12 Best Working Capital Loans for Ecommerce Businesses in 2026 (With Comparison Table)

14

mins read

TL;DR

We ranked 12 ecommerce working capital lenders across platform-embedded, fintech, and traditional categories with true cost scenarios.

Flat fees mask real APR; a 6% fee on a 4-month MCA translates to roughly 36% annualized cost.

We introduce a seasonal capital stacking framework and CCC formula to time draws for maximum ROI.

Luca AI is the only lender combining working capital with deployment ROI modeling before you sign.

Hidden fee red flags include origination charges, UCC liens, prepayment lockouts, and fund redirection clauses.

Q1. What Are the 12 Best Working Capital Loans for Ecommerce Businesses in 2026? [toc=Best Working Capital Loans]

Ecommerce businesses face a structural cash flow problem that traditional retail does not: marketplace payouts are delayed 1 to 14 days, inventory must be purchased 60 to 90 days before it sells, and ad spend hits your account today while revenue trickles in over weeks. These timing mismatches create working capital gaps that widen during seasonal peaks like BFCM and Prime Day. The 12 lenders below span three categories: platform-embedded, ecommerce-specialized fintech, and traditional/government-backed, each solving a different piece of this puzzle.

Luca AI Best for intelligence-backed capital with deployment ROI modeling

Shopify Capital Best for Shopify-native merchants needing same-day MCA

Amazon Lending Best for FBA sellers scaling inventory

PayPal Working Capital Best for PayPal-heavy sellers with flexible repayment

Wayflyer Best for data-driven DTC brands scaling ad spend

Clearco Best for marketing and inventory spend reimbursement

8fig Best for marketplace sellers needing continuous capital plans

Settle Best for CPG ecommerce brands managing supplier payments

OnDeck Best for established ecommerce businesses wanting term loans

Bluevine Best for ecommerce businesses needing revolving credit lines

Fundbox Best for newer ecommerce businesses with limited credit history

SBA 7(a) Loan Best for established businesses seeking the lowest long-term rates

Master Comparison Table

Lender

Key Capabilities

Best For

Pricing

Luca AI ⭐⭐⭐⭐⭐

AI-driven underwriting, real-time ROI modeling, dynamic capital pricing, cross-functional cash flow intelligence

Founders who need capital + intelligence unified in one system

Low-barrier line of credit up to $150K, 600 min credit score, 12 to 24 week terms

Newer ecommerce businesses with limited credit history

Draw fee starting at 4.66% for 12-week terms

SBA 7(a) Loan ⭐⭐⭐

Up to $5M, lowest long-term rates, 10 to 25 year terms available

Established businesses willing to wait 60 to 90 days for cheapest capital

9 to 11.5% APR (prime + 2.25 to 4.75%)

🏆 1. Luca AI

✅ Why Did We Choose This Tool?

I built Luca AI because I lived the exact problem every ecommerce founder faces: capital providers who push money without understanding if you should take it, and analytics tools that show what happened but can't tell you what to do next. Luca is first on this list not just because I'm the author. It's here because it's the only platform that combines working capital with an AI reasoning engine that models whether deploying that capital will actually generate positive ROI. No other lender on this list can answer "If I take $75K and deploy it to Meta, what's my cash position in 90 days?" before you sign. That's intelligence-backed capital, and it's a category that didn't exist until we built it.

Luca AI's Working Capital intelligence dashboard serves as an AI Co-Founder for ecommerce, unifying sales analytics, ad spend modeling, inventory visibility, and embedded capital access in one conversational interface.

💰 Solutions Offered

Dynamic Capital Access Instant, non-dilutive funding with pricing that adjusts in real time based on current business health, not 90-day-old snapshots

Cross-Functional Cash Flow Modeling Ask "How much capital do I actually need for Q4?" and get answers synthesized across Shopify, Meta, Stripe, and Xero data

Proactive Working Capital Alerts 24/7 scanning surfaces cash runway compression, stockout risks, and scaling opportunities before they hit your P&L

Optimal Capital Sizing Luca recommends smaller, frequent advances to minimize idle capital and total cost, unlike lenders incentivized to push large lump sums

Unified Financial Intelligence Single conversational interface replacing 8 to 12 disconnected dashboards, spreadsheets, and financing applications

📊 Key Metrics

💸 Capital Range: €10K to €500K per advance, dynamically priced

⏰ Funding Speed: Same-day deployment

📊 Integrations: Shopify, Meta, Google Ads, Stripe, Xero, and 20+ data sources

✅ Personal Guarantee: None required

🔁 Repayment: Revenue-share, automated via platform integrations

🎯 Best For

Ecommerce founders ($1M to $20M revenue) who need working capital and strategic intelligence on how to deploy it, unified in a single AI Co-Founder interface.

📋 Case Study

The Problem: A €3M DTC skincare brand on Shopify faced a severe Q4 cash crunch. They needed €500K for November inventory by August, but their bank required a 90-day approval with personal guarantee. Wayflyer offered €500K at 8% flat fee, but the founder was not sure they needed the full amount upfront, leaving potential idle capital costing thousands in unnecessary fees.

How Luca Helped: Luca modeled the brand's actual capital needs by analyzing sales velocity, supplier payment timelines, and campaign ROAS data. Instead of one €500K lump sum, Luca recommended three staged draws: €150K in August, €200K in September (at a lower rate reflecting improved business health), and €100K in October.

The Outcome: Total cost of capital was 6.2% versus the 8% flat fee for a single large advance. Zero idle capital. The founder deployed every euro with ROI confidence because Luca had modeled the downstream cash flow impact before each draw.

Shopify Capital provides the fastest path to working capital for merchants already selling on Shopify. There is no application. Offers appear directly in your Shopify admin based on your sales history, and funds can arrive the same day. The product is a merchant cash advance (MCA) where Shopify buys a percentage of your future sales for a lump sum, collecting repayment as a fixed percentage of daily card sales.

Shopify Capital's funding dashboard surfaces pre-qualified offers directly inside your Shopify admin — zero application, zero credit check — but funds only Shopify-channel revenue while ignoring Amazon, wholesale, and every other sales channel.

💰 Solutions Offered

Merchant Cash Advances Lump sum from $200 to $2M in exchange for a share of future daily sales

Business Loans Fixed repayment over 12 months (available in select regions)

No Credit Check Required Eligibility based entirely on Shopify sales history and store performance

Automatic Remittance Daily percentage deducted from card sales; zero manual payment management

No Personal Guarantee Advances are unsecured with no collateral required

📊 Key Metrics

💸 Capital Range: $200 to $2,000,000

⏰ Funding Speed: Same-day (invite-only, no application)

📊 Factor Rate: 1.10 to 1.15 (flat fee ~10 to 15%)

✅ Personal Guarantee: None

🔁 Repayment: % of daily sales; max 18 months

🎯 Best For

Shopify-native merchants who need fast capital without paperwork and are comfortable with a higher effective cost for the convenience of same-day, no-application funding.

💬 Reviews

"Good value for money? No. Quick money in a pinch? Yes." u/nkl7e6h, r/shopify Reddit Thread

"Our recent Shopify Capital 180,000 loan has been declined after we applied. This is strange to me, as since 2025 we've successfully been accepted for and repaid over 500k in capital loans." r/shopify Reddit Thread

🏆 3. Amazon Lending

✅ Why Did We Choose This Tool?

Amazon Lending provides invite-only financing directly within Seller Central, offering term loans ($10K to $750K), cash advances, and lines of credit specifically designed for marketplace sellers. The deep native integration means Amazon can underwrite based on real-time seller performance data, including inventory velocity, sales rank, and customer metrics, rather than traditional credit checks.

💰 Solutions Offered

Term Loans Fixed amounts from $10K to $750K with 6 to 12 month repayment, auto-deducted from seller disbursements

Cash Advances $5K to $500K repaid as percentage of disbursements for rapid promotional campaigns

Revolving Line of Credit $10K to $500K draw-as-needed facility for seasonal demand swings

Community Lending $10K to $250K at 3 to 9% APR for underrepresented sellers with terms up to 5 years

No Collateral Required Unsecured financing based on seller account health

📊 Key Metrics

💸 Capital Range: $5,000 to $750,000 (up to $5M via Lendistry partner)

⏰ Funding Speed: 1 to 3 business days

📊 APR Range: 3 to 19% for term loans; 8 to 24% for cash advances

✅ Personal Guarantee: None for standard products

🔁 Repayment: Auto-deducted from seller disbursements

🎯 Best For

Amazon FBA sellers with established sales history who need inventory financing or promotional capital with repayment tied directly to their marketplace performance.

