it's the right move. Our AI Co-Founder architecture connects commerce, marketing, finance, and operations into a single reasoning layer, meaning capital pricing reflects your actual business health today, not a 90-day-old snapshot.

Luca AI's Revenue Based Financing intelligence dashboard serves as an AI Co-Founder for ecommerce, unifying sales analytics, ad spend modeling, inventory visibility, and embedded capital access in one conversational interface.

💡 Solutions Offered

✅ Dynamic capital pricing that adjusts in real-time based on business performance across Shopify, Meta, Stripe, and Xero data

✅ Cross-functional scenario modeling: ask "If I take €50K and deploy to Meta, what's my cash position in 90 days?" and get an answer in seconds

✅ Proactive intelligence that scans your business 24/7, surfacing capital opportunities and risks before they hit your P&L

✅ Multiple small advances (€10K to €500K) instead of one large lump sum, reducing total cost by keeping capital deployed, never idle

E-commerce founders and CFOs who want a system that tells them whether to take capital before offering it, intelligence and funding unified in one platform.

📖 Case Study

The Problem: A mid-market DTC skincare brand running €4.2M annually across Shopify and Amazon was preparing for Q4. Their existing RBF provider offered a €200K lump-sum advance at a 1.35x cap, but the founder had no visibility into whether scaling Meta spend would actually convert to profitable inventory turnover given rising CPMs.

How Luca Helped: Luca AI connected their Shopify, Meta Ads, Stripe, and Xero data, then modeled the downstream cash impact of deploying €200K to Meta versus splitting it between Meta (€120K) and inventory pre-purchase (€80K). The scenario model showed the split deployment would yield 22% better cash-on-cash return by Month 4.

The Outcome: Instead of a single €200K advance, the brand drew 4 smaller tranches (€50K each) over 8 weeks, each dynamically repriced as Q4 performance data came in. Total cost of capital was 19% lower than the original lump-sum offer, and zero capital sat idle. The brand finished Q4 with its highest-ever contribution margin.

Lighter Capital is the longest-standing pure-play RBF provider for technology companies, having deployed over $350M since 2010. Their revenue-based loan structure with a fixed repayment cap (1.3x to 1.5x) eliminates compounding interest concerns, and their willingness to fund pre-profit SaaS companies with as little as $15K MRR makes them accessible at earlier stages than most competitors.

💡 Solutions Offered

✅ Revenue-based loans up to $4M per round, with follow-on funding up to $10M total

✅ Monthly repayment tied to 2% to 8% of revenue, scaling with business performance

✅ Fixed repayment cap (1.3x to 1.5x): total cost is known upfront regardless of repayment speed

✅ No equity, no personal guarantees, no board seats required

✅ Founder community and VC network access included with financing

📊 Core Metrics

💰 Funding Range: $50K to $4M per round (up to $10M total)

📈 Revenue Share: 2% to 8% of monthly revenue

⏰ Time to Funding: 2 to 4 weeks

📋 Min Revenue: $15K MRR ($200K annual)

🌍 Geographies: US, Canada

🎯 Best For

SaaS startups with proven MRR seeking non-dilutive growth capital without giving up equity or board control.

💬 Reviews

"Lighter Capital has been a great financing partner; they funded us based on our revenue metrics when traditional banks wouldn't look at us. The repayment cap structure means no surprises. Downside: the process took about 3 weeks, which felt long when we needed capital urgently." SaaS Founder Lighter Capital - Trustpilot Verified Review

"Solid product for early-stage SaaS. The 1.3x to 1.5x cap is transparent and fair. Wish they offered faster turnaround; by the time funding arrived, we'd already missed the window on one initiative." VP Finance Lighter Capital - G2 Verified Review

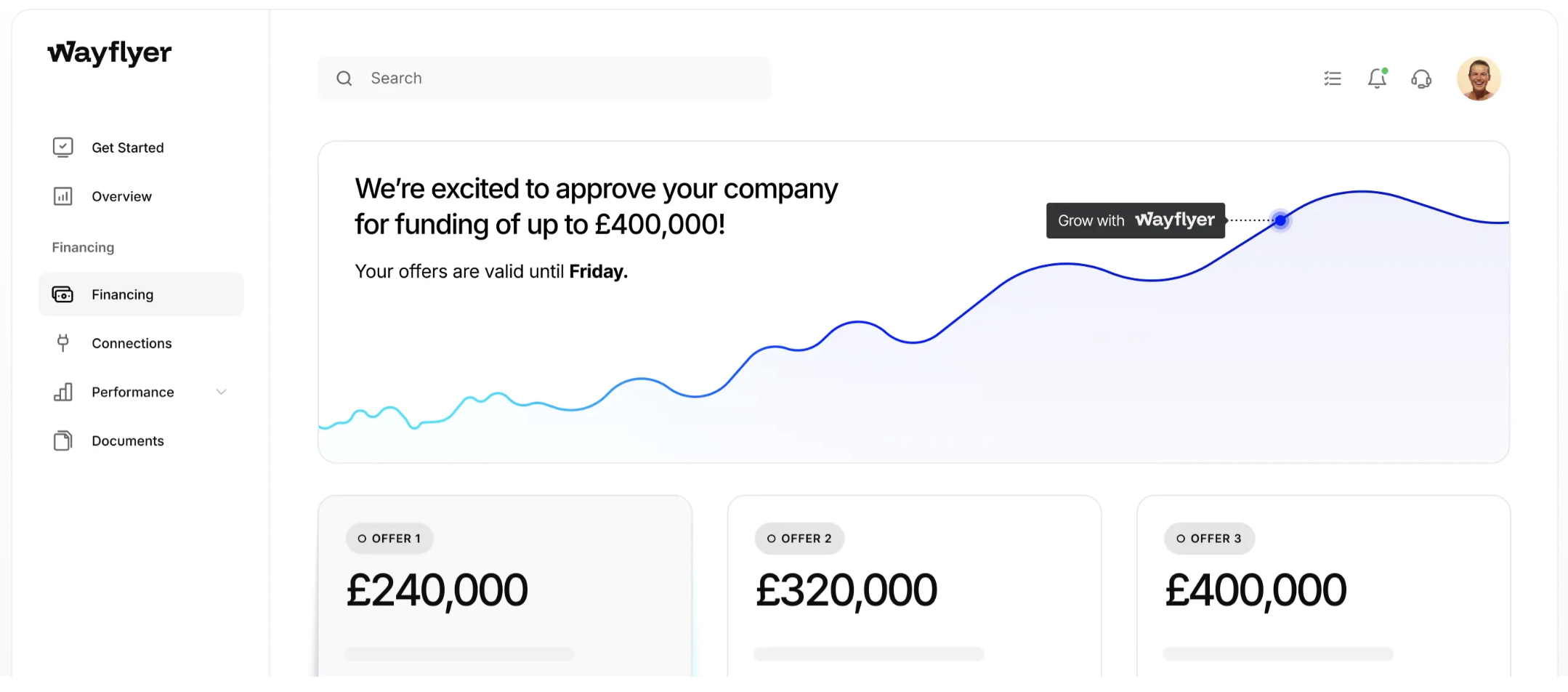

🏆 3. Wayflyer

✅ Why Did We Choose This Tool?

Wayflyer has deployed over $3.5 billion to e-commerce brands across 10+ countries, making it one of the most battle-tested RBF providers for online retail. Their flat-fee model starting at just 2% on funded amounts is among the cheapest in the industry, and their multi-currency support (USD, GBP, EUR, AUD) serves brands selling internationally.

Wayflyer's capital dashboard presents tiered funding offers alongside a revenue performance chart — approval in 24 hours with 2–9% flat fees — but underwriting is based on trailing sales snapshots with no intelligence layer to model whether scaling that campaign will tank your cash runway.

💡 Solutions Offered

✅ Three funding products: Cash Advance, Term Loan, and Rolling Finance for different growth stages

✅ Flat fees starting at 2% on funded amounts, with no compounding interest

✅ Funding range from $5K to $20M with multi-currency disbursement

✅ Revenue-share repayment that flexes with daily sales volume

✅ Integrations with Shopify, Amazon, Stripe, and other e-commerce platforms for automated underwriting

📊 Core Metrics

💰 Funding Range: $5K to $20M

📈 Fee Structure: 2% to 10% flat fee

⏰ Time to Funding: 24 to 72 hours

📋 Min Revenue: ~$20K/month

🌍 Geographies: US, UK, EU, Australia

🎯 Best For

E-commerce and Amazon sellers needing fast, affordable inventory or ad-spend funding with flexible daily repayment.

💬 Reviews

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues this was incredibly disappointing and I am frustrated that no-one reached out to us sooner to advise that they would be unable to support our business in the future." Joshua Hannan Wayflyer - Trustpilot Verified Review

"Read their terms and contract carefully! -they said their offer is not secured, which is false, they still will file UCC -they can deem you in default for any reason at their discretion... the worst bank agreement I have read in 25 years." Zachary Piech Wayflyer - Trustpilot Verified Review

🏆 4. Pipe

✅ Why Did We Choose This Tool?

Pipe pioneered the concept of trading recurring revenue streams for upfront capital without creating debt on the balance sheet. Rather than lending money, Pipe connects businesses with institutional investors who purchase future revenue at a discount, a structurally different approach that appeals to SaaS companies wanting to avoid traditional debt covenants.

💡 Solutions Offered

✅ Revenue trading platform: sell future recurring revenue to institutional investors for upfront cash

✅ Embedded capital through vertical SaaS partnerships (Boulevard, Housecall Pro, Priority)

✅ No debt created on balance sheet: revenue purchase, not a loan

✅ Platform-based underwriting using real-time SaaS metrics

✅ No personal guarantees or equity dilution required

📊 Core Metrics

💰 Funding Range: Varies by ARR (typically up to 50% of annual recurring revenue)

📈 Fee Structure: Up to 1% trading fee per transaction

⏰ Time to Funding: 1 to 5 business days

📋 Min Revenue: $5K+ MRR (varies by partner channel)

🌍 Geographies: US primarily; expanding via embedded partners

🎯 Best For

SaaS companies and subscription businesses wanting to convert MRR/ARR into immediate capital without adding debt to the books.

💬 Reviews

"I know of two startup owners that used Clearco and switched over to Pipe Capital. They say day and night difference." Terry Clearco - Trustpilot Verified Review

"Pipe's concept is smart: trade your recurring revenue instead of taking on debt. But the shift to embedded lending through SaaS partners means access depends heavily on which platforms you use. If you're not on one of their partner platforms, the experience is less straightforward now." u/SaaS_CFO_throwaway, r/SaaS Reddit Thread

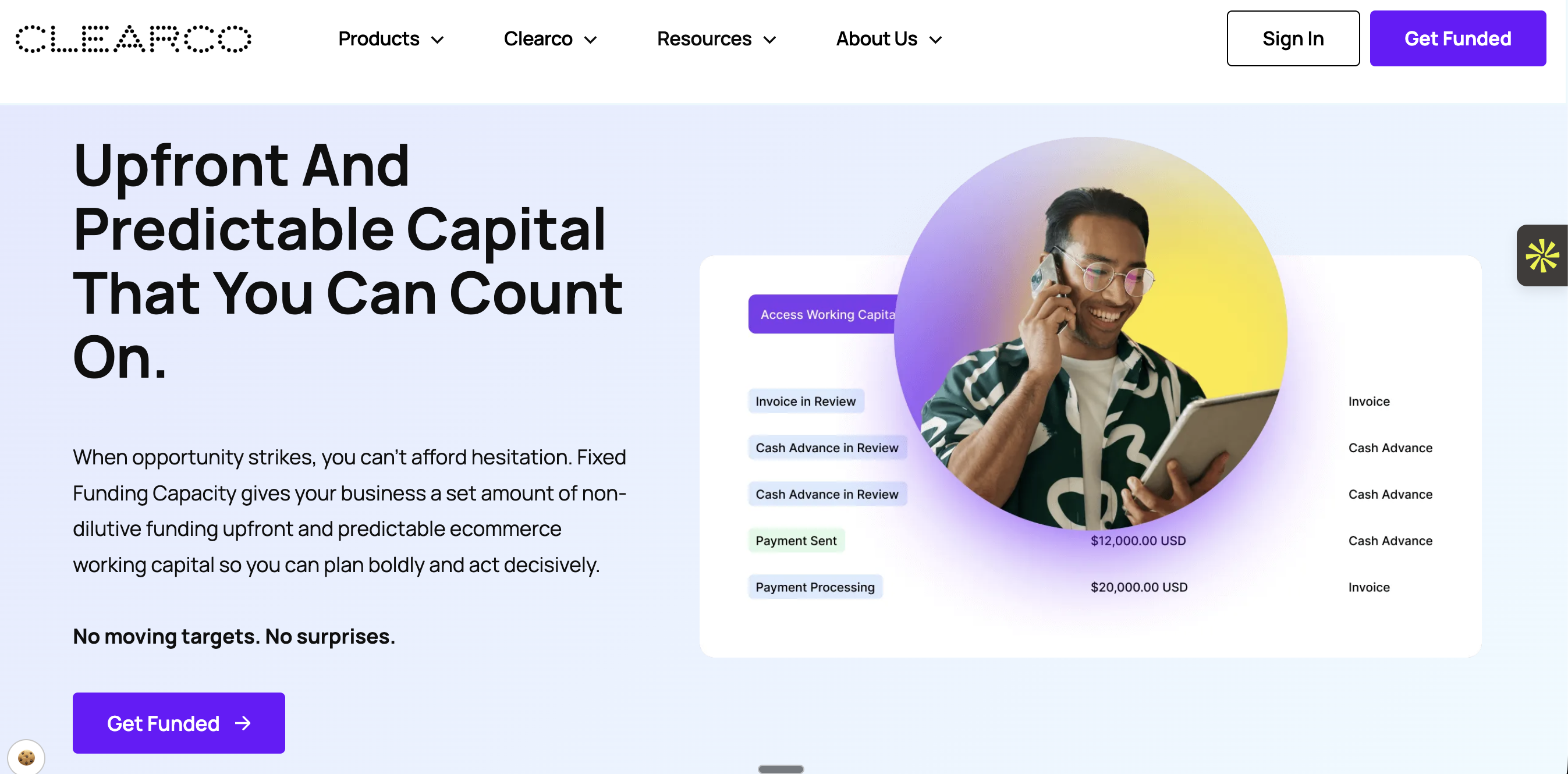

🏆 5. Clearco

✅ Why Did We Choose This Tool?

Clearco (formerly ClearBanc) was a pioneer in the "funding-as-a-service" space for DTC brands, having deployed over $4.4 billion since inception. Their 2025 relaunch introduced performance-based pricing, no equity dilution, no personal guarantees, and multiple funding structures including rolling capacity and invoice funding.

Clearco's capital dashboard tracks cash advances, invoice funding, and payment status in one view — offering 6–12% flat-fee non-dilutive funding — but multiple borrowers report that repayment deductions exceeded contracted terms, inflating the effective cost well beyond the advertised rate.

💡 Solutions Offered

✅ Revenue advances, invoice funding, fixed and rolling funding capacity

✅ Performance-based pricing that improves as business momentum grows

✅ No equity dilution, no personal guarantees, no blanket liens

✅ Predictable, capped weekly repayments

✅ Designed for digital marketing spend and inventory purchases

📊 Core Metrics

💰 Funding Range: $10K to $10M+

📈 Fee Structure: 5% to 12.5% flat fee depending on term and use case

⏰ Time to Funding: 24 to 72 hours

📋 Min Revenue: ~$10K/month online revenue

🌍 Geographies: US, Canada, UK, EU, Australia

🎯 Best For

DTC e-commerce brands using capital specifically for marketing spend and inventory purchases.