💬 Reviews

"Amazon Lending is invite-only and terms are non-negotiable. Great rates if you qualify, but you have zero control over when or what you're offered." Verified FBA Seller Trustpilot Review

"I've used Amazon Lending three times for inventory. The auto-deduction from disbursements is painless, but the lack of transparency around eligibility criteria is frustrating. I was approved one quarter and rejected the next with no explanation." u/17xhhjg, r/FulfillmentByAmazon Reddit Thread

🏆 4. PayPal Working Capital

✅ Why Did We Choose This Tool?

PayPal Working Capital removes traditional underwriting barriers. There is no credit check, no fixed monthly payment, and funds arrive within minutes of approval. Repayment is automatically deducted as a percentage of your PayPal sales, meaning you pay more when business is strong and less during slow periods. For sellers processing significant volume through PayPal, it is one of the most accessible capital options available.

💰 Solutions Offered

Working Capital Advance $1K to $300K (up to 35% of annual PayPal sales) repaid as percentage of each sale

PayPal Business Loan $5K to $150K with fixed weekly payments over 17 to 52 weeks

No Credit Check Eligibility based on PayPal account history and sales volume

Minutes-Fast Funding Capital deposited to your PayPal account within minutes

Flexible Repayment Choose your repayment percentage; no fixed payment schedule on Working Capital product

📊 Key Metrics

💸 Capital Range: $1,000 to $300,000

⏰ Funding Speed: Minutes after approval

📊 Cost Structure: Fixed fee (not APR); varies by amount, sales history, and repayment percentage

✅ Personal Guarantee: None

🔁 Repayment: % of each PayPal sale (Working Capital) or fixed weekly (Business Loan)

🎯 Best For

Ecommerce sellers with strong PayPal transaction volume who want fast, no-credit-check capital with revenue-aligned repayment.

💬 Reviews

"PayPal Working Capital is legitimate and many businesses use it successfully. The automatic repayment from sales can work well for businesses with consistent revenue, but becomes problematic when sales fluctuate or slow down." u/npmef8a, r/loansforsmallbusiness Reddit Thread

"This product is expensive compared to traditional business loans and the automatic deduction can destroy cash flow during slow periods." u/nph277v, r/loansforsmallbusiness Reddit Thread

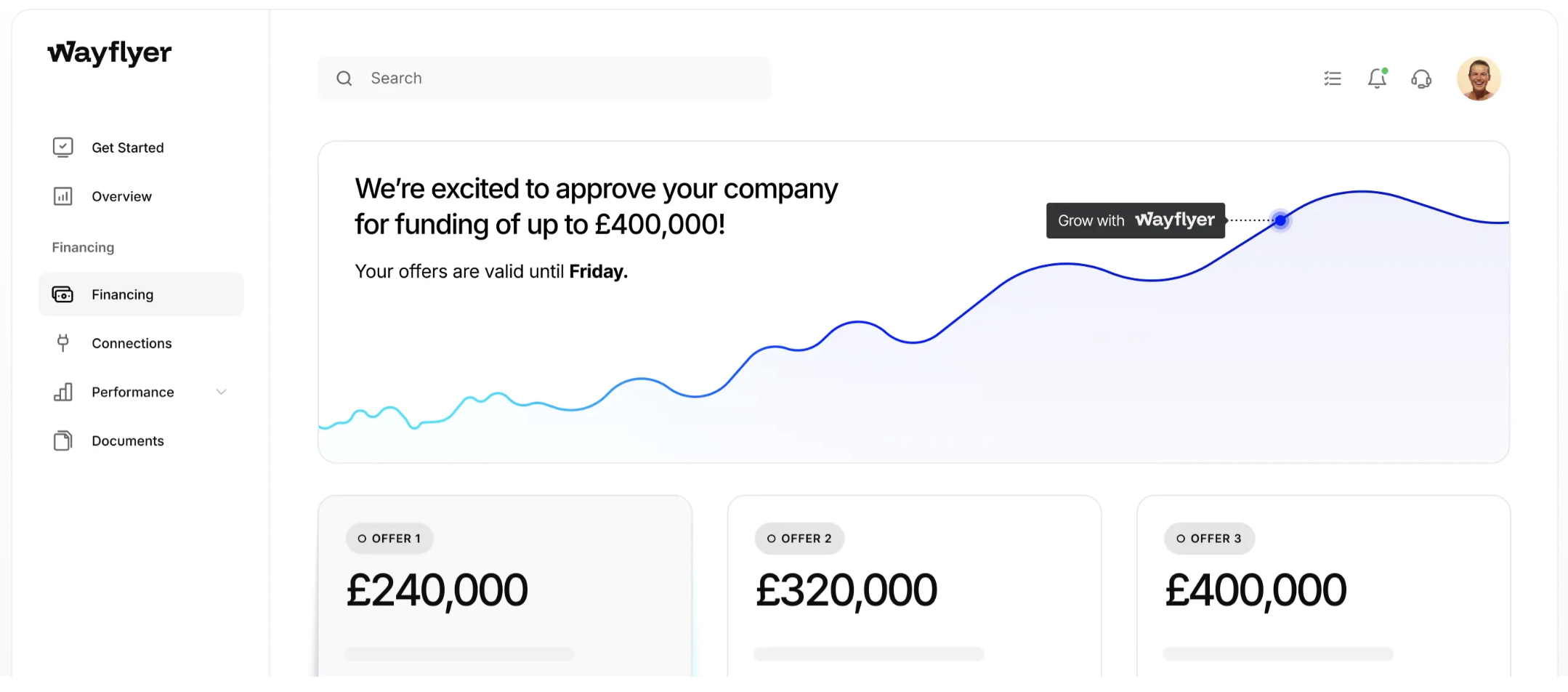

🏆 5. Wayflyer

✅ Why Did We Choose This Tool?

Wayflyer has deployed over $3.5 billion to ecommerce brands across the US, UK, EU, and Australia, offering revenue-based financing with some of the most competitive flat fees in the market, starting as low as 2% on funded amounts. They connect directly to Shopify, Amazon, Stripe, and ad platforms to underwrite based on live store performance data rather than credit scores alone.

Wayflyer's capital dashboard presents tiered funding offers alongside a revenue performance chart — approval in 24 hours with 2–9% flat fees — but underwriting is based on trailing sales snapshots with no intelligence layer to model whether scaling that campaign will tank your cash runway.

💰 Solutions Offered

Revenue-Based Advances $5K to $20M with flat fees starting at 2 to 9%

Multi-Currency Funding USD, GBP, EUR, and AUD to support international sellers

Data-Driven Underwriting Connects to ecommerce platforms and payment processors for real-time risk assessment

Flexible Repayment Daily, weekly, or bi-weekly remittance as percentage of sales

No Origination or Maintenance Fees Zero application, documentation, or unused facility fees

📊 Key Metrics

💸 Capital Range: $5,000 to $20,000,000

⏰ Funding Speed: As fast as 24 hours

📊 Flat Fee: 2 to 9% (effective APR 8 to 35%)

✅ Personal Guarantee: Not typically required (⚠️ UCC filing may apply)

🔁 Repayment: % of daily/weekly sales

🎯 Best For

Data-driven DTC brands doing $10K+ monthly revenue who want the most competitively priced revenue-based financing with global multi-currency support.

💬 Reviews

"Really disappointing experience. I have used Wayflyer on a number of occasions to help with Q4 stock purchasing and working capital requirements only to be told we no longer fit their criteria. Given we have used them multiple years running with no issues this was incredibly disappointing." Joshua Hannan Wayflyer Trustpilot Review

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC... the worst bank agreement I have read in 25 years." Zachary Piech Wayflyer Trustpilot Review

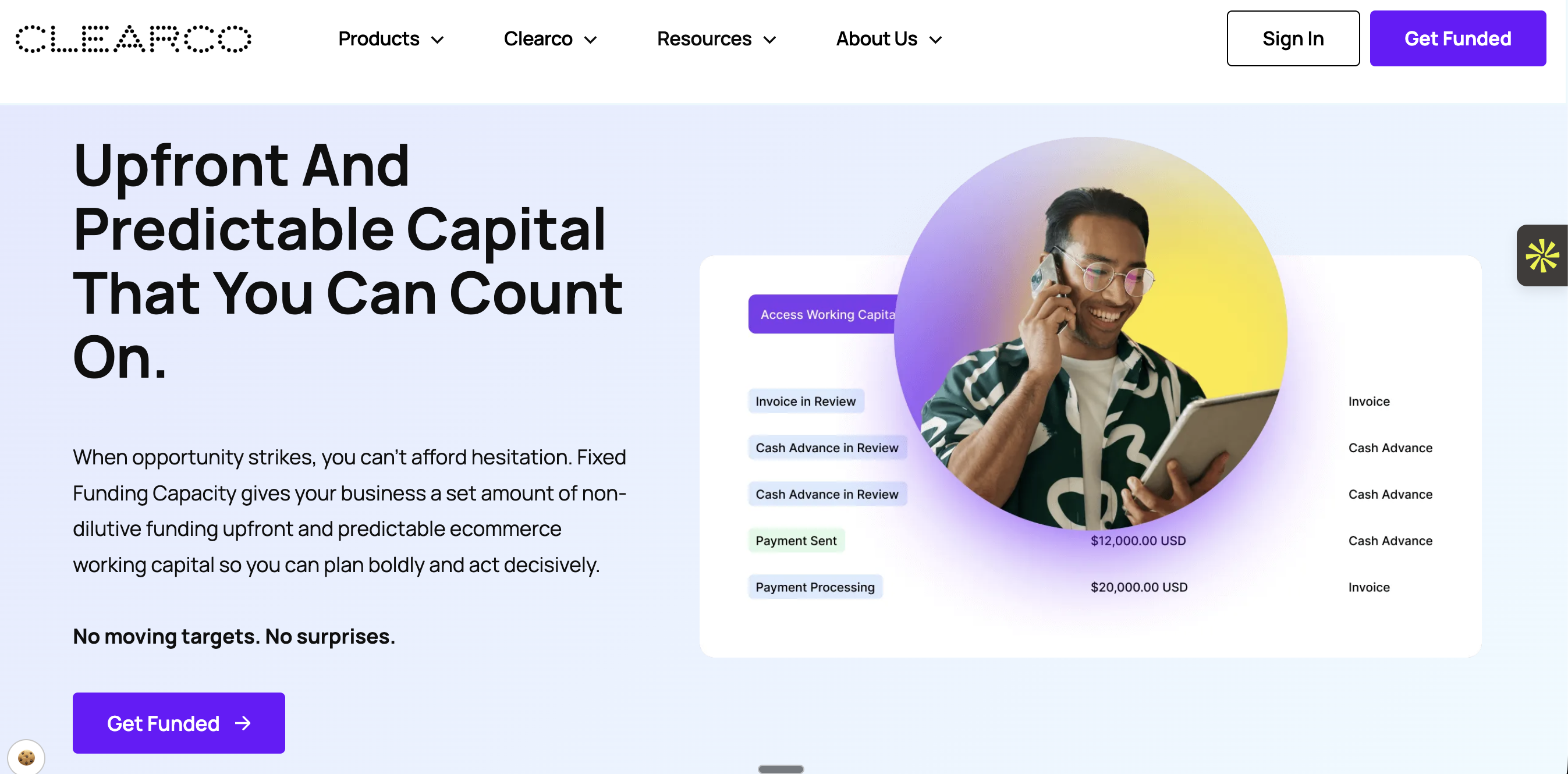

🏆 6. Clearco

✅ Why Did We Choose This Tool?

Clearco pioneered the receipt-and-invoice funding model for ecommerce, reimbursing marketing and inventory expenses with capped weekly repayments rather than uncapped daily percentage deductions. Their fixed weekly payment structure gives brands more predictable cash planning than traditional RBF providers who take larger cuts during high-revenue periods like BFCM.

Clearco's capital dashboard tracks cash advances, invoice funding, and payment status in one view — offering 6–12% flat-fee non-dilutive funding — but multiple borrowers report that repayment deductions exceeded contracted terms, inflating the effective cost well beyond the advertised rate.

💰 Solutions Offered

Receipt Funding Upload marketing/inventory receipts for reimbursement up to $1M; capped weekly repayments

Invoice Funding Advance against outstanding invoices for B2B and wholesale ecommerce

Fixed Weekly Payments Payments capped at a set amount rather than uncapped % of daily revenue

Prorated Early Repayment Fee reduces if you pay back early (unlike many MCA providers)

No Equity or Personal Guarantee Non-dilutive with no collateral required

📊 Key Metrics

💸 Capital Range: Up to $1,000,000 per advance

⏰ Funding Speed: 48 hours for term sheet; 1 to 5 days for funding

📊 Flat Fee: 5 to 12% depending on advance term (4-month = ~5%, 6-month = ~8%)

✅ Personal Guarantee: None

🔁 Repayment: Fixed capped weekly payments over 4 to 6 months

🎯 Best For

Ecommerce brands that need marketing and inventory capital with predictable, capped weekly repayments and early payoff discounts.

💬 Reviews

"Clearco Lost Touch With Its Own Business Model. Despite no change in our cash position or risk profile, and with strong recurring revenue, we started facing stricter cash-on-hand demands that made little sense for a company offering high-cost MCA." Melissa Clearco Trustpilot Review

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco Trustpilot Review

🏆 7. 8fig

✅ Why Did We Choose This Tool?

8fig takes a different approach from one-time lump sum advances. It provides continuous capital injections timed to your supply chain cycle, so capital arrives exactly when you need it for production, shipping, and inventory. Their AI-powered financial planning tool maps your entire supply chain timeline and structures payments accordingly, which is particularly valuable for marketplace sellers managing complex inventory flows.

💰 Solutions Offered

Continuous Capital Plans Funding delivered in scheduled injections aligned to your supply chain milestones

AI Supply Chain Planning Free financial planning tools that map inventory cycles and cash flow needs

Flexible Remittance Weekly or pay-as-you-go repayment structures over 4 to 6 months

Adjustable Payment Schedules Modify repayment timing based on cash flow changes

Up to $10M Funding Scales with established sellers as repayment history builds

📊 Key Metrics

💸 Capital Range: Up to $10,000,000

⏰ Funding Speed: Approval 24 to 48 hours; initial disbursement 1 to 3 business days

📊 Flat Fee: 6 to 10% of total funding amount

✅ Personal Guarantee: Not typically required

🔁 Repayment: Weekly/scheduled remittances over 4 to 6 months

🎯 Best For

Amazon and marketplace sellers with complex supply chain timelines who need capital delivered in stages aligned to production and shipping milestones.

💬 Reviews

"8fig's continuous funding model is genuinely different. Capital arrives when your supply chain needs it, not in one lump sum. But be careful with the 'offer more funds' cycle; the costs compound quickly if you keep extending." Verified eCommerce Seller 8fig Trustpilot Review

"The financial planning tool is actually useful for visualizing your cash flow timeline. That said, initial funding took closer to 2 weeks, not the '48 hours' they advertise." Amazon Seller 8fig Trustpilot Review

🏆 8. Settle

✅ Why Did We Choose This Tool?

Settle is more than a lender. It is an operating platform for CPG and wholesale ecommerce brands that combines financing ($20K to $15M) with bill pay, purchase order management, and inventory cost tracking in one system. Critically, Settle charges simple interest rather than flat fees, meaning your total cost decreases the faster you repay, a significant advantage over lenders who charge the same flat fee regardless of early payoff.