💬 Reviews

"Clearco Lost Touch With Its Own Business Model. We worked with Clearco for a couple of years and had a great experience early on. Unfortunately, things changed when our account was reassigned. Despite no change in our cash position or risk profile, and with strong recurring revenue, we started facing stricter cash-on-hand demands that made little sense for a company offering high-cost MCA." Melissa Clearco - Trustpilot Verified Review

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

🏆 6. Founderpath

✅ Why Did We Choose This Tool?

Founderpath has deployed over $200M to 500+ SaaS founders and built a reputation specifically within the bootstrapped SaaS community. Their product suite now includes revenue purchase agreements (discount rates from 7%), term loans (from 15% APR), and MCAs, alongside AI-powered growth agents that help founders increase revenue, not just access capital.

💡 Solutions Offered

✅ Revenue purchase agreements with discount rates starting at 7%

✅ Term loans starting at 15% APR with early repayment savings

✅ Merchant cash advances with repayment rates as low as 5% of monthly revenue

✅ AI growth agents for revenue optimization alongside capital

✅ Underwriting based on SaaS metrics: ARR, churn, gross margins, and retention

📊 Core Metrics

💰 Funding Range: $50K to $5M+

📈 Fee Structure: Discount rates from 7%; term loans from 15% APR

⏰ Time to Funding: 1 to 7 business days

📋 Min Revenue: $10K MRR

🌍 Geographies: US, expanding internationally

🎯 Best For

Bootstrapped SaaS founders wanting non-dilutive capital paired with growth tooling, specifically those who refuse VC but need capital to scale.

💬 Reviews

"Founderpath's approach felt genuinely aligned with our growth. The underwriting was fast, metrics-driven, and the team understood SaaS unit economics. We used the revenue advance to hire two engineers without touching equity." SaaS CEO Founderpath - G2 Verified Review

"Good rates for bootstrapped SaaS, but if your churn is above 5% monthly, the offers get thin quickly. The platform is clearly optimized for low-churn, high-retention businesses." u/bootstrapped_saas, r/SaaS Reddit Thread

🏆 7. Outfund

✅ Why Did We Choose This Tool?

Outfund has established itself as the largest revenue-based finance provider in the UK, with £115M+ raised in Series A funding and a commitment to deploy £500M+ to online businesses globally. Their flat-fee structure starting at 2% for competitive offers, flexible repayment (revenue share or fixed instalments), and 24-hour processing make them a strong option for UK and EU-based e-commerce brands.

💡 Solutions Offered

✅ Funding from £10K to £10M for online and subscription businesses

✅ Flat transparent fee starting at approximately 2% for strongest profiles

✅ Choice of revenue-share repayment or fixed instalments

✅ Daily or weekly collection via direct debit

✅ No personal guarantees required; 24-hour application processing

📊 Core Metrics

💰 Funding Range: £10K to £10M

📈 Fee Structure: ~2% to 6%+ flat fee

⏰ Time to Funding: 24 to 48 hours

📋 Min Revenue: £10K to £25K/month, 6 to 12 months trading

🌍 Geographies: UK, EU, Australia

🎯 Best For

UK, EU, and Australian online businesses needing fast, transparent non-dilutive capital with flexible repayment options.

💬 Reviews

"Outfund was straightforward: flat fee, no surprises, money in the account within 48 hours. We used it to bridge Q4 inventory purchases for our UK Shopify store. Solid experience overall." E-commerce Founder Outfund - Trustpilot Verified Review

"Applied, got approved, but the revenue share percentage felt high for our margin profile. If you're running above 40% gross margins it works well; below that, the economics get tight quickly." DTC Brand Owner Outfund - Trustpilot Verified Review

🏆 8. Kapitus

✅ Why Did We Choose This Tool?

Kapitus has provided over $7 billion in financing to 65,000+ small businesses since 2006, making it one of the most established players in the SMB lending space. Unlike most providers on this list that focus on tech or e-commerce, Kapitus serves a broad range of industries with multiple products including revenue-based financing, lines of credit, equipment financing, and SBA loans.

💡 Solutions Offered

✅ Revenue-based financing up to $5M with fixed total repayment cost

✅ Business line of credit starting at 6.25%

✅ Equipment financing for asset-heavy businesses

✅ SBA loans for qualifying small businesses

✅ Dedicated funding specialists for personalized guidance

📊 Core Metrics

💰 Funding Range: $10K to $5M

📈 Fee Structure: Rates from 6.25%; origination fee ~2.5%

⏰ Time to Funding: 24 to 72 hours

📋 Min Revenue: $250K annual; 650 credit score; 2 years in business

🌍 Geographies: US

🎯 Best For

Established small businesses (non-tech) with 2+ years of operations needing working capital, equipment financing, or flexible credit lines.

💬 Reviews

"Kapitus came through when our bank said no. The process was quick and the dedicated rep actually understood our seasonal cash flow needs. Rates aren't the cheapest, but the speed and flexibility made up for it." Small Business Owner Kapitus - Trustpilot Verified Review

"Decent option for SMBs, but the credit score requirement (650) and 2-year minimum operating history shut out a lot of newer businesses. If you qualify, it's a solid product. If you don't, there's no flexibility." Operations Manager Kapitus - G2 Verified Review

🏆 9. Biz2Credit

✅ Why Did We Choose This Tool?

Biz2Credit has built a comprehensive small-business financing marketplace processing over $131K average financing amounts, with approval in as fast as 24 hours and funding within 72 hours. Their revenue-based financing product goes up to $2M+ with one of the lowest credit score requirements in the industry (575), and their flexible repayment options (daily, weekly, or biweekly) offer more structure choices than most competitors.

💡 Solutions Offered

✅ Revenue-based financing up to $2M+ with flexible repayment schedules

✅ Term loans up to $1M for larger capital needs

✅ Daily, weekly, or biweekly repayment options, not just daily debit

✅ 60-second prequalification and 24-hour approval process

✅ Lower barrier to entry: 575 credit score, 1 year in business, $250K annual revenue

📊 Core Metrics

💰 Funding Range: $25K to $2M+

📈 Fee Structure: 3% to 8% revenue share

⏰ Time to Funding: 24 to 72 hours

📋 Min Revenue: $250K annual; 575 credit score; 1 year in business

🌍 Geographies: US

🎯 Best For

Small businesses needing accessible financing with lower credit requirements and flexible repayment scheduling.

💬 Reviews

"Clearco Lost Touch With Its Own Business Model... If you're exploring MCA options, I'd recommend checking out Biz2Credit. They offer longer terms, lower costs, and consistent monthly funding based on your revenue, without demanding invasive access to your platforms." Melissa Clearco - Trustpilot Verified Review

"Biz2Credit's application was genuinely fast: prequalified in under 2 minutes, funded in 3 days. The rep was helpful. Only gripe: the total cost of capital wasn't crystal clear upfront; I had to calculate the effective APR myself." Business Owner Biz2Credit - Trustpilot Verified Review

🏆 10. Shopify Capital

✅ Why Did We Choose This Tool?

Shopify Capital has funded over $5 billion to Shopify merchants, making it the most frictionless RBF option for businesses already on the Shopify platform. There is no application process: Shopify pre-qualifies merchants based on store performance and presents offers directly in the Shopify admin dashboard. Factor rates of 1.10 to 1.17 make it one of the cheapest merchant cash advance products available.

Shopify Capital's funding dashboard surfaces pre-qualified offers directly inside your Shopify admin — zero application, zero credit check — but funds only Shopify-channel revenue while ignoring Amazon, wholesale, and every other sales channel.