💰 Solutions Offered

Inventory Financing Fund inventory before it lands with flexible draw amounts from $20K to $15M

Bill Pay Platform Manage vendor payments, purchase orders, and landed cost tracking in one system

Simple Interest Pricing Total cost decreases with faster repayment, unlike flat-fee MCA providers

No Prepayment Penalties Pay back early and save; no escalating APRs or hidden fees

No Personal Guarantee or Equity Founder-friendly terms with transparent repayment schedules

📊 Key Metrics

💸 Capital Range: $20,000 to $15,000,000

⏰ Funding Speed: Fast application with rapid decisions

📊 Cost Structure: Simple interest (decreases with faster repayment)

✅ Personal Guarantee: None required

🔁 Repayment: Fixed, predictable repayment schedule (no daily % deductions)

🎯 Best For

CPG and wholesale ecommerce brands that need inventory financing combined with an operational back-office platform for vendor management and cost tracking.

💬 Reviews

"We've been using Settle to manage all of our inventory payments, and it has been a game-changer for our CPG ecommerce business. The platform is seamless, reliable, and has transformed our cashflow." Shopify App Review Settle Shopify App Store Review

"Financing options are easy to understand and built directly into the platform so you know exactly how much you're paying on each transaction. Also, really impressed with their AI tool when uploading bills." Shopify App Review Settle Shopify App Store Review

🏆 9. OnDeck

✅ Why Did We Choose This Tool?

OnDeck provides traditional term loans and lines of credit with same-day funding capability, making it one of the fastest conventional lenders for ecommerce businesses that prefer a straightforward fixed-payment structure over revenue-percentage models. They accept borrowers with credit scores as low as 625 and only one year in business, a lower barrier than most traditional lenders.

💰 Solutions Offered

Term Loans $5K to $250K with daily or weekly repayment over up to 24 months

Line of Credit $6K to $100K revolving facility with 12 to 24 month terms

Same-Day Funding Capital deployed as fast as the same business day

Subpar Credit Accepted Minimum 625 FICO, $100K annual revenue, 1 year in business

Instant Draws Line of credit withdrawals of $1K to $10K funded within 30 minutes

📊 Key Metrics

💸 Capital Range: $5,000 to $250,000

⏰ Funding Speed: Same-day (instant for small draws)

📊 APR Range: 35 to 99% estimated (factor-rate based)

✅ Personal Guarantee: Yes, required

🔁 Repayment: Daily or weekly; terms up to 24 months

🎯 Best For

Established ecommerce businesses ($100K+ annual revenue) that prefer fixed-payment term loans with fast funding and can accept higher APR in exchange for speed and accessibility.

💬 Reviews

"OnDeck was fast. Funds arrived same day. But the effective APR was significantly higher than I expected once I calculated it from the factor rate. Good for emergencies, not for long-term capital needs." Small Business Owner OnDeck Trustpilot Review

"Potentially high cost to borrow: OnDeck might use a factor rate that translates into an APR of 31.00% or higher." WSJ Buy Side Analysis OnDeck WSJ Review

🏆 10. Bluevine

✅ Why Did We Choose This Tool?

Bluevine offers one of the more competitive revolving lines of credit for ecommerce businesses, with starting simple interest rates of 7.80% and credit limits up to $250K. The revolving structure means you only pay interest on what you draw, making it ideal for ecommerce brands with fluctuating capital needs across seasons rather than a one-time lump sum requirement.

💰 Solutions Offered

Revolving Line of Credit Up to $250K; draw and repay as needed with same-day access

Term Line of Credit $5K to $200K with 6 or 12 month fixed terms

Same-Day Funding Draws processed same business day

Monthly or Weekly Repayment Flexible payment schedules to match cash flow patterns

Low Minimum Requirements 625 credit score, $40K monthly revenue, 24 months in business

🔁 Repayment: Weekly or monthly over 6 to 12 months

🎯 Best For

Ecommerce businesses with recurring but variable capital needs, including seasonal inventory purchases, ad spend scaling, or bridging payout gaps, that benefit from draw-as-needed flexibility.

💬 Reviews

"Bluevine's line of credit is great for its flexibility. Only borrowing what you need. But 'starting at 7.80%' is misleading since that's simple interest, not APR. The actual annual cost can be 20 to 50% when you calculate it properly." Business Financing Review Bluevine Trustpilot Review

"Approved and funded in under 24 hours. The revolving structure is exactly what seasonal ecommerce needs. Just be prepared for the personal guarantee requirement." Online Seller Bluevine Trustpilot Review

🏆 11. Fundbox

✅ Why Did We Choose This Tool?

Fundbox is the most accessible lender on this list for newer ecommerce businesses, requiring just a 600 credit score, $100K annual revenue, and three months in business. Their line of credit up to $150K with 12 or 24 week terms fills the gap for early-stage sellers who cannot yet qualify for Bluevine, OnDeck, or SBA programs.

💰 Solutions Offered

Business Line of Credit Up to $150K (up to $250K on some products) with 12 or 24 week terms

Low Barrier to Entry 600 minimum credit score, $100K annual revenue, 3 months in business

No Prepayment Penalties Pay back early and reduce your draw fee

Fast Approval Automated underwriting with same-day decision and funding

Simple Draw Fee Structure Starting at 4.66% for 12-week terms; 8.99% for 24-week terms

📊 Key Metrics

💸 Capital Range: $1,000 to $150,000

⏰ Funding Speed: Same-day

📊 Draw Fee: Starting at 4.66% (12-week) or 8.99% (24-week)

✅ Personal Guarantee: Yes, required

🔁 Repayment: Weekly over 12 or 24 weeks

🎯 Best For

Newer ecommerce businesses (3+ months old) with lower credit scores that need a small-to-mid-size line of credit to manage operational cash flow gaps.

💬 Reviews

"Fundbox approved me with a 620 credit score when everyone else said no. The rate isn't cheap, but for a business under a year old, having any access to a credit line was the difference between stocking inventory and missing Q4." Small Business Owner Fundbox Trustpilot Review

"Interest rates start low but the weekly repayment on a 12-week term means you're paying it back fast. Good for very short-term needs, not for ongoing working capital." Verified Borrower Fundbox Trustpilot Review

🏆 12. SBA 7(a) Loan

✅ Why Did We Choose This Tool?

The SBA 7(a) loan offers the lowest long-term interest rates available to ecommerce businesses, currently 9 to 11.5% APR based on the April 2026 prime rate of 6.75%. For established sellers willing to navigate the 60 to 90 day application process with full documentation, an SBA loan provides the cheapest capital for large, long-horizon needs like warehouse buildouts, major inventory investments, or business acquisitions.

💰 Solutions Offered

Term Loans up to $5M The largest non-dilutive capital option available to small businesses

Lowest APR in Market Variable rates from prime + 2.25% to prime + 4.75%

Long Repayment Terms Up to 10 years for working capital; up to 25 years for real estate

SBA Express Loans Faster processing for amounts up to $500K

Fee Waivers SBA guarantee fees waived for loans under $125K

📊 Key Metrics

💸 Capital Range: Up to $5,000,000

⏰ Funding Speed: 60 to 90 days (Express: 2 to 4 weeks)

📊 APR Range: 9.00 to 11.50% (April 2026)

✅ Personal Guarantee: Yes, required for loans over $25K

🔁 Repayment: Monthly; terms up to 10 years for working capital

🎯 Best For

Established ecommerce businesses (2+ years, 680+ credit, demonstrated profitability) seeking the lowest possible long-term capital cost and willing to invest time in the application process.