💡 Solutions Offered

✅ Merchant cash advances up to $2M for pre-qualified Shopify sellers

✅ No application required: offers appear in Shopify admin based on store performance

✅ Factor rates of 1.10 to 1.17 with no origination or hidden fees

✅ Repayment via automatic percentage of daily Shopify sales

✅ No early repayment penalties; total cost fixed upfront

📊 Core Metrics

💰 Funding Range: ~$200 to $2M (based on processing volume)

📈 Fee Structure: Factor rate 1.10 to 1.17 (10% to 17% flat cost)

⏰ Time to Funding: 1 to 3 business days after acceptance

📋 Min Revenue: Invitation-only based on Shopify sales history

🌍 Geographies: US, UK, Canada, Australia

🎯 Best For

Active Shopify merchants wanting the simplest possible capital access with transparent, low-cost pricing: no applications, no negotiation.

💬 Reviews

"Shopify Capital is the easiest money I've ever accessed: the offer just showed up in my dashboard, I clicked accept, and funds hit my account in 2 days. The factor rate was fair. Only issue: you can't request it. You wait for them to offer." Shopify Merchant Shopify Capital - Trustpilot Verified Review

"Great for small amounts and convenience. But once you need more than what they offer or want to negotiate terms, you're stuck. There's no conversation, no flexibility: it's take-it-or-leave-it. For larger capital needs, you'll outgrow Shopify Capital quickly." E-commerce Founder, r/shopify Reddit Thread

Methodology note: Star ratings reflect weighted scoring across Cost Transparency (25%), Funding Speed (20%), Eligibility Flexibility (15%), Intelligence and Decision Support (25%), and User Trust (15%). Full scoring breakdown in Q2 below.

Q2. How Were These Revenue-Based Financing Companies Scored and Ranked? [toc=Scoring Methodology]

Transparency matters when a ranked list influences capital decisions. Every provider on this list was evaluated using a consistent, weighted methodology designed to reflect what actually matters to e-commerce founders choosing between RBF options, not just who offers the cheapest headline fee, but who helps you make a smarter decision with that capital.

📊 Five Evaluation Criteria

RBF Evaluation Criteria

Criteria

Weight

What It Measures

💰 Cost Transparency & Fee Structure

25%

Clarity of pricing, effective APR disclosure, absence of hidden origination fees or opaque multipliers

⏰ Funding Speed & Accessibility

20%

Time from application to funds in account; friction in the approval process

📋 Eligibility Flexibility

15%

Minimum revenue thresholds, credit score requirements, business model and geography coverage

🧠 Intelligence & Decision Support

25%

Whether the provider helps you assess if funding is the right move, not just offers capital blindly

⭐ User Reviews & Trust

15%

Aggregated sentiment from Trustpilot, G2, Reddit, weighted toward recency and verified users

Total: 100%

⭐ Star Rating Mapping

Scores were calculated per provider across all five criteria, then converted to a 5-star scale:

Score to Star Conversion

Score Range

Star Rating

0 to 20

⭐

21 to 40

⭐⭐

41 to 60

⭐⭐⭐

61 to 80

⭐⭐⭐⭐

81 to 100

⭐⭐⭐⭐⭐

Provider Star Ratings

Provider

Star Rating

Luca AI

⭐⭐⭐⭐⭐

Lighter Capital

⭐⭐⭐⭐

Wayflyer

⭐⭐⭐⭐

Pipe

⭐⭐⭐⭐

Clearco

⭐⭐⭐

Founderpath

⭐⭐⭐⭐

Outfund

⭐⭐⭐

Kapitus

⭐⭐⭐

Biz2Credit

⭐⭐⭐

Shopify Capital

⭐⭐⭐

✅ Why RBF Works, and Where It Doesn't

Consolidated Pros:

✅ Non-dilutive: no equity surrendered, no board seats granted

✅ Flexible repayment that scales with revenue, easing cash flow pressure during slow months

✅ Fast access: most providers fund within 24 to 72 hours versus 6 to 8 weeks for bank loans

✅ No personal guarantees required by most top providers

✅ Cash-flow aligned: repayments shrink when revenue dips

Consolidated Cons:

❌ Higher effective cost than traditional bank loans (typical effective APR ranges from 15% to 40%)

❌ Revenue dependency: pre-revenue or declining businesses don't qualify

❌ Risk of over-leveraging through renewal stacking (covered in detail in Q4)

❌ Limited to businesses with demonstrable, recurring, or consistent revenue

🧠 The Intelligence Gap

Most providers score competitively on Speed and Eligibility but fall short on Intelligence & Decision Support, the criterion carrying 25% of the total weight. Traditional RBF providers offer capital as a commodity: they assess whether they should lend, not whether you should borrow. Only Luca AI scores maximum on this criterion because it reasons across your commerce, marketing, and financial data to model the downstream impact of taking capital before offering it. That architectural difference, intelligence before capital, not capital without context, is what separates a 5-star provider from the rest.

Q3. Provider-by-Provider Breakdown: Fees, Speed, Eligibility, Category Picks, and Real User Reviews [toc=Provider Breakdown and Reviews]

The master comparison table below distills the 10 providers across 8 critical dimensions. Use it as a quick-reference before diving into the category picks and review evidence that follows.

📊 Master Comparison Table

Provider-by-Provider Comparison Across 8 Dimensions

Provider

Revenue Share %

Fee Type

Max Funding

Speed

Min Revenue

Credit Req

Geographies

Best For

Luca AI

Dynamic

Real-time pricing

€500K

Same day

€1M/yr

None

EU, UK

Intelligence-led capital

Lighter Capital

2% to 8%

Repayment cap 1.3x to 1.5x

$4M/round

2 to 4 weeks

$15K MRR

None

US, CA

SaaS growth capital

Wayflyer

N/A

2% to 10% flat fee

$20M

24 to 72 hrs

~$20K/mo

None

US, UK, EU, AU

E-commerce speed funding

Pipe

N/A

~1% trading fee

Varies by ARR

1 to 5 days

$5K MRR

None

US

SaaS revenue trading

Clearco

N/A

5% to 12.5% flat fee

$10M+

24 to 72 hrs

~$10K/mo

None

US, CA, UK, EU, AU

DTC ad spend & inventory

Founderpath

5%+

Discount from 7%; loans from 15% APR

$5M+

1 to 7 days

$10K MRR

None

US

Bootstrapped SaaS

Outfund

N/A

2% to 6%+ flat fee

£10M

24 to 48 hrs

£10K to £25K/mo

None

UK, EU, AU

UK/EU online businesses

Kapitus

N/A

From 6.25%

$5M

24 to 72 hrs

$250K/yr

650

US

Established SMBs

Biz2Credit

3% to 8%

Revenue share

$2M+

24 to 72 hrs

$250K/yr

575

US

Flexible SMB financing

Shopify Capital

N/A

Factor rate 1.10 to 1.17

$2M

1 to 3 days

Invitation only

None

US, UK, CA, AU

Shopify-native merchants

🏆 Category Winner Picks

Best for SaaS: Lighter Capital, purpose-built for recurring revenue businesses with no equity or personal guarantees, and follow-on funding up to $10M total

Best for E-commerce: Wayflyer, $5K to $20M range with multi-currency support and flat fees starting at 2%, though user reviews flag inconsistent underwriting decisions

Best for SMB (Non-Tech): Kapitus, broad product suite (RBF, lines of credit, equipment financing, SBA loans) with $7B+ deployed to 65,000+ businesses

Best for International/Europe: Outfund, UK's largest RBF provider with £115M+ Series A, serving UK, EU, and Australian online businesses

Best for Fastest Funding: Shopify Capital, no application required, offers appear in your Shopify admin, funds arrive in 1 to 3 days after acceptance

Best for Large Checks: Pipe, revenue trading model with no fixed ceiling, scaling with your ARR rather than capping at a predetermined amount

Best for Bootstrapped Founders: Founderpath, built specifically for the bootstrapped SaaS community with 500+ founders funded and AI growth agents included alongside capital

⚠️ What Real Users Are Saying

The review landscape across Trustpilot, G2, and Reddit reveals a consistent pattern: most RBF providers earn praise for initial onboarding speed but face criticism on post-funding support, pricing transparency, and renewal reliability.