💬 Reviews

"I've taken almost a million total through Shopify Capital. You can make it work well in some industries. Now I do SBA." u/n7yyk6y, r/shopify Reddit Thread

"If you aren't qualifying for legitimate financing and your business is more than 2yrs old, ask your accountant why not and see if you can fix it." u/nklbup0, r/shopify Reddit Thread

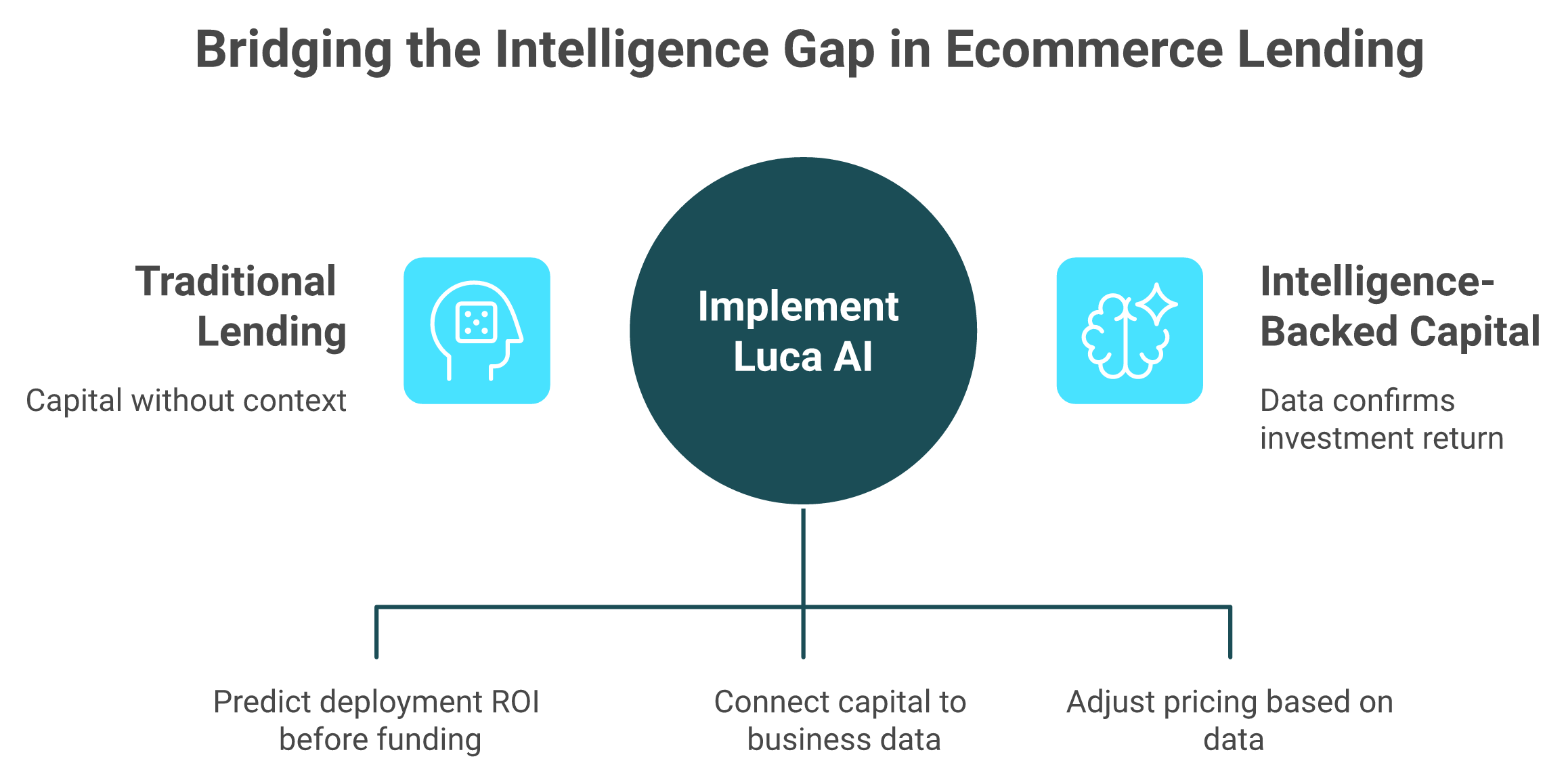

⚠️ The Intelligence Gap Across All 11 Standalone Lenders

Every lender profiled above, from Shopify Capital to SBA 7(a), answers the question "Can I get capital?" None of them answers the question that actually matters: "Should I take this capital, and where should I deploy it for the highest return?" That is the fundamental gap Luca AI was built to close. By unifying working capital with cross-functional business intelligence, Luca ensures that every dollar of capital deployed is backed by data-driven reasoning across your marketing performance, inventory timing, cash conversion cycle, and financial runway. It is the difference between borrowing money and making an investment decision.

Q2. How Were These 12 Ecommerce Working Capital Lenders Evaluated and Scored? [toc=Evaluation Methodology]

Choosing a working capital lender is not a one-dimensional decision. A low headline rate means nothing if the lender can't integrate with your sales channels, hides fees in the fine print, or offers capital without helping you understand whether the deployment makes financial sense. To create a credible, repeatable ranking, we scored every lender across five weighted criteria totaling 100%.

⭐ The Five Evaluation Criteria

Scoring Methodology for Ecommerce Working Capital Lenders

Criteria

Weight

What It Measures

Ecommerce Specialization

25%

Platform integrations (Shopify, Amazon, Stripe), understanding of online seller cash flows, marketplace payout awareness, and ecommerce-specific underwriting

Cost Transparency

20%

Fee structure clarity, ability to calculate true APR, absence of hidden charges (origination, UCC, prepayment penalties), and honest sales communication

Funding Speed & Flexibility

20%

Application-to-funds timeline, revenue-linked repayment options, early repayment terms, and ability to adjust capital amounts mid-cycle

Qualification Accessibility

20%

Minimum revenue thresholds, credit score floors, time-in-business requirements, collateral demands, and personal guarantee obligations

Capital + Intelligence Integration

15%

Whether the lender provides analytics, ROI modeling, cash flow forecasting, or decision-support data alongside capital deployment

The total across all five criteria sums to 100%. Each lender was scored against these dimensions using publicly available product data, verified user reviews, and official documentation.

📊 Star Rating Methodology

Scores map to a five-tier star system: 5★ (81 to 100 points), 4★ (61 to 80), 3★ (41 to 60), 2★ (21 to 40), 1★ (0 to 20). No lender on this list scored below 3 stars. Tools that fell below that threshold were excluded during research.

Star Ratings for All 12 Lenders

Lender

Star Rating

Luca AI

⭐⭐⭐⭐⭐

Shopify Capital

⭐⭐⭐⭐

Amazon Lending

⭐⭐⭐⭐

Wayflyer

⭐⭐⭐⭐

Bluevine

⭐⭐⭐⭐

PayPal Working Capital

⭐⭐⭐⭐

Settle

⭐⭐⭐⭐

Clearco

⭐⭐⭐

OnDeck

⭐⭐⭐

8fig

⭐⭐⭐

Fundbox

⭐⭐⭐

SBA 7(a) Loan

⭐⭐⭐

💡 Why Capital + Intelligence Integration Matters

Most working capital decisions in ecommerce fail not because the money was expensive, but because it was deployed without understanding inventory timing, ad performance trajectory, or cash conversion impact. A founder who borrows $100K to scale a Meta campaign without modeling the downstream cash flow effect is gambling, not growing. Traditional lenders score zero on this dimension because they treat capital as a standalone transaction.

Traditional lenders answer 'Can I get capital?' — only intelligence-backed capital answers 'Should I take it, and where should I deploy it?'

✅ Luca AI is the only entrant scoring maximally on Capital + Intelligence Integration. It models deployment ROI before funding, connects capital decisions to cross-functional data (marketing to inventory to cash position), and dynamically prices advances based on real-time business health rather than static applications. ❌ Every other lender on this list, from Shopify Capital to SBA 7(a), provides money without context on whether taking it is the right strategic move.

Q3. What Types of Working Capital Financing Exist for Ecommerce and How Does Online Seller Cash Flow Differ? [toc=Financing Types Explained]

Before evaluating specific lenders, founders need to understand why ecommerce businesses face structurally different cash flow challenges than traditional retail, and which financing types exist to solve each variation of the problem.