Wayflyer drew pointed criticism for opaque contract terms. One merchant reported discovering blanket UCC filings despite being told the offer was unsecured:

"Read their terms and contract carefully! -they said their offer is not secured, which is false, they still will file UCC -they can deem you in default for any reason at their discretion... the worst bank agreement I have read in 25 years." Zachary Piech Wayflyer - Trustpilot Verified Review

Clearco users flagged accelerated fund withdrawals that increased effective interest rates beyond what contracts stated:

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Verified Review

A Clearco user also calculated the true cost of their advance at approximately 35 to 40% APR after accounting for weekly repayment mechanics:

"Pretty expensive product at 35-40 APR. Even worse support... 6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% / 4 months = 12 months = 36% APR." Julian Fernau Clearco - Trustpilot Verified Review

These patterns reinforce why Intelligence & Decision Support carries 25% of our scoring weight. Capital without context leaves founders to discover cost surprises after the contract is signed.

Q4. What Does Revenue-Based Financing Actually Cost? Real Scenarios, Effective APR, and the Renewal Trap [toc=True RBF Cost Analysis]

The headline fee on an RBF offer rarely tells the full story. A "6% flat fee" or "1.3x repayment cap" can translate into wildly different effective costs depending on how quickly you repay, and most providers have no incentive to help you understand that math before you sign.

💰 Three RBF Pricing Models Explained

RBF Pricing Models Compared

Pricing Model

How It Works

Example on $500K

Typical Providers

Factor Rate (1.2x to 1.5x)

Total repayment = Advance x Factor Rate, regardless of time

$500K x 1.3 = $650K total repayment

Shopify Capital, Kapitus

Flat Fee % (6% to 12%)

One-time fee on funded amount; repaid via revenue share

$500K x 8% = $40K fee; repay $540K total

Wayflyer, Clearco, Outfund

Revenue Share % (2% to 15% of monthly revenue) until cap

Fixed % of monthly revenue until repayment cap hit

8% of revenue/month until $650K repaid (1.3x cap)

Lighter Capital, Biz2Credit

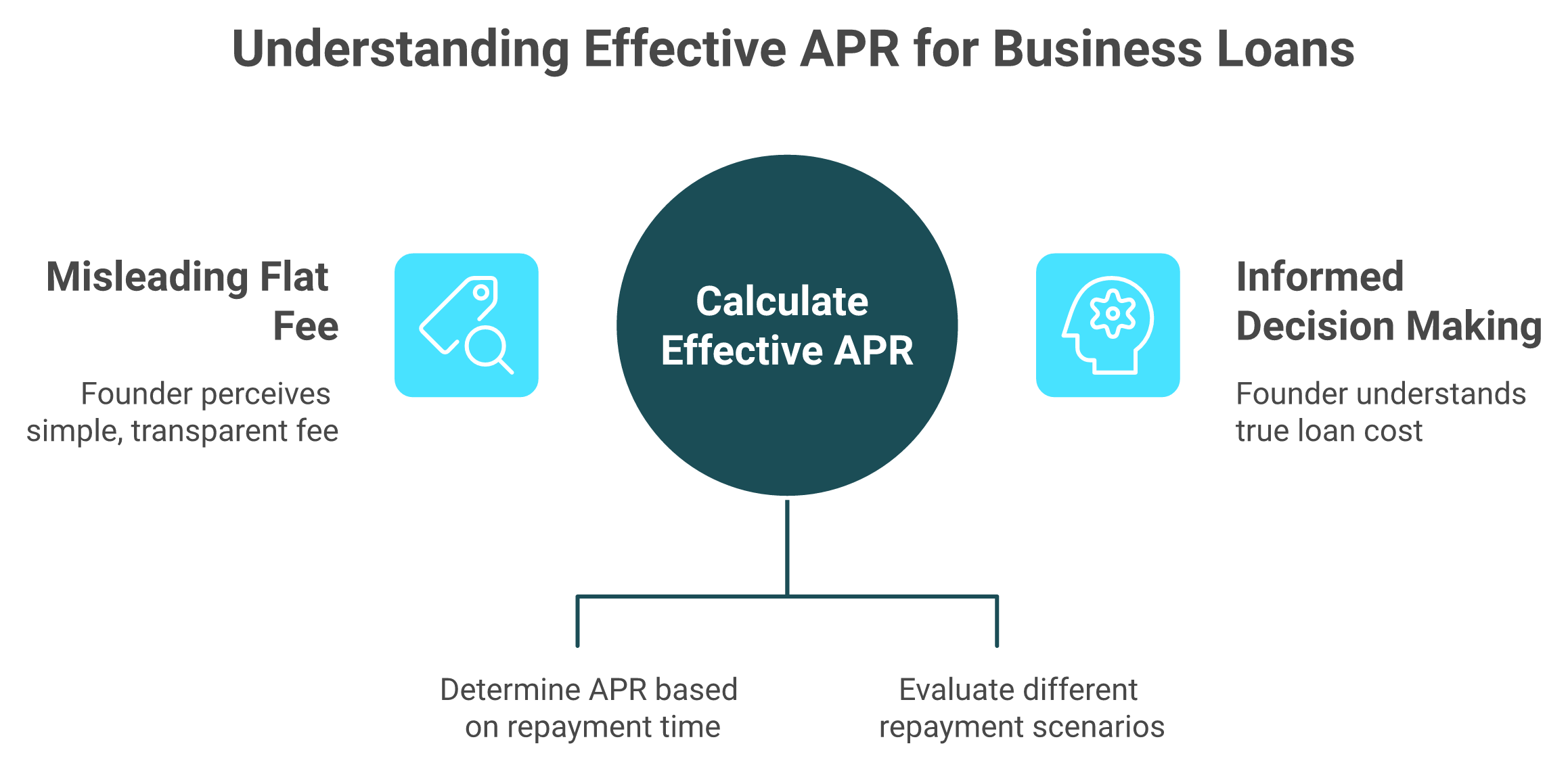

📈 Why Effective APR Matters More Than Stated Fee

A 10% flat fee sounds simple: you borrow $500K and repay $550K. But if you repay that in 3 months, your annualized cost exceeds 40%. If it takes 12 months, the effective APR drops to roughly 10 to 12%. Most providers don't disclose this distinction. Effective APR is calculated by annualizing the total cost relative to the average outstanding balance over the repayment period. The faster you repay, the higher the annualized rate because you held the capital for less time.

The headline flat fee on an RBF offer masks the true effective APR, which shifts dramatically depending on how quickly you repay the advance.

📊 $500K RBF Deal: Three Revenue Scenarios

Assumptions: $500K advance, 8% flat fee ($540K total repayment), 10% revenue share on monthly revenue starting at $200K/month.

$500K RBF Cost Across Revenue Scenarios

Scenario

Monthly Revenue Trend

Months to Repay

Total Paid

Effective APR

A: Growing Revenue (+5%/month)

$200K to $310K

~7 months

$540K

~14%

B: Flat Revenue (steady)

$200K constant

~9 months

$540K

~11%

C: Declining Revenue (-3%/month)

$200K to $152K

~13 months

$540K

~8%

The counterintuitive insight: declining revenue produces a lower effective APR because you hold the money longer, but your business is suffering while repayment drags on. The "cheapest" scenario on paper is often the worst outcome in practice.

⚠️ The Renewal Trap: How Stacking Compounds Cost

This is where most founders get caught. You take a $200K advance at a 1.3x cap ($260K repayment). Six months in, with $130K still outstanding, you take a second advance of $150K at 1.3x ($195K repayment). You now owe $325K total, but because both advances run concurrently with revenue share deductions, your effective cash available for operations shrinks dramatically.

Single $200K advance: Total cost = $60K (the 0.3x premium)

Stacked ($200K + $150K at month 6): Blended total cost = $105K, but average capital actually available is lower because of overlapping repayment streams

Effective blended APR jumps 30% to 50% compared to a single, properly-sized advance

Renewal stacking is the RBF industry's quiet margin expander. Providers benefit from encouraging early refinancing because it generates new fees on partially-repaid capital. This is precisely why understanding your unit economics before taking on additional capital is critical.

Renewal stacking is the RBF industry's quiet margin expander, nearly doubling your total cost of capital while shrinking available cash from overlapping repayment streams.

✅ Luca AI's Dynamic Alternative

The same $500K capital need drawn through Luca AI looks structurally different. Instead of one lump sum, you draw 5 to 8 smaller advances (€50K to €100K each) over weeks, each dynamically priced based on real-time business health at the moment of disbursement. Capital that isn't needed yet isn't drawn, so it never accrues cost. As performance improves, subsequent tranches price more favorably.

✅ No idle capital sitting in your account accruing cost you don't need yet

✅ Pricing improves as your data shows stronger performance

✅ Scenario modeling built in: Luca shows the cash flow impact of each advance before you accept it

❌ Traditional lump-sum providers: full cost begins accruing on day one, regardless of whether you've deployed the capital

The result: total cost of capital typically runs 15% to 25% lower than equivalent lump-sum offers, because you're only paying for capital when, and if, the data says it's the right time to deploy.

Q5. What Are the Red Flags of Predatory RBF Terms, and How Should You Read a Term Sheet? [toc=Red Flags and Term Sheets]

Not all revenue-based financing is founder-friendly. The industry's low regulatory barrier means some providers use opaque fee structures, aggressive collection mechanisms, and contract clauses that can trap businesses in cycles of escalating cost. Knowing what to look for before you sign is the difference between growth capital and a financial liability.

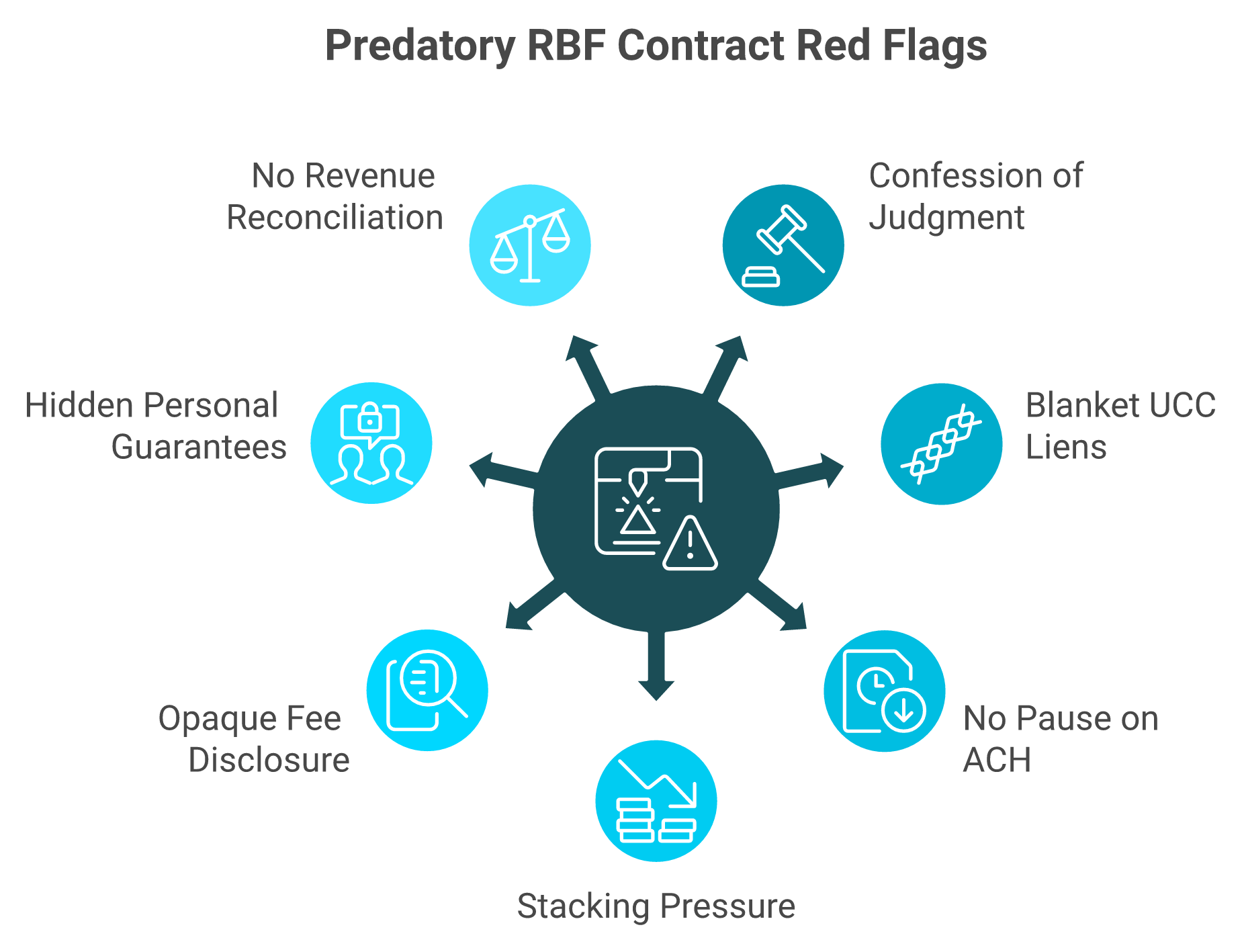

Before signing any RBF term sheet, scan for these seven red flags that separate founder-friendly financing from predatory contract structures.

⚠️ 7 Red Flags in RBF Contracts

Confession of Judgment clauses allows the provider to seize your assets or freeze accounts without court proceedings. You waive your right to defend yourself before a judgment is entered.

Blanket UCC liens on all business assets not just your receivables. Some providers file UCC-1 liens that cover inventory, equipment, and intellectual property, even when the advance is structured as a revenue purchase. One merchant discovered this the hard way:

"Read their terms and contract carefully! -they said their offer is not secured, which is false, they still will file UCC -they can deem you in default for any reason at their discretion... -they can enter your building and take your property in excess of the value of what is owed. -they can redirect your Shopify funds to their account." Zachary Piech Wayflyer - Trustpilot Verified Review

Daily ACH withdrawals with no pause mechanism repayment continues at the same rate even during revenue dips, with no reconciliation process to reduce withdrawals when sales slow down.

Auto-renewal or stacking encouragement providers that push a second advance before the first is repaid, compounding your total cost (detailed in Q4).

Opaque fee disclosure with no effective APR a "6% flat fee" that actually translates to 35 to 40% APR once weekly repayment mechanics are factored in. One user calculated this firsthand:

"Pretty expensive product at 35-40 APR. Even worse support... 6% for 4 months extension does not sound like a lot. Since you have to pay back weekly immediately, you will have less than half of the money on average available over the 4 months. That puts you to 12% / 4 months = 12 months = 36% APR." Julian Fernau Clearco - Trustpilot Verified Review

Mandatory personal guarantees disguised as standard some contracts include director indemnity clauses that function as personal guarantees while marketing the product as "no PG required."

No reconciliation when revenue drops true RBF should flex with your revenue. If your contract has fixed daily or weekly debits regardless of sales performance, it's structurally closer to a merchant cash advance.