⏰ Why Ecommerce Cash Flow Is Structurally Different

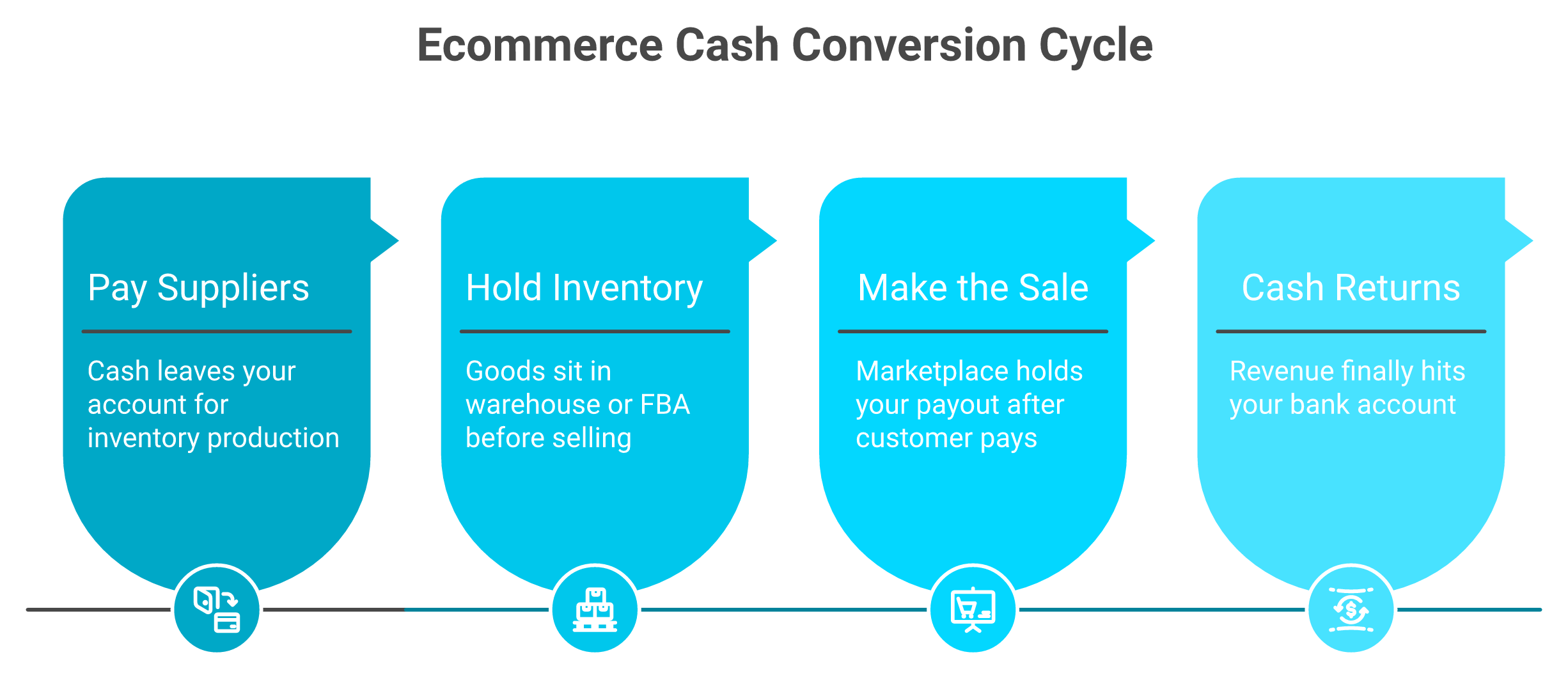

Traditional retail collects payment at the point of sale. Ecommerce doesn't. The timing mismatch between spending money and receiving it creates a persistent working capital gap that widens during growth phases. According to recent industry data, 35% of US online retailers experienced cash flow difficulties in 2024, even while reporting revenue growth.

Delayed marketplace payouts : Amazon holds seller disbursements for 14 days; Shopify Payments settles in 1 to 3 business days; PayPal can hold funds for 21+ days on new accounts

Upfront inventory purchasing : Production orders require payment 60 to 90 days before goods arrive and sell

Ad spend timing gaps : Meta and Google charge immediately; revenue from those campaigns materializes days to weeks later

Seasonal demand volatility : BFCM, Prime Day, and Q4 spikes require capital months in advance; Q1 slowdowns compress cash runway

2026 tariff pressures : Tariff surcharges are increasing COGS and forcing higher inventory pre-purchases, further straining working capital as companies hold more cash at customs and build safety stock buffers

A 2026 Versapay survey of 400 finance leaders found that 69% reported increased late customer payments over the past year, while 78% said unexpected AR issues are now forcing changes to capital investments and hiring plans.

💰 Financing Types Available to Ecommerce Businesses

Ecommerce Financing Types Comparison

Financing Type

How It Works

Typical Cost

Speed

Best Ecommerce Use Case

Term Loans

Fixed lump sum, fixed repayment schedule

6 to 36% APR

1 to 4 weeks

Large inventory purchases, warehouse buildouts

Business Lines of Credit

Revolving draw; pay interest only on used amount

7 to 25% APR

Same-day draws

Ongoing operational gaps, seasonal bridge funding

Revenue-Based Financing

Fixed fee repaid as % of daily/weekly sales

6 to 12% flat fee

24 to 72 hours

Ad scaling, inventory restock during growth spurts

Merchant Cash Advance

Factor rate (1.1 to 1.5) on future sales; daily auto-debit

20 to 60%+ effective APR

Same-day

Emergency capital; highest cost, fastest speed

Invoice Factoring

Advance against outstanding B2B invoices

1 to 5% per invoice

1 to 3 days

B2B and wholesale ecommerce with net-30/60 terms

Inventory/PO Financing

Capital specifically for purchasing inventory or fulfilling POs

1 to 6% per month

3 to 10 days

Inventory-heavy brands managing supplier payments

SBA 7(a) Loan

Government-backed term loan; lowest rates, longest approval

9 to 11.5% APR

60 to 90 days

Established businesses seeking cheapest long-term capital

Platform-Embedded Lending

Native offers from Shopify/Amazon/PayPal; no application

Factor rate or fixed fee

Same-day

Quick capital for platform-native merchants

✅ Non-Dilutive vs. Dilutive: When to Choose Debt Over Equity

If your capital need is short-term and tied to a specific opportunity, such as inventory for Q4, scaling a proven Meta campaign, or bridging a payout delay, non-dilutive working capital preserves ownership and makes financial sense. Equity should be reserved for long-horizon investments like team building, R&D, or market expansion where the payoff timeline exceeds 12 months. Most ecommerce founders at $1M to $20M revenue should exhaust non-dilutive options before diluting.

As one DTC financing guide put it: "When recurring expenses are funded with equity, dilution becomes a habit. The business grows, but ownership keeps shrinking, for a problem that working capital should have solved."

🔍 Where Luca AI Fits

Luca AI helps founders navigate this complexity by modeling which financing type fits their specific cash flow pattern. Ask "What type of capital should I use for Q4 inventory?" and get a recommendation based on your real-time cash conversion cycle, revenue trajectory, and repayment capacity, not a generic comparison table.

Q4. What Does an Ecommerce Working Capital Loan Actually Cost and What Are the Hidden Fee Red Flags? [toc=True Costs and Hidden Fees]

You accepted a $75K advance at an advertised "8% flat fee" expecting $6,000 in total cost. Three months in, you've also paid a $2,250 origination fee, a $350 UCC filing fee, and discovered that early repayment doesn't reduce the total amount owed. Your actual cost: $8,600, an effective 11.5% fee. Annualize that over a 6-month term and you're looking at 40%+ APR. This is not hypothetical. Real ecommerce founders report these experiences across multiple lenders.

⚠️ How "Flat Fees" Mask True Cost

The fundamental problem is that flat fees and factor rates obscure the time-value of money. A 10% flat fee sounds reasonable until you realize you're repaying it over 4 to 6 months through daily deductions, meaning on average, you only had access to half the capital for the full term. The conversion is straightforward: divide the fee by the average outstanding balance, then annualize. A "6% flat fee" on a 4-month MCA with weekly repayment translates to roughly 36% APR

💸 True Cost of Borrowing $100K Across Lender Types

True Cost Comparison for $100K Borrowed

Lender Type

Advertised Cost

Total Dollar Cost on $100K

Effective APR (6-month term)

Shopify Capital

Factor 1.10 to 1.15

$10,000 to $15,000

~25 to 35%

Wayflyer

2 to 9% flat fee

$2,000 to $9,000

~8 to 27%

Clearco

6 to 12% flat fee

$6,000 to $12,000

~35 to 40% (reported by users)

8fig

6 to 10% per cycle

$6,000 to $10,000+ (escalates)

Variable; can exceed 40%

OnDeck

35 to 99% APR

$17,500 to $49,500

35 to 99%

Bluevine

Starting 7.80% simple

$7,800+

14 to 95%

Fundbox

4.66%+ draw fee

$4,660+ (12 weeks)

~24 to 30% annualized

SBA 7(a)

Prime + 2.25 to 4.75%

$4,500 to $5,750/year

9 to 11.5%

Luca AI

Dynamic pricing

Adjusts per advance based on real-time health

Optimized per draw

⚠️ Revenue level changes everything. At $20K monthly revenue, a $100K MCA repaid at 10% of daily sales takes ~17 months, and the effective APR drops. At $500K monthly revenue, the same advance repays in under 2 months, and the effective APR skyrockets because you paid the full flat fee while holding capital for a fraction of the year.

🚩 Hidden Fee Red Flags Checklist

Origination fees (1 to 5%) : Added on top of the advertised rate; often buried in documentation

UCC filing fees ($100 to $500) : Lenders file a lien on your business assets, sometimes without clear disclosure

Prepayment penalties that lock full cost : Many MCAs charge the same total fee whether you repay in 2 months or 12

Fund redirection clauses : Wayflyer's contract includes the right to "redirect your Shopify funds to their account" and "enter your building and take your property in excess of the value of what is owed"

"Read their terms and contract carefully! They said their offer is not secured, which is false, they still will file UCC... they can enter your building and take your property in excess of the value of what is owed. They can redirect your Shopify funds to their account... the worst bank agreement I have read in 25 years." Zachary Piech Wayflyer - Trustpilot Review

"They trick you into signing a low APR contract, and then one month into the term, they hike up the rates by offering more funds. They divide the lending into cycles. I only received one. The second and third funding were pulled at the last minute." Khalid 8fig - Trustpilot Review

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated thereby increasing the effective interest rate significantly and then could never resolve these issues." Thomas Bishop Clearco - Trustpilot Review

✅ How Luca AI Eliminates Cost Blindness

Luca AI calculates the total cost of capital, including all fees, and converts it to effective APR at your projected sales velocity before you accept any funding. More critically, it models whether the ROI of deploying that capital exceeds the cost: "If I take $75K and put it into Meta, will the return cover the 8% fee plus generate profit within the repayment window?" You see both the cost and the payoff, before you sign. Intelligence-backed capital means you never accept funding blindly.

Q5. How Does the Ecommerce Cash Conversion Cycle Work and When Should You Stack Multiple Capital Sources? [toc=Cash Conversion Cycle]

Amazon operates on a negative cash conversion cycle of approximately -28 to -40 days, collecting customer payments immediately while negotiating 60 to 90 day supplier terms, effectively using supplier money to fund growth across AWS, warehousing, and logistics. That negative CCC is Amazon's growth engine. Most ecommerce founders don't have that leverage, and without understanding their own CCC, they're making capital decisions blind.

📊 The CCC Formula for Ecommerce

The cash conversion cycle measures how many days your cash is tied up between paying for inventory and collecting revenue from customers:

CCC = Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) - Days Payable Outstanding (DPO)

Your cash is trapped between paying suppliers and collecting revenue — the CCC measures exactly how long that gap lasts for your business type.

Cash Conversion Cycle by Ecommerce Archetype

Ecommerce Archetype

DIO

DSO

DPO

CCC

Working Capital Need at $1M Revenue

DTC Shopify Brand

30 days

2 days

15 days

17 days

~$47K

Amazon FBA Seller

45 days

14 days

20 days

39 days

~$107K

Multi-Channel + Wholesale

50 days

35 days

25 days

60 days

~$164K

A CCC of 45 days means every £1 of revenue ties up working capital for 45 days before returning to your account. The longer your CCC, the more external capital you need to maintain operations, let alone grow.

⏰ Seasonal Capital Stacking Framework

Rather than relying on a single capital source year-round, sophisticated operators layer financing types across the ecommerce calendar:

Sophisticated ecommerce operators don't rely on one capital source — they layer financing types across the seasonal calendar to match each quarter's needs.

Q1 Recovery : Revolving LOC (Bluevine/Fundbox) for operational bridge + begin SBA 7(a) application for long-term base capital

Q2 Inventory Loading : RBF (Wayflyer/Settle) for supplier pre-payments on Q4 inventory

Q3 Pre-Peak : Platform capital (Shopify Capital) for ad scaling + inventory top-ups

Q4 Execution : Stack RBF for final inventory + platform capital for BFCM ad spend

⚠️ Stacking rules: Total repayment obligations across all sources must stay below 20 to 25% of monthly revenue. Many MCA providers explicitly prohibit stacking in their contracts and can demand immediate repayment if they discover additional positions. Use cheapest capital for longest-horizon needs, and fastest capital for time-sensitive opportunities.

🔄 Financing Graduation Path

Year 1 : Platform-embedded MCA (Shopify Capital, PayPal Working Capital) for accessibility

Year 2 : Add RBF or LOC for flexibility (Wayflyer, Bluevine) as revenue history builds

Year 3+ : Layer SBA 7(a) for lowest-cost base capital + RBF for seasonal peaks

✅ Where Luca AI Connects the Dots

Most ecommerce brands at $1M to $20M make capital timing decisions by accident. Shopify doesn't calculate CCC, and Xero doesn't connect payables to marketing spend. Luca AI calculates real-time CCC by synthesizing Shopify order data, Stripe/PayPal payout timing, Xero payables, and inventory velocity. Ask "What's my cash conversion cycle, and what happens if I negotiate 45-day supplier terms?" or model stacking scenarios: "If I take $50K from Shopify Capital for ads and $75K from Wayflyer for inventory, what's my cash position through Q4?" No standalone lender provides this unified forecast.

Q6. Which Lender Fits Your Ecommerce Business Type and How Do You Qualify for the Best Rates? [toc=Lender Fit by Business Type]

With 12 lenders across four categories, the real challenge isn't access to capital. It's matching your specific business stage, channel mix, credit profile, and seasonal pattern to the right financing type. Choosing based on funding speed alone or lowest advertised rate without modeling repayment cash flow impact is how founders end up overpaying by 30 to 50%.

💰 Scenario-Based Lender Recommendations

Recommended Lenders by Ecommerce Business Type

Your Business Type

Recommended Primary Lender

Recommended Stack

Shopify DTC brand

Shopify Capital

+ Wayflyer for inventory

Amazon FBA seller

Amazon Lending

+ 8fig for continuous capital

Multi-channel seller

Bluevine LOC

+ Settle for supplier payments

Seasonal ecommerce

Stacked RBF + platform capital

Per Q5 quarterly framework

Early-stage (under 1 year)

PayPal Working Capital

+ Fundbox LOC

Scaling brands ($1M+)

SBA 7(a) for base

+ Wayflyer for seasonal peaks

Bad credit (below 600)

Shopify Capital or PayPal

No credit check, sales-based

✅ The Right Evaluation Framework

Rather than comparing headline rates, evaluate every lender against six criteria:

True Cost Clarity : Can you calculate effective APR, not just the advertised flat fee?

Repayment Flexibility : Does repayment flex with revenue, or are you locked into fixed daily deductions?

Deployment Intelligence : Does the lender help you understand where to deploy capital?

Speed vs. Cost Trade-off : Does the funding timeline match your opportunity window?

Ecosystem Fit : Does the lender integrate with your sales channels (Shopify, Amazon, Stripe)?

Stacking Compatibility : Can you layer this with other sources without penalties?

📋 How to Qualify for the Best Rates

💳 Maintain a 680+ credit score (625 minimum for OnDeck/Bluevine; none required for Shopify Capital/PayPal)

⏰ 12+ months operating history (3 months minimum for Fundbox)

💸 Consistent monthly revenue above $10K with clean bank statements (3 to 6 months)

The real question isn't "which lender has the lowest rate." It's "which system tells you whether this capital will generate a positive return before you sign." Only Luca AI scores perfectly on Deployment Intelligence because it models ROI before disbursement.