📋 How to Read an RBF Term Sheet

Every RBF term sheet contains clauses that directly impact your total cost and operational flexibility. Here's what to look for in plain English:

RBF Term Sheet Clause Guide

Clause

What It Means

What to Negotiate

Revenue Share %

The percentage of monthly/daily revenue deducted for repayment (typically 2% to 15%)

Lower is better; push below 10% if possible

Repayment Cap / Multiple

Total amount you'll repay (e.g., 1.3x means $130K on a $100K advance)

Insist on a fixed cap; reject uncapped multiples

Term Length

Maximum repayment window before penalties or acceleration

Longer terms = lower effective APR

Default Triggers

Events that let the provider accelerate full repayment

Remove subjective triggers ("any material change")

Early Repayment

Penalties or discounts for paying off early

Request a discount (5 to 10% fee reduction) for early payoff

UCC Filing Scope

What assets the lien covers

Limit scope to receivables only, not all business assets

Origination Fees

Upfront fees deducted before you receive funds

Demand full transparency; calculate into effective APR

✅ How Luca AI Handles This Differently

At Luca AI, we model the exact total repayment, effective APR, and cash flow impact against your real business data before you accept any advance. There are no blanket UCC liens, no confession of judgment clauses, and no stacking pressure, because the same system that recommends capital also models the risk of taking it. If the data says an advance would strain your cash position, Luca tells you to wait rather than pushing capital you don't need.

Q6. RBF vs. Venture Capital, Bank Loans, and MCAs, and Which Business Type Should Choose What? [toc=RBF vs Other Financing]

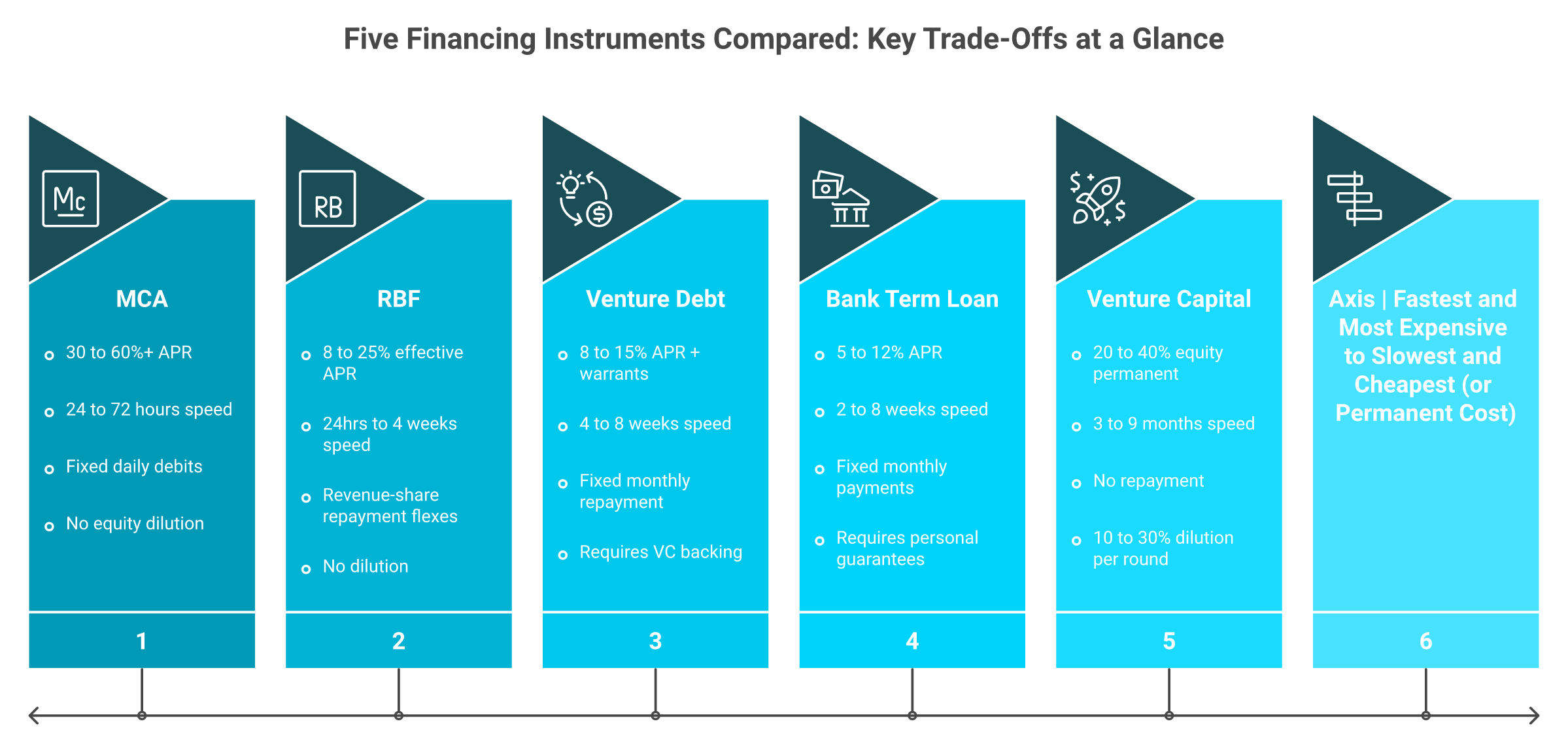

Choosing the wrong financing instrument costs more than just money; it costs equity, time, or operational flexibility you can't recover. Founders evaluating RBF are typically weighing it against four alternatives: venture capital, bank term loans, venture debt, and merchant cash advances. Each has a structurally different cost, speed, and trade-off profile.

Every financing instrument sits on a cost-speed spectrum. RBF occupies the middle ground: faster than bank loans and VC, cheaper than MCAs, and fully non-dilutive.

📊 Financing Alternatives Compared

Financing Alternatives Comparison

Factor

RBF

Venture Capital

Bank Term Loan

Venture Debt

MCA

💸 Equity Dilution

None

10 to 30% per round

None

Warrants (1 to 3%)

None

💰 Typical Cost

8 to 25% effective APR

20 to 40% equity (permanent)

5 to 12% APR

8 to 15% APR + warrants

30 to 60%+ effective APR

⏰ Speed

24 hrs to 4 weeks

3 to 9 months

2 to 8 weeks

4 to 8 weeks

24 to 72 hours

📋 Repayment

Revenue-share (flexes)

No repayment (equity is permanent)

Fixed monthly

Fixed monthly

Fixed daily debit

🎯 Best For

Revenue-stage growth capital

Pre-revenue, massive scale

Asset-heavy, strong credit

VC-backed, need bridge

Urgent cash, any credit

⚠️ Biggest Risk

Higher cost if revenue grows fast

Permanent dilution

Personal guarantees

Warrants + covenants

Aggressive daily debits

🔍 Key Distinctions Often Confused

RBF vs. MCA: Both are non-dilutive and fast, but structurally different. RBF ties repayment to a percentage of revenue; when sales dip, repayment shrinks. MCAs typically take fixed daily debits regardless of revenue performance, creating severe cash flow strain during slow periods. Effective APR on MCAs often exceeds 40 to 60%, roughly double the cost of most RBF products.

RBF vs. Venture Debt: Venture debt is cheaper (8 to 15% APR) but requires existing VC backing, often includes warrant coverage (1 to 3% equity), and demands collateral. RBF requires none of these, but costs more in total repayment.

RBF vs. VC: No dilution, no board seats, no 9-month fundraising process. But also no strategic network, no follow-on signaling, and no massive check sizes. RBF is capital, not a partnership.

🎯 Which Business Type Should Choose What?

Financing Recommendation by Business Type

Business Type

Recommended Financing

Why

Top Providers

E-commerce / DTC

RBF

Inventory financing, ad spend scaling, Q4 preparation; revenue aligns with repayment

For e-commerce brands, timing capital deployment correctly is as important as choosing the right provider:

8 to 10 weeks before Q4 draw RBF for inventory pre-purchase when supplier lead times are longest

4 to 6 weeks before peak deploy ad spend capital when CPMs haven't yet spiked but audience targeting is set

Avoid drawing post-peak taking RBF in January to cover Q4 shortfalls means you're paying for capital during your lowest revenue months, extending repayment and increasing effective cost

✅ Where Luca AI Fits in This Decision

Luca AI is the only provider on this list that doesn't just offer capital; it models which financing type is optimal for your specific business at this specific moment. Ask "Should I take RBF now or wait for my bank loan approval?" and get a scenario-modeled answer in seconds, built from your real Shopify, Stripe, Meta, and Xero data. The system that provides the capital also provides the framework for deciding whether to take it.

Q7. People Also Ask: Revenue-Based Financing for E-commerce and SaaS [toc=RBF FAQs]

What is revenue-based financing?

Revenue-based financing (RBF) is a funding model where a business receives upfront capital in exchange for a fixed percentage of its future monthly revenue until a predetermined repayment cap is reached. Unlike traditional loans, there are no fixed monthly payments; repayment scales with your actual sales, making it inherently flexible for businesses with variable revenue.

How much does RBF cost?

The effective cost of RBF ranges widely depending on provider, amount, and repayment speed. Flat fees typically range from 2% to 12% of the funded amount, while repayment caps (factor rates) range from 1.1x to 1.5x. Translated to effective APR, most RBF products fall between 8% and 30%, though some providers with weekly repayment structures can exceed 35 to 40% effective APR once the average outstanding balance is factored in.

Is revenue-based financing a loan?

Technically, no. Most RBF products are structured as a purchase of future revenue, not a debt instrument. This distinction matters for accounting (it may not appear as debt on your balance sheet), tax treatment, and legal protections. However, some providers, particularly those using fixed daily debits or confession-of-judgment clauses, operate closer to merchant cash advances despite marketing themselves as RBF.

Can startups with no revenue get RBF?

No. RBF requires demonstrated, consistent revenue as the basis for both underwriting and repayment. Most providers require minimum monthly revenue between $10K and $50K, with at least 6 to 12 months of trading history. Pre-revenue startups should explore equity financing (angel investors, VC) or grants instead.

How fast can I get RBF funding?

Speed varies significantly by provider. Shopify Capital can fund within 1 to 3 business days since there's no application; offers appear automatically. Wayflyer and Clearco typically fund within 24 to 72 hours after connecting e-commerce platforms. Lighter Capital, which performs deeper SaaS-specific underwriting, takes 2 to 4 weeks. Luca AI deploys capital same-day because underwriting is continuous and real-time, not application-based.

Does RBF affect my credit score?

Most RBF providers perform only a soft credit pull during the application process, which does not impact your personal credit score. However, some providers file UCC-1 liens against your business assets, which can appear on business credit reports and affect your ability to secure other financing simultaneously.

What's the difference between RBF and a merchant cash advance?

RBF and MCAs are often confused but differ structurally. RBF ties repayment to a percentage of revenue; if your sales drop 30%, your repayment drops proportionally. MCAs typically require fixed daily or weekly debits regardless of revenue performance, creating cash flow pressure during slow periods. MCAs also tend to carry higher effective costs (30 to 60%+ APR equivalent) compared to RBF (8 to 30% effective APR).

How does Luca AI's RBF differ from traditional providers?

Traditional RBF providers offer capital based on static, historical revenue snapshots; they assess whether they should lend, not whether you should borrow. Luca AI inverts this model by combining real-time business intelligence with dynamic capital. Before offering funding, Luca models the downstream cash flow impact of taking capital, prices each advance based on current business health (not 90-day-old data), and deploys in smaller tranches to reduce total cost. The result: you receive both the capital and the strategic confidence to deploy it correctly.

FAQ's

How do we choose the right revenue-based financing provider for our e-commerce business?

We recommend evaluating RBF providers across five weighted criteria: cost transparency, funding speed, eligibility flexibility, intelligence and decision support, and user trust. The most common mistake founders make is optimizing solely for the lowest headline fee without considering whether the provider helps them assess if funding is even the right move at this moment.

Cost transparency: Does the provider disclose effective APR, or only a flat fee percentage?

Funding speed: Can you access capital within 24 to 72 hours, or does underwriting take weeks?

Intelligence layer: Does the provider model your downstream cash flow impact before offering capital?

Contract terms: Are there blanket UCC liens, confession of judgment clauses, or auto-renewal pressure?

We built Luca AI's financial management tools specifically to solve this gap. Our system reasons across your Shopify, Stripe, Meta, and Xero data to model whether capital deployment will actually improve your cash position before you accept any advance. The provider that offers the cheapest rate is not always the provider that produces the best outcome for your business.

What is the real effective APR on revenue-based financing for startups?

The effective APR on revenue-based financing typically ranges from 8% to 30%, but it can exceed 35 to 40% with certain providers that use weekly repayment structures. The stated flat fee (often 6% to 12%) is misleading because effective APR depends on how quickly you repay the advance.

Here is the core math most providers do not disclose: if you borrow $500K at an 8% flat fee ($540K total repayment) and repay through a 10% monthly revenue share, your effective APR shifts dramatically based on revenue trajectory.

Growing revenue (+5%/month): Repaid in roughly 7 months at approximately 14% effective APR.

Flat revenue: Repaid in roughly 9 months at approximately 11% effective APR.

Declining revenue (-3%/month): Repaid in roughly 13 months at approximately 8% effective APR, but your business is deteriorating.

We designed our unit economics tracking approach to give founders visibility into these true cost dynamics before signing any term sheet. The cheapest APR on paper often correlates with the worst business outcome in practice.

Is revenue-based financing better than venture capital for e-commerce brands?

For most revenue-stage e-commerce brands, RBF is structurally better than venture capital for specific use cases like inventory financing, ad spend scaling, and Q4 preparation. RBF requires no equity dilution, no board seats, and funds within 24 hours to 4 weeks versus 3 to 9 months for a typical VC round.

However, the trade-offs are real:

RBF advantage: Non-dilutive, fast, cash-flow aligned repayment, no personal guarantees with most top providers.

RBF limitation: Higher cost if revenue grows fast (8 to 25% effective APR versus zero repayment on equity).

VC limitation: Permanent 10 to 30% dilution per round plus loss of operational control.

We help founders navigate this decision through AI-powered cash flow forecasting that models both scenarios against real business data. Pre-revenue startups should pursue VC or angel funding since RBF requires demonstrated, consistent revenue to qualify.

What are the biggest red flags in a revenue-based financing contract?

We have identified seven critical red flags that separate founder-friendly RBF from predatory financing structures. Spotting these before you sign can save your business from escalating cost cycles and operational constraints.

Confession of Judgment clauses: The provider can seize assets or freeze accounts without court proceedings.

Blanket UCC liens: Liens covering all business assets (inventory, equipment, IP), not just receivables.

Daily ACH withdrawals with no pause mechanism: Fixed debits continue even when revenue drops.

Auto-renewal or stacking encouragement: Pushing a second advance before the first is repaid, compounding total cost by 30 to 50%.

Opaque fee disclosure: A stated 6% flat fee that translates to 35 to 40% effective APR once weekly repayment mechanics are factored in.

At Luca AI, we model exact total repayment, effective APR, and cash flow impact against your real business data before you accept any advance. There are no blanket UCC liens, no confession of judgment clauses, and no stacking pressure in our structure.

How does non-dilutive financing through RBF work for SaaS and e-commerce companies?

Non-dilutive financing through RBF works by providing upfront capital in exchange for a fixed percentage of future monthly revenue (typically 2% to 15%) until a predetermined repayment cap (usually 1.1x to 1.5x the funded amount) is reached. Unlike equity financing, you surrender zero ownership, no board seats, and maintain full operational control.

The repayment structure is inherently flexible:

When monthly revenue increases, you repay faster but at a higher effective APR.

Total cost is capped upfront, unlike interest-bearing loans that compound over time.

For SaaS companies, providers like Lighter Capital and Pipe offer terms based on MRR and ARR metrics. For e-commerce brands, providers like Wayflyer and Shopify Capital underwrite based on platform sales data. We built our intelligence-capital thesis around the principle that the best non-dilutive capital is capital paired with real-time decision support, so you deploy funds only when and where the data confirms a positive return.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.png)