Q7. Questions Ecommerce Founders Ask Before Choosing a Working Capital Loan [toc=Common Founder Questions]

Can you get an SBA 7(a) loan for an ecommerce business?

Yes, but it requires patience and preparation. SBA 7(a) loans are available to ecommerce businesses that meet the standard eligibility criteria: operate for profit, be located in the U.S., qualify as "small" under SBA size requirements, and demonstrate reasonable ability to repay. In practice, most approved ecommerce applicants have 680+ credit scores, 2+ years in business, demonstrated profitability, and can provide a personal guarantee.

The SBA's Working Capital Pilot (WCP) program, which has delivered more than $150 million in new lending since its inception, offers flexible credit lines with both asset-based and transaction-based financing options. While manufacturers account for over 25% of the WCP portfolio, ecommerce businesses with inventory assets can also qualify.

Do working capital loans require a personal guarantee?

It depends entirely on the lender type:

Personal Guarantee Requirements by Lender Category

❌ Usually no, but may file UCC lien on business assets

Lines of credit (Bluevine, Fundbox, OnDeck)

✅ Yes, required for most products

SBA 7(a) loans

✅ Yes, required for loans above $25K

⏰ How Fast Can Ecommerce Businesses Get Working Capital?

Same-day: Shopify Capital, PayPal Working Capital, Bluevine (small draws), OnDeck

1 to 3 days: Wayflyer, Clearco, 8fig, Fundbox

1 to 2 weeks: Larger term loans, new LOC applications

60 to 90 days: SBA 7(a) (SBA Express: 2 to 4 weeks for up to $500K)

💳 Will a Working Capital Loan Affect My Credit Score?

MCA and revenue-based financing products (Shopify Capital, Wayflyer, Clearco) typically do not report to credit bureaus, meaning they won't help or hurt your score. Term loans and lines of credit (OnDeck, Bluevine, Fundbox) generally do report, which can build credit history with on-time payments but damage it with missed ones. SBA loans report to all three major bureaus.

💸 How Much Working Capital Does an Ecommerce Business Need?

Calculate your CCC using the framework in Q5, then multiply by your daily operating cost. A general rule: maintain 2 to 3 months of operating expenses as a working capital buffer. For a $1M revenue DTC brand with a 17-day CCC, that's roughly $47K in working capital need; for a multi-channel seller with a 60-day CCC, it's closer to $164K.

✅ How Luca AI Personalizes These Answers

For founders who want answers to these questions based on their actual business data, not generic guidelines, Luca AI models your specific qualification probability, calculates your exact working capital need from real-time CCC, and identifies which lender fits your credit profile, revenue stage, and seasonal pattern. Ask "Am I likely to qualify for SBA 7(a), and is the 90-day wait worth it vs. taking Shopify Capital today?" and get a data-backed answer in seconds, because the right answer depends on your cash position, not a comparison table.

FAQ's

What is the cheapest working capital loan for an ecommerce business in 2026?

The cheapest long-term working capital for ecommerce businesses is the SBA 7(a) loan, currently priced at 9 to 11.5% APR based on the April 2026 prime rate of 6.75%. However, it requires 680+ credit, 2+ years in business, a personal guarantee, and a 60 to 90 day approval timeline.

For founders who need faster capital, revenue-based financing from providers like Wayflyer (2 to 9% flat fee) offers competitive short-term pricing, though the effective APR rises significantly at higher revenue levels because you repay the full flat fee faster.

We built Luca AI's financial management tools to solve this exact problem: before you accept any advance, we calculate total cost of capital including all fees, convert it to effective APR at your projected sales velocity, and model whether the deployment ROI exceeds the borrowing cost. The cheapest loan on paper is not always the smartest capital decision. A 9% SBA loan that takes 90 days to close can cost more in missed opportunity than a 6% Wayflyer advance funded in 24 hours. True cost clarity requires modeling both the price of capital and the price of waiting.

Can I get a working capital loan for my ecommerce business without a personal guarantee?

Yes. Several ecommerce-specific lenders offer working capital without requiring a personal guarantee. Platform-embedded options like Shopify Capital, PayPal Working Capital, and Amazon Lending are entirely sales-based with no credit check and no personal guarantee.

Revenue-based financing providers including Wayflyer, Clearco, and 8fig also typically do not require personal guarantees, though they may file a UCC lien on your business assets. This is an important distinction: a UCC filing is not a personal guarantee, but it does give the lender a secured claim against business property.

Traditional lenders like Bluevine, OnDeck, Fundbox, and SBA 7(a) programs do require personal guarantees for most products. We help founders navigate these trade-offs through our working capital planning tools, which map your qualification profile against each lender's requirements and recommend the optimal match based on your credit score, revenue stage, and risk tolerance. The goal is matching your business to a lender where you qualify for the best terms, not just the fastest approval.

How do I calculate how much working capital my ecommerce business needs?

We use the cash conversion cycle (CCC) formula: CCC = Days Inventory Outstanding + Days Sales Outstanding minus Days Payable Outstanding. Once you know your CCC, multiply it by your average daily operating cost to determine your baseline working capital need.

For context, a DTC Shopify brand typically has a 17-day CCC requiring roughly $47K in working capital per $1M revenue. An Amazon FBA seller averages a 39-day CCC needing about $107K. A multi-channel seller with wholesale can hit a 60-day CCC requiring $164K or more.

Maintain 2 to 3 months of operating expenses as a buffer

Add seasonal peaks: BFCM and Q4 inventory loading can double your baseline need

Factor in 2026 tariff surcharges increasing COGS and safety stock requirements

Rather than estimating manually, our cash flow forecasting engine calculates your real-time CCC by synthesizing Shopify order data, Stripe and PayPal payout timing, Xero payables, and inventory velocity, giving you a precise capital figure instead of a generic estimate.

What hidden fees should I watch for in ecommerce working capital loans?

We have identified five critical hidden fee red flags that ecommerce founders encounter across multiple lenders:

Origination fees (1 to 5%): Added on top of the advertised flat fee and often buried in closing documentation.

UCC filing fees ($100 to $500): Lenders file a lien on your business assets, sometimes without upfront disclosure during the sales process.

Prepayment penalties that lock full cost: Many MCAs charge the same total fee whether you repay in 2 months or 12, eliminating any benefit from early payoff.

Fund redirection clauses: Some contracts include rights to redirect your platform payouts directly to the lender's account.

Post-signing repayment changes: Multiple verified reviews report repayment amounts increasing after the contract is signed.

The core issue is that flat fees and factor rates obscure the time-value of money. A 10% flat fee repaid over 4 to 6 months through daily deductions means you only had access to about half the capital on average. We built our unit economics tracking to calculate true effective APR at your projected sales velocity before you accept any offer, so you see the real cost, not the marketed one.

Should I stack multiple working capital sources for my ecommerce store?

Yes, but only with a structured framework. We recommend a seasonal capital stacking approach where you layer different financing types across the ecommerce calendar based on cost, speed, and purpose:

Q1 Recovery: Revolving line of credit for operational bridge funding, plus begin SBA 7(a) application for long-term base capital.

Q2 Inventory Loading: Revenue-based financing for supplier pre-payments on Q4 inventory.

Q3 Pre-Peak: Platform capital like Shopify Capital for ad scaling and inventory top-ups.

Q4 Execution: Stack RBF for final inventory purchases plus platform capital for BFCM ad spend.

The critical stacking rule: total repayment obligations across all sources must stay below 20 to 25% of monthly revenue. Many MCA providers explicitly prohibit stacking in their contracts and can demand immediate repayment if they discover additional positions. We help founders model these scenarios through our data analysis tools, which forecast your combined cash position across multiple capital sources and flag repayment conflicts before they become problems.

Enjoyed the read? Join our team for a quick 15-minute chat — no pitch, just a real conversation on how we’re rethinking Ecommerce with AI - Luca

Loading Schedule...

Your AI Co-Founder is here.

Here’s why:

Shopify, Meta, Xero - one brain.

"Should I scale?" Answered with real data.

Growth capital. No applications. One click.

Thank you! Your submission has been received! Please book a time slot for the Meeting

Oops! Something went wrong while submitting the form.

.png